HSAs: A silver bullet for the silver loading conundrum

Photo Credit: Getty

After the longest government shutdown in American history — ostensibly caused by the expiration of the expanded Obamacare subsidies — Republicans have debated health care policy and potential reforms to the individual market for health insurance. To date, only one bill has passed: the Lower Health Care Premiums for All Americans Act.

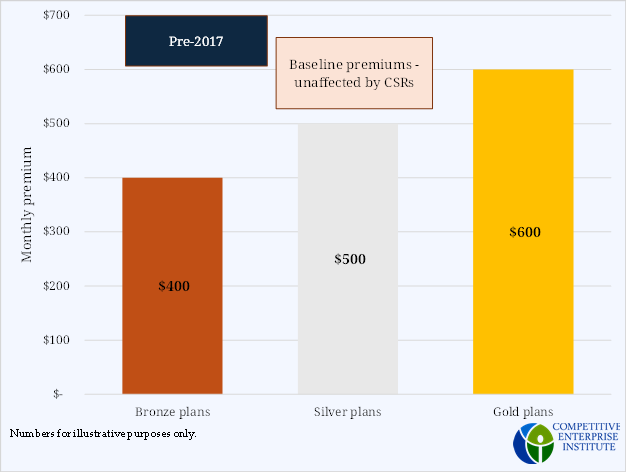

Among other provisions, the bill would directly fund the lesser-discussed Obamacare subsidy — the cost-sharing reduction (CSR) subsidy. While the subsidies for insurance premiums receive most of the coverage, the Affordable Care Act also required insurance companies to cover a portion of beneficiaries’ out-of-pocket costs. This additional subsidy was only available to individuals earning less than 250 percent of the federal poverty level (while premium subsidies were available for people earning up to 400 percent) and to those who chose a Silver plan. Enrollees in Gold or Bronze plans were ineligible.

Initially, the law directed insurance companies to provide this benefit and the federal government would reimburse them. However, because the Affordable Care Act didn’t specifically appropriate funds to make these payments to the insurance companies, many — including President Obama’s Treasury counsel and a District Court — believed they were unlawful.

In October 2017, President Trump discontinued the payments. Since the underlying law did not change, though, insurance companies were still required to cover the same percentage of eligible beneficiaries’ out-of-pocket costs. As a result, insurers were no longer reimbursed and were forced to absorb the costs themselves. But since insurance companies, like any business, cannot absorb losses indefinitely, they raised prices to cover their additional costs. In this case, those higher prices came in the form of higher insurance premiums.

Silver loading explained

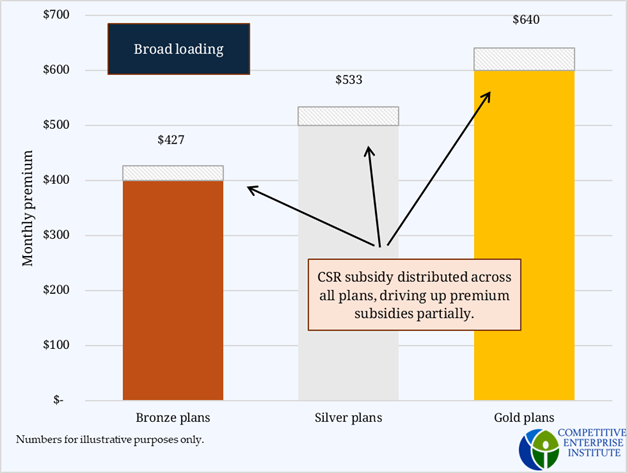

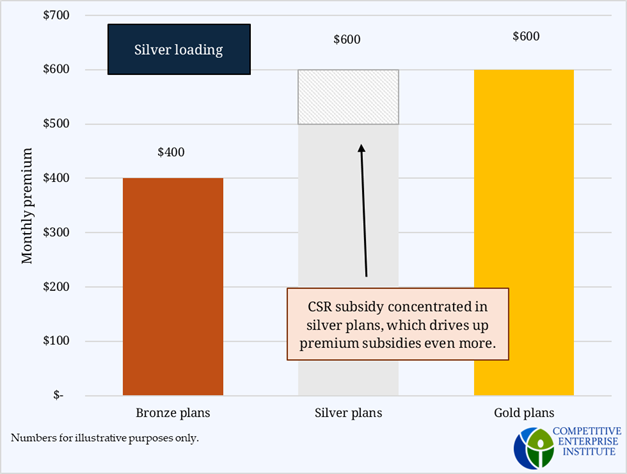

Insurers then faced a choice on how to pass these costs on to consumers: they could spread the costs across all customers, known as “broad loading,” which would cause premiums to go up for all customers, across all metal levels — Bronze, Silver, and Gold — or they could engage in so-called “silver loading” where they concentrate the cost of providing the out-of-pocket subsidies entirely within Silver plans, making premiums for Silver plans, and only Silver plans, go up.

The problems with silver loading

Both broad loading and silver loading lead to an increase in government spending even though the subsidies are no longer directly funded. The reason taxpayers still end up footing the bill is because the premium subsidies are tied to the Silver plans, and if the premiums for Silver plans increase, the subsidies increase. In fact, with silver loading, increased premium subsidies generally cost taxpayers even more than direct funding of the CSR subsidies would have.

Because premium subsidies are benchmarked to the second-cheapest Silver plan and because the premium subsidies are available to a wider range of beneficiaries (Gold and Bronze enrollees and enrollees with incomes), the unfunded CSRs end up costing taxpayers more money than had they been funded.

Republicans have twice attempted to address this issue, first in 2017 and again in 2025, but in both cases the change was ruled incompatible with Senate rules and abandoned. On the other hand, many politicians want to keep these CSRs unfunded because it leads to higher subsidies. These particularly include state policymakers, some of whom have explicitly directed insurance companies to practice silver loading because it boosts total subsidies. As with other federal subsidy programs, this approach benefits these policymakers’ constituents at expense of other states’ taxpayers. For national policymakers, there is evidence that the higher subsidies boost overall enrollment.

While some may prefer the indirect subsidy increase because it raises the proportion of the population with insurance, silver loading should still be replaced with more direct approaches. For one, silver loading is distortive. It sways both enrollees who receive the CSRs and those who don’t.

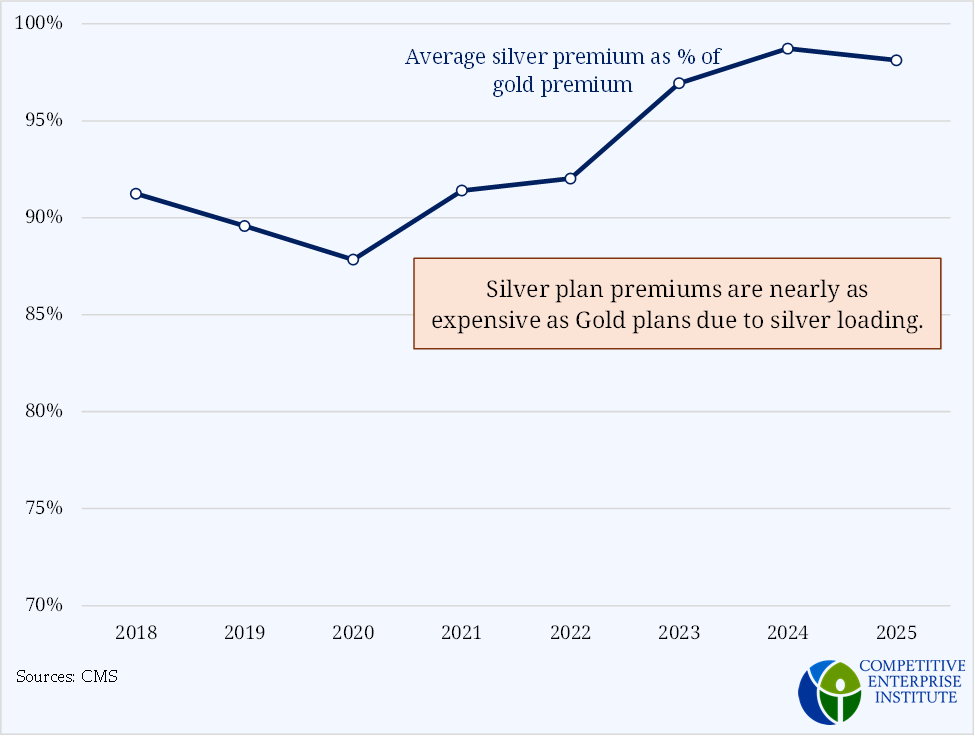

One of the ways it distorts choices is by changing the relative prices of the different plans. Bronze, Silver, and Gold plans were designed to help consumers choose between high upfront/low point-of-sale costs (Gold) versus low upfront/high point-of-sale costs (Bronze). In the case of health insurance, Gold plans have higher premiums but lower copays, while Bronze plans have lower premiums and higher copays. Silver falls in the middle. But because of silver loading, the premiums for Silver plans are approaching those of Gold plans, upending the intended structure and operation. In some states, Silver plan premiums have surpassed Gold.

Consumers who don’t receive the cost-sharing reductions shift to Gold or Bronze plans even though they may prefer Silver plans. For those who are eligible, the subsidies cause them to gravitate toward Silver plans even though they might prefer Gold or Bronze.

Second, it is an inefficient use of taxpayer money to achieve a goal. If boosting insurance is the goal, it can be done more efficiently than by telling insurance companies they have to subsidize a subset of customers using a subset of plans which raises premiums for that plan in unpredictable ways which themselves get filtered through MLR requirements, age-banding, etc., which then raises subsidies for everyone.

Third, fraud is widespread in these exchange plans. Huge amounts of money are going to people who do not qualify for these subsidies and may not even receive insurance at all. Boosting the subsidies increases this fraudulent spending.

Proposed reforms

The simplest fix is to fund the CSRs via direct government appropriation. This is the original intent of the statute and how President Obama administered the CSRs. Doing so would substantially reduce overall spending and return the program to its congressionally approved limits. However, it would not address the distortionary element that pushes CSR recipients into Silver plans.

To address that problem, there are two potential solutions. One is to remove the stipulation from the law that limits the CSRs to Silver plan enrollees. Because these CSRs are meant for low-income people, it would seem preferable to make them available to enrollees regardless of what plan they chose. The likely reason this was not done originally is that it would make the system much more complicated.

As originally written, CSR-eligible enrollees within the Silver tier receive plans with a different actuarial value than what is standard. While the standardized actuarial value for Silver plans is 70 percent (i.e., premiums pay for 70 percent of the enrollee’s health costs and the enrollee pays the remainder out of pocket), with CSRs, that actuarial value can be 73, 87, or 94 percent. Extending CSRs to other metal tiers would necessitate multiple actuarial values across all tiers, significantly increasing administrative complexity.

Another option would be to eliminate CSRs altogether, simplifying the system. Funds currently spent on CSRs could be redirected to premium subsidies for the same population to ensure they are not worse off. With greater premium subsidies, enrollees would be free to choose a higher metal tier with higher actuarial values that replicate the CSRs. Some health care experts, however, worry that beneficiaries might choose lower-tier plans to save money on premiums, but then expose themselves to higher out-of-pocket costs, which could lead them to forego necessary care.

While that fear relies on confidence in government judgment over individual choice, even that problem could be solved with Health Savings Accounts (HSAs). Rather than redirecting CSR funds to premium subsidies, that money could be deposited into enrollees’ HSAs, which they would be able to use for out-of-pocket payments. This solution seems to address all criticisms. This change would:

- Simplify Obamacare, correcting the complexity introduced by restricting CSRs to Silver plans

- Maintain the subsidy levels according to income as originally written

- Ensure the funds are available for cost sharing

- Eliminate the incentive for silver loading

- Lower overall subsidies and waste

- Reduce distortionary effects

Silver loading represents a national failure of health care policymaking and reflects states’ appetite for drawing additional taxpayer funds to benefit themselves. There’s a straightforward solution that could satisfy everyone who cares about good policy and Congress should take it up.