Sustainability Disclosures, Meant to Protect, Could Create Additional Risk for Investors

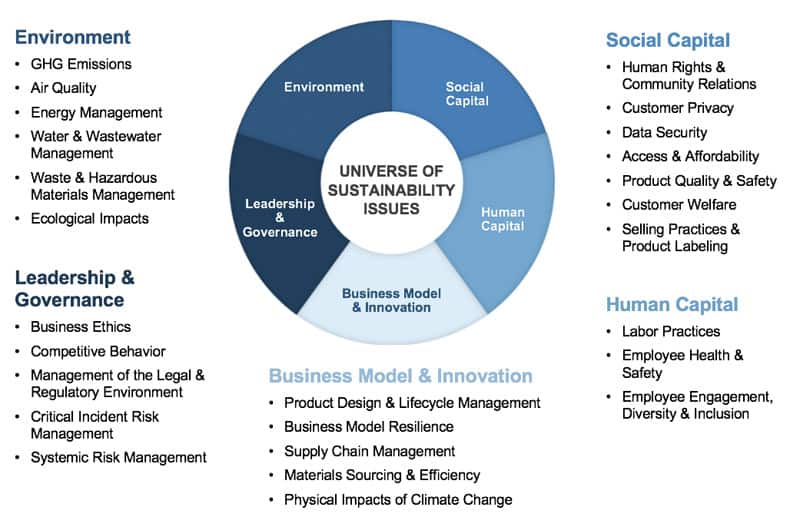

The lead editorial in Tuesday’s Wall Street Journal took on the Sustainability Accounting Standards Board (SASB), a non-governmental body that “issues guidelines for what kinds of sustainability information corporations should report to investors.” In the context of the SASB, the umbrella of “sustainability” covers a lot of territory, not just the environmental issues most frequently associated with that term. The board also tells companies how they should be managing data security, supply chains, and employee diversity.

The SASB claims that it focuses on issues that are “financially material” to the companies they are assessing—that is, information that would substantially influence whether a particular investor would choose to buy a particular stock. If these notional investors are going to make informed decisions, the argument goes, then responsible companies need to pony up the detailed disclosures that the SASB recommends. But materiality is in the eye of the beholder.

Critics of the SASB—and other environmental, social, and governance (ESG) guided analyses of corporate management—would say that very few, if any, investors actually care about many of the detailed sustainability topics that companies are supposed to provide disclosures on. Instead, many of the topics line up better with the agendas of left-wing advocacy groups that are hostile to market economies in general. In other words, SASB-style disclosures seem like they are devised to give ammunition to anti-corporate activists as much as they are to protect actual investors.

But even if that were true, the Machiavellian financial advisor might say, those risks are still real. If an international coalition of environmental NGOs looks like it’s about to persuade policy makers around the world to adopt policies that would make the oil business less profitable, then sustainability disclosures for energy companies need to assess and report on that political risk.

That’s fair enough, as long as the threat is real and not merely an aspirational one among said NGOs. But that’s precisely the problem with a big institutional framework like the SASB. It can be used to create and increase the very risks it’s supposedly warning investors about. It would be like an infectious disease research institute inviting thousands of coughing influenza patients to a medical conference. You might learn a lot about the latest flu strain, but you would certainly also spread the contagion.

There are some investors who only want to invest in companies that are carbon neutral. There are probably also some investors who are only interested in companies led by a CEO who is a Christian, a non-drinker, or an Aries. The problem arises when we have to decide which of these are simply matters of preference among investors and which are the “correct” characteristics for a company to have. The ESG advocates want everyone to agree not only that SASB-style disclosures are of interest to potential investors, but that there is only a single position on each issue that is the correct and defensible one. And that’s not an investor awareness project for minimizing risk—that’s an ESG activist project that is going to create expensive new liabilities.

But should we really be worried if the SASB and similar entities are merely issuing voluntary guidelines? That status may not last long. As the Journal editors point out, the SASB’s goal is to have the Securities and Exchange Commission incorporate its recommendations. And in their defense, that’s the only long-term strategy that makes any sense for the SASB. The more strict standards of operation become for SASB-compliant companies, the more money they’ll be leaving on the table by not pursuing otherwise profitable lines of business. That’s going to attract wildcat players who don’t care whether they’re on the list of “100 Most Sustainable Companies” or are invited to corporate executive symposia on ESG leadership.

The only way to keep the social justice industry leaders from having their lunches eaten by new entrants will be to make it illegal to do business any other way. There’s no logical middle path between leaving firms free to invest according to their own standards and requiring them to do it the activist-approved way.

It’s going to be a showdown.