Let Private Markets Assess the Financial Risks of Climate Change

Photo Credit: Getty

In her opening remarks this week to the Financial Stability Oversight Council (FSOC), Treasury Secretary Janet Yellen identified climate change as the “big” “emerging risk” facing the nation’s financial system. She explained:

[Climate change] is an existential threat to our environment, and it poses a tremendous risk to our country’s financial stability. We know that storms will hit us with more frequency, and more intensity. We know warming temperatures might disrupt food and water supplies, leading to unrest around the world. Our financial system must be prepared for the market and credit risks of these climate-related events. But it must also be prepared for the best-possible case scenario: that we begin a rapid transition to a net-zero carbon economy, which also creates potential challenges for financial institutions and markets. On all these fronts, the Council has an important role to play, helping to coordinate regulators’ collective efforts to improve the measurement and management of climate-related risks in the financial system.

The operative phrase here is “coordinate regulators’ collective efforts.” It suggests an ambition to centrally plan lending practices throughout the financial sector.

Her rationale is not supported by evidence. “We know that storms will hit us with more frequency”? Actually, we don’t know that. University of Colorado Professor Roger Pielke, Jr. reports that since 1945, the number of hurricanes that made landfall in the North Atlantic and Western Pacific, which account for about 70 percent of all landfalling hurricanes, declined by one third. Since 1973, there has been considerable annual and decadal variability, but no long-term trend of increasing global tropical cyclone frequency (Dr. Ryan Maue, December 31, 2020). Since 1900, there has been no trend in the strength or frequency of U.S. land-falling hurricanes, and none in hurricane-related damages once losses are adjusted for changes in population, wealth, and inflation (Klotzbach et al. 2018). Modeling studies mostly suggest a future of decreasing hurricane frequency, albeit combined with an increase in the proportion of major (category 4-5) hurricanes (Cha et al. 2020).

“We know warming temperatures might disrupt food and water supplies, leading to unrest around the world.” Well, lots of bad stuff “might” happen over the next 80 years. There is no empirical basis for the disaster scenario Yellen invokes. Despite climate alarms going back to the 1980s, global crop yields and per capita food supply keep increasing. Since 1990, more than 2.67 billion people gained access to improved water sources.

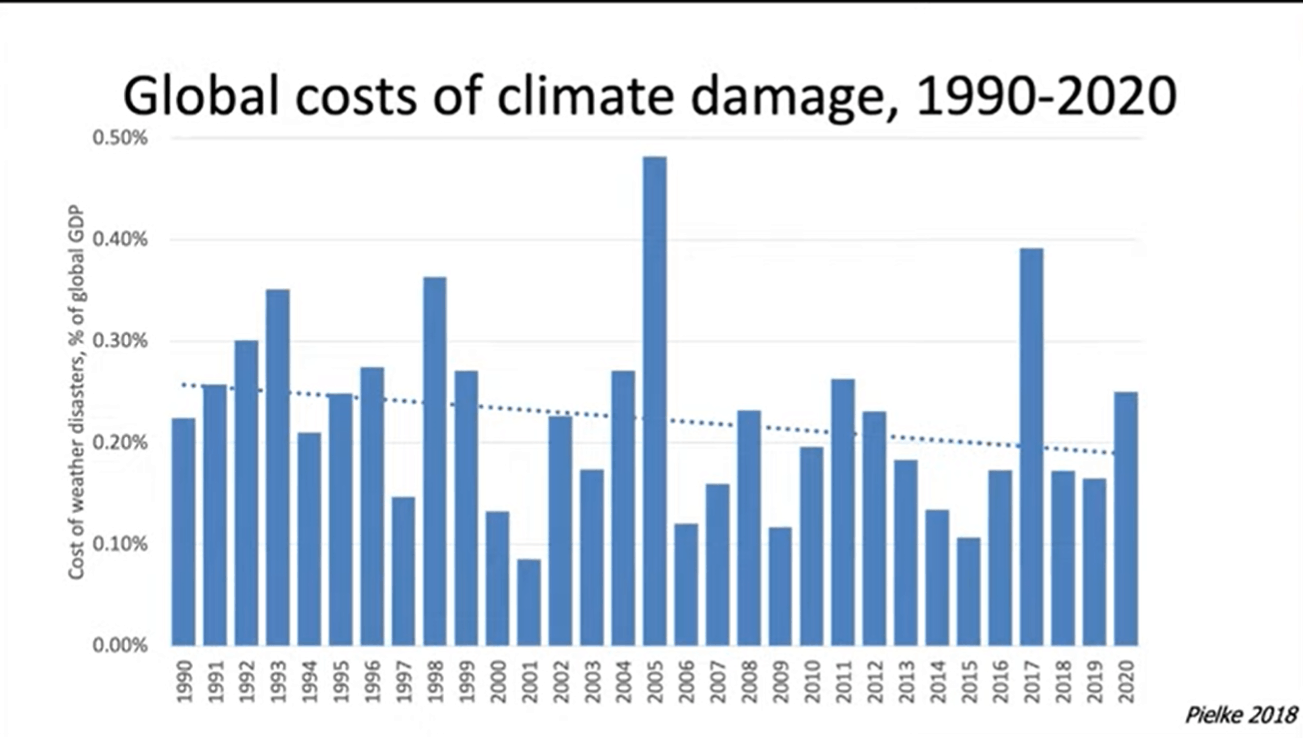

More broadly, although extreme weather damages keep increasing along with population growth, property values, coastal construction, and the consumer price index, the relative economic impact has declined from about 0.26 percent global GDP in 1990 down to about 0.18 percent in 2020.

The Senate Banking Committee held a hearing on March 18 titled “Protecting the Financial System from Risks Associated with Climate Change. ” Secretary Yellen should read the testimonies of American Enterprise Institute economist Benjamin Zycher and Hoover Institution economist John Cochrane.

Zycher warned that coercing banks to discriminate against carbon-intensive industries would damage the economy as well as our legal and constitutional institutions:

Proposals that the Federal Reserve enforce a mandate that financial institutions evaluate climate “risks” represent a blatant effort to distort the allocation of capital away from economic sectors disfavored by certain political interest groups pursuing ideological agendas. This would represent the return of Operation Choke Point, a past attempt to politicize access to credit, one deeply corrosive of our legal and constitutional institutions.

For those who may not remember Operation Choke Point, see my colleague John Berlau’s 2018 retrospective.

Choke Point was a multi-agency operation in which several entities engaged in a campaign of threats and intimidation to get the banks that they regulate cut off financial services—from providing credit to maintaining deposit accounts—to certain industries that regulators deemed harmful to a bank’s “reputation management.”

Legitimate businesses engaged in wholly legal activities such as coin dealers, gun shops, and payday lenders suddenly found their access to banking services cut off. Choke Point was never authorized by an act of Congress. It was not even adopted through a public notice-and-comment rulemaking. It was implemented by guidance documents advising banks to shun customers deemed (by the regulators) to be persons or entities of ill repute.

Needless to say, companies engaged in producing fossil fuels and building fossil energy infrastructure have long been subject to a vilification campaign. That campaign arguably creates “reputation risk” for banks that dare to finance fossil fuel companies. Not coincidentally, climate campaigners have long put pressure on banks to terminate such financing. The Biden administration makes no secret of its desire to drive capital out of the fossil fuel industry. Denying the industry access to financing would scare away investors in droves.

At the Senate Banking Committee hearing, Sen. Cynthia Lummis (R-WY) asked the five expert witnesses whether Operation Choke Point damaged the U.S. financial system. Zycher replied:

I think operation Choke Point was deeply corrosive to the rule of law and our constitutional institutions. It was a blatant attempt to bypass Congress and implement a politicized allocation of credit in a way that disfavored politically unpopular industries.

The other witnesses professed not to know enough detail to answer the question, although Gregory Gelzinis of the Center for American Progress opined that “it is important to remember that reputational risk is financial risk.” Reputational risk is a wholly circular construct. Proponents define “reputation risk” as banking services sold to certain sectors, and then conclude that such business relations threaten banks’ reputations. The Senators should also remember that proponents seek to damage the reputations of fossil fuel companies and the banks that finance them.

Cochrane of the Hoover Institution disputed the hearing’s core premise (which is also Yellen’s) that climate change poses a measurable risk to the financial system:

Sure, we don’t know what will happen in 100 years. But banks did not fail in 2008 because they bet on radios not TV in the 1920s. Banks failed over mortgage investments made in 2006. Trouble in 2100 will come from investments made in 2095. Financial regulation does not and cannot pretend to look past 5 years or so, and there is just no climate risk to the financial system at this horizon.

What would Secretary Yellen say to that? During the FSOC meeting she chaired, staff of the Federal Reserve System Board of Governors briefed the Council about “climate change and its potential impact on financial stability.” Unsurprisingly, no one was invited to present a skeptical counterpoint.

A partisan echo chamber is a poor basis for imposing discriminatory financing rules on the financial sector. A smarter approach would be to just let people with skin in the game assess for themselves how much risk climate change or climate policy poses to particular loans or lending practices. Zycher puts the point as follows:

Because the uncertainties attendant upon the future effects of increasing atmospheric concentrations of greenhouse gases are so great, a top-down policy approach for the evaluation of any attendant risks is itself very risky. A wiser approach would entail allowing market forces to make such “risk” determinations in a bottom-up fashion, thus avoiding an obvious politicization of the allocation of capital. It is reasonable to hypothesize that the market in its atomistic fashion has decided that it is the sum of decisions by financial institutions and investors that is the more reliable gauge of the highly uncertain business implications of evolving climate phenomena.