Consumers benefit from access to Buy Now, Pay Later options

Photo Credit: Getty

In a rapidly evolving retail landscape, with more and more commerce moving online, there has been a rise of financial technology (or fintech) tools. These services, commonly known as Buy Now, Pay Later (BNPL), offer consumers newfound flexibility and control over their purchasing power.

Now at retailers like Sephora, Urban Outfitters, as well as airlines and online boutiques called “Instastores,” the chance to pay in interest free installments is a routinely offered option at checkout. Modern BNPL platforms provide transparency and convenience, empowering consumers to make informed financial decisions and offering much needed competition to traditional leasing agreements or layaway options.

The BNPL market is growing rapidly, jumping from a $2 billion origination (new financing offering) for the five biggest firms in 2019 to $24.2 billion in 2021. BNPL was virtually unheard of 10 years ago, but now is nearly ubiquitous at online stores, which reflects this massive increase in scale. The industry is undoubtedly experiencing a boom, and as a result regulators and many State Attorneys General are paying attention to, and probably planning on meddling in, this formerly niche fintech space. State and federal officials should be cautious when considering new regulations in case they diminish consumer access to a helpful budgeting tool.

A 2023 report from the Consumer Financial Protection Bureau (CFPB) looked at consumer data from the five biggest BNPL firms and showed that consumers use BNPL tools differently from a typical credit card or other short term loan.

While concerns persist that BNPL users might be stacking loans or carrying credit card debt simultaneously, data suggests that BNPL users pay off their bills reliably. Only 10.5 percent of BNPL users have been charged a late fee, and only 3.8 percent of fees are considered charge-offs, meaning uncollectable or delinquent.

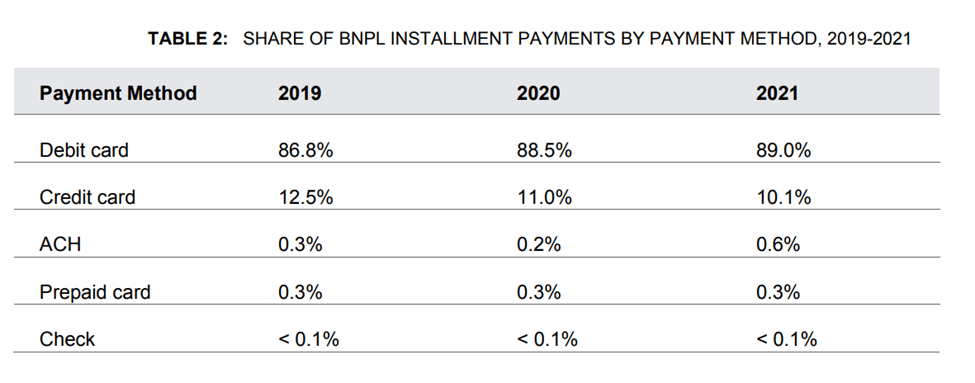

This is because nearly 89 percent of BNPL purchases are linked to debit cards, meaning they are tied directly to users’ available funds, not to extended lines of credit. In contrast, 21 percent of Americans have incurred a credit card late fee in the past year, and 47 percent of Americans have carried a balance at least once in the past year. In the CFPB report, which was largely critical of BNPL services, the Bureau had to acknowledge that, “BNPL imposes significantly lower direct financial costs on consumers than legacy credit products.”

This responsible borrowing seems to have been built into the product by design. The Founder and CEO of the BNPL company Afterpay, Nick Molnar, spoke to the consumer motivation for using BNPL instead of a traditional credit card, saying, “[I]t’s not widely spoken about, but the whole genesis is the global financial crisis in 2008. It hit some millennials that just turned 18 and it was, ‘don’t spend money that you don’t have…’ In the U.S., two out of three people aged 18 to 30 don’t own a credit card. They use debit cards. This is their form of budgeting.”

Molnar also noted that, “85% of our customers use debit cards.” His observation matched the trend observed by CFPB at other BNPL firms:

Another major BNPL firm, Klarna, detailed how they design their loans so they are likely to be paid back in an annual report:

“When a consumer chooses [a BNPL lender] for the first time, we give consumers a small line of credit, usually around $100. Then we do a new assessment for each and every transaction they make. We see that consumers can use the product responsibly before we make small increases in the amount available to them. This is why 99 percent of our lending is repaid and our losses are below the card industry standard.”

One might ask, if most BNPL users pay off their bills on time and are not charged interest or late fees, how do companies make money?

The answer is that, among other revenue sources, the lion’s share of BNPL revenue comes from the “merchant discount fee.” BNPL firms receive a negotiated percentage of each transaction, typically ranging from 3 to 6 percent. Merchants are willing to accept this fee because, without the payment plan, the customer is unlikely to make the purchase at all.

BNPL services represent a significant advancement in consumer finance. Instead of relying solely on layaway or lease-to-own stores, which have historically been prevalent in low-income communities, consumers now have more ways to purchase available to them. Those stores also come with their own problems. Recently, the CFPB announced the distribution of over $191 million to consumers harmed by a leasing firm that operated at stores including Sears and Kmart. The CFPB found that customers didn’t receive important information about their loans during transactions, possibly due to errors by salespeople. This shift towards BNPL enhances purchasing power and offers a wider choice of retailers.

To be sure, there are likely some quirks to be smoothed out in this relatively new fintech tool. Consumer credit laws vary slightly by state, affecting licensing and registration. In some states, BNPL providers partner directly with banks to issue loans. Although, to be clear, regulatory difference does not mean there is a need for national uniformity.

This financial tool, like every financial tool, requires personal responsibility. The temptation to overspend can lead to unintended consequences, such as late fees or accumulated debt. Therefore, consumers must understand their financial situation and the terms of the agreement they are entering into.

As one fictitious blue-collar worker famously advised his nephew, with great power comes great responsibility; consumers must manage their finances vigilantly to fully leverage the benefits these services offer. Regulators would be well advised to let this process happen naturally.