Is Shareholder Activism Surging or Peaking?

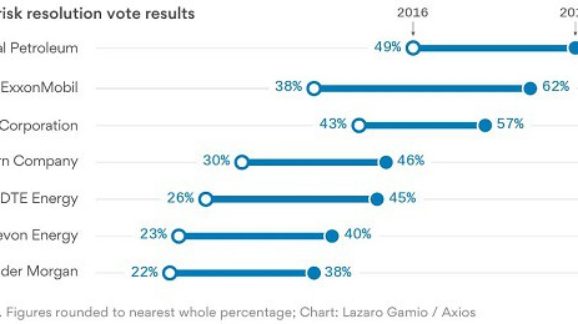

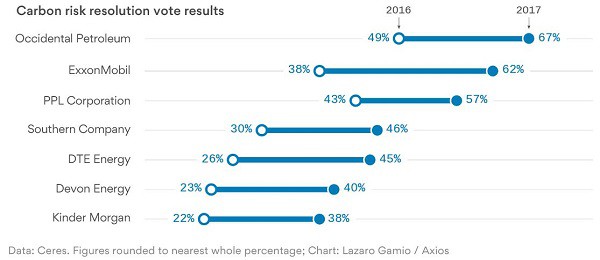

“A record number of investors are pressuring fossil-fuel companies to reveal how climate change could hit their bottom lines,” energy analyst Amy Harder of Axios reports. The chart below shows the shift in shareholder voting between 2016 and 2017. It also shows three recent victories for shareholder activists. Two major oil companies, Occidental Petroleum and ExxonMobil, and a mostly coal- and gas-fired electric power producer, PPL Corporation, approved resolutions to “stress test” how their portfolios will perform under climate policies designed to limit global warming to below 2°C.

Surge or Peak?

The shifts depicted in the chart could be a sign of things to come. Alternatively, we could be seeing the crest of a movement juiced by the expectation that Hillary Clinton would become president, implement the Clean Power Plan, and ramp up U.S. climate “ambition” under the Paris Agreement.

The shareholder resolutions approved by Occidental, ExxonMobil, and PPL all specifically invoke the Paris Agreement and its goal to hold warming to below 2°C. Other sources indicate that the Paris Agreement energized the whole socially-conscious investor movement. JustMeans.com reports:

More 2016 shareholder proposals than ever before address climate change—94 compared with 82 in 2015. Of the resolutions, 22 ask energy extractors and suppliers to detail how the warming planet will affect their operations and how they will respond if governments follow through with commitments made in the Paris climate treaty in December to keep fossil fuel assets in the ground to prevent damaging temperature increases.

Shareholder activism will no doubt feed off the “We Are Still In” campaign led by former New York City mayor Michael Bloomberg—a coalition of large companies and state and local officials pledging to implement the Paris Agreement despite President Trump’s decision to withdraw. However, climate talk is cheap. In 2007, Bloomberg led a coalition of 1,000 mayors pledging to comply with the Kyoto Protocol regardless of President George W. Bush’s policies. “When Kyoto’s 2012 carbon-reduction deadline arrived, however, virtually all these cities had failed to live up to the pledge their mayors had made, missing the Kyoto targets badly,” reports Todd Myers of the Seattle-based Washington Policy Center.

One of Harder’s sources, Kevin Book of ClearView Energy Partners, argues that corporate leaders are taking climate risk more seriously than ever, and are doing so in spite of Trump: “Investment risk is increasing, and investors care—not because they believe or don’t believe in climate change—but because they care about the value of their investments. The issue doesn’t go away just because Trump came to Washington.”

Moody’s announced in June 2016 that it “would consider the carbon-reduction pledges in the Paris climate deal when it rates fossil-fuel companies,” and Fitch Ratings is “now discussing to what extent to consider carbon risk more explicitly in its processes,” Harder reports. However, she also acknowledges that “by repealing Obama-era regulations on climate change and withdrawing from the Paris deal, Trump is taking away explicit policies for credit agencies to use in their ratings.” That means he is also reducing investment risk.

Note, too, that fear of climate-related regulations, taxes, and prosecution is largely responsible for whatever limited success shareholder activists have achieved. Trump seeks to dispel that fear, championing the American people’s freedom to develop the nation’s energy treasure. Elections matter.

Shareholder Value Con Game

Sponsors of the 2°C resolutions claim their goal is to “protect shareholder value.” But as chairman Bob taught an earlier generation of activists, you don’t need a weatherman to know which way the wind blows. Exxon’s shareholders don’t need “stress tests” to see financial peril in policies designed to suppress the production, transport, and consumption of the company’s products. As is also obvious, the shareholder-value scolds are among the most vociferous proponents of the “keep it in the ground” policies creating the financial risks they demand the companies divulge.

There’s a con game going on here. The shareholder activists lobby for policies that would bankrupt fossil energy companies. Then, they pressure the companies to report the financial risks those policies entail. As Harder puts it, “the ultimate goal of these symbolic resolutions is to show fossil-fuel based companies their current investments won’t work in a carbon-constrained world.” The activists hope such disclosure will hasten the targeted company’s demise, in three ways.

First, the reports—hailed by campaigners as confessions of financial unsustainability—will tend to scare away investors, depressing stock values. Second, activist attorneys general and others in the eco-litigation fraternity will cite the reports as proof the companies have defrauded shareholders by “hiding climate risk.” Third, as the targeted firms dwindle in wealth, market share, and number, so will their ability to defend themselves against further litigation and regulation.

It’s Not Working

However, I’m betting investor activists won’t have much impact on energy markets, for two reasons. First, fossil fuel companies are more resilient, both financially and legally, than the activists imagine. Touting the theory that ExxonMobil invests shareholder dollars without due consideration of climate risk, New York State Attorney General Eric Schneiderman obtained and recently published documents estimating the impacts of carbon pricing on the oil giant’s finances. In 2014, the company forecast that carbon prices in industrial countries would reach $60 per ton in 2030 and $80 per ton in 2040. In an interview with Climatewire reporter Benjamin Hulac, Carbon Tax Center director Charles Komanoff stated:

This document seems to me either on the curve or ahead of the curve, rather than behind the curve, in actual world carbon pricing. This four-page document doesn’t seem to me to be a smoking gun saying that they weren’t looking soberly and seriously at current and near-future carbon pricing.

Moreover, Schneiderman’s 16-month investigation isn’t going well, as Katie Brown of Energy In Depth reports. During court proceedings, Justice Barry Ostrager, after reminding Schneiderman’s team that ExxonMobil had turned over 2 million documents, complained: “I think you are wasting my time.” The Judge’s exasperation may have something to do with the AG’s office continually changing the investigation’s rationale. Brown explains:

Exxon’s lawyers pointed this out, noting that first the investigation was about what Exxon supposedly knew about climate change in the 1970s; when that went absolutely nowhere, they turned to stranded assets. When that was a huge flop, they decided that Exxon was actually inflating the risks of climate change. It’s no wonder Justice Ostrager was losing his patience.

Schneiderman’s Exxon probe was to be the big breakthrough case for the shareholder activist movement. So far it’s been a bust, and most of the other “AGs United for Clean Power” have slinked away from Schneiderman’s crusade.

Second, Trump has repudiated Obama’s anti-fossil energy agenda. Although “progressive” pundits and investors may view Trump as no more than a bump on the road to a carbon-constrained future, fossil fuel CEOs and investors can plainly see he has their back and means to protect them from regulatory predation. That should make the CEOs bolder about standing up for their shareholders’ real interests.

Ultimately, I believe, the decisive factor will be the success or failure of Trump’s economic program. If Trump’s deregulatory and tax-cut initiatives boost annual GDP growth to 3 percent, there won’t be much enthusiasm for pro-Paris agitation in either corporate board rooms or the public square.