The problem with Obamacare is Obamacare

Photo Credit: Getty

This year, the COVID-induced expansion of the Affordable Care Act (ACA) will expire. Extending the expanded subsidies has become a point of contention between Republicans and Democrats, and the clock is ticking. Marketplace enrollees will start choosing their plans in a month.

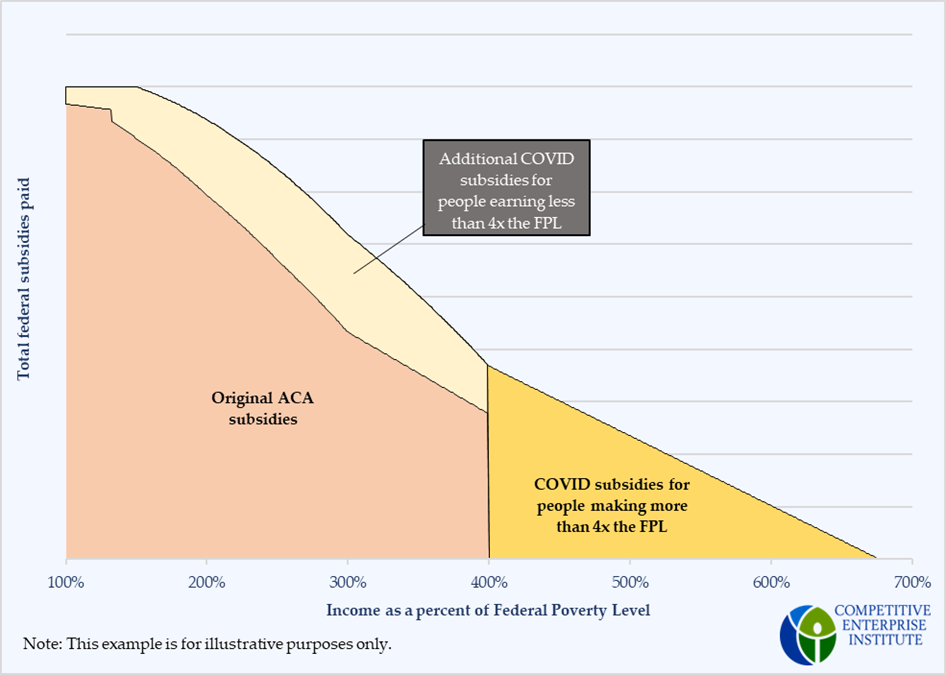

The expansion of ACA subsidies can be broken into two components. Originally, the ACA provided subsidies only for people earning between the federal poverty level (FPL) and four times the federal poverty level (between 100 percent and 400 percent of the FPL for short). Those subsidies decreased with income, so that the higher the income (or, the farther away from poverty), the more the individual was expected to pay, and the lower the taxpayers’ share would be. If a person was in a household that earned more than four times the federal poverty level, there were no subsidies at all.

The COVID expansion of Obamacare/ACA expanded the subsidies in two ways. It increased subsidies for people earning less than 400 percent of the FPL, but for the first time, it also provided subsidies for people above the cutoff. These were designed just as those in the original ACA were, to phase out gradually as income increases.

The figure below illustrates how subsidies would change with income, and how the expanded subsidies compare with those originally legislated.

Today, a major argument from the left to extend subsidies is that people above 400 percent of the FPL cannot afford health insurance without the subsidies.

Those on the right are turning this argument against the ACA itself, saying that it was supposed to “bend the [health care] cost curve downward” and reduce premiums by $2500/year. They argue that if insurance is still not affordable, or less affordable, after more than a decade under the law, then the Affordable Care Act failed at its titular objective.

In fact, the unaffordability of health insurance for people above the cutoff does demonstrate how the ACA failed. One of the reasons the 400 percent FPL cutoff was put in place was that, when the law was written, premiums were much more affordable for this group.

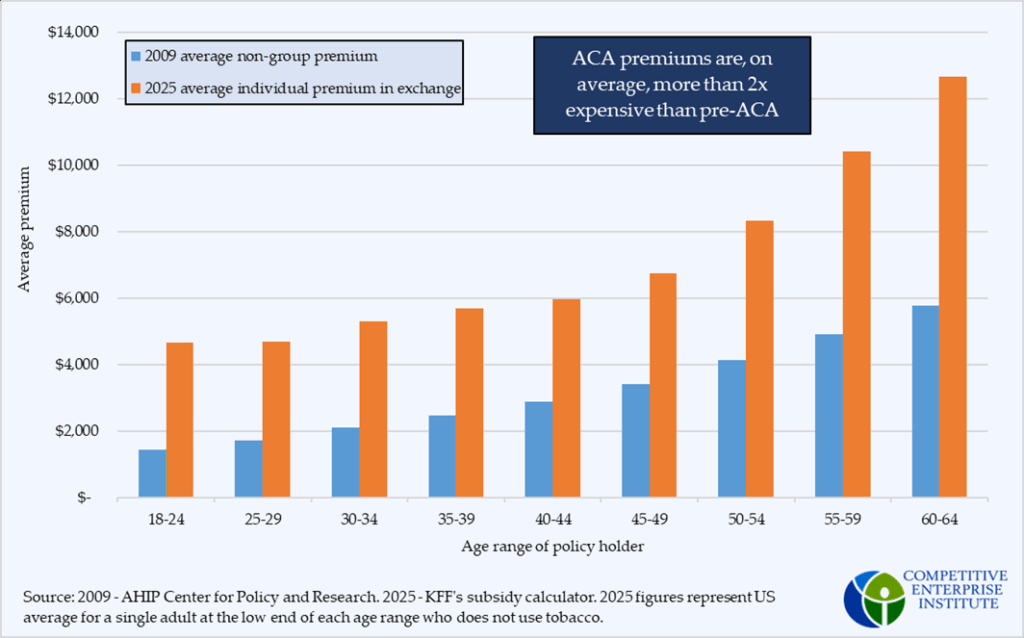

The Affordable Care Act was written primarily in 2009. At that time, premiums for direct purchase insurance were much lower than they are today. According to the a study done by the America’s Health Insurance Plans (AHIP), in 2009, average premiums for non-group insurance plans cost an average of $2,985/yr (all dollar figures are nominal) for individuals, and $6,328 for families. For a 60 year-old individual, the average cost of a policy was $5,755. Across all ages, premiums for marketplace coverage are higher than individual insurance was in 2009.

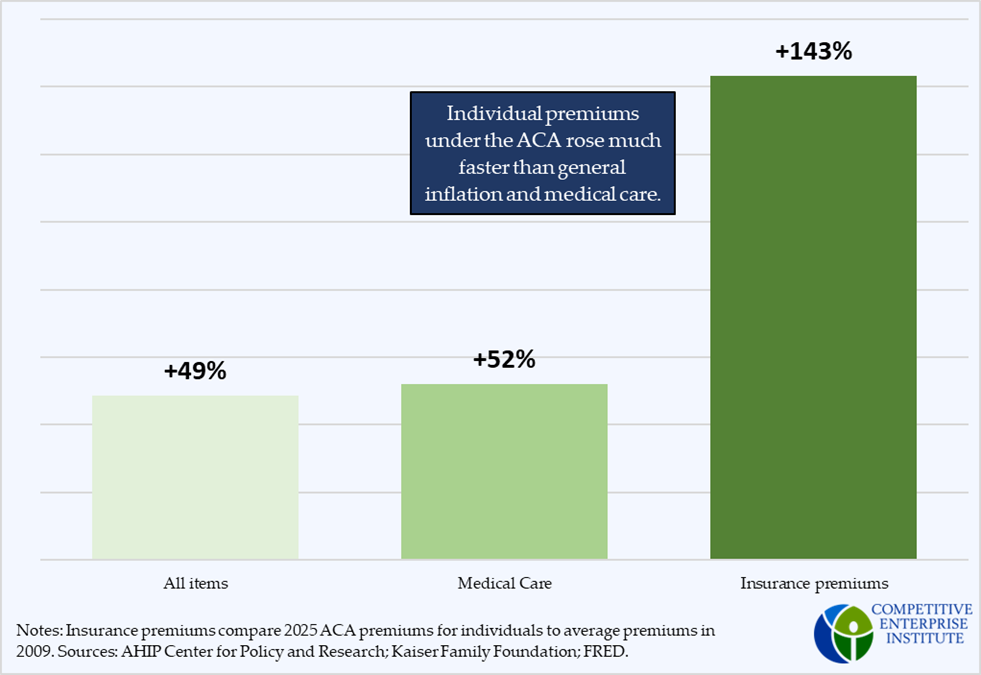

On average, premiums have more than doubled in nominal terms since then. Medical care, notorious for its high inflation rate, has only risen 51 percent and overall prices have risen 49 percent, including the high inflation during the Biden administration.

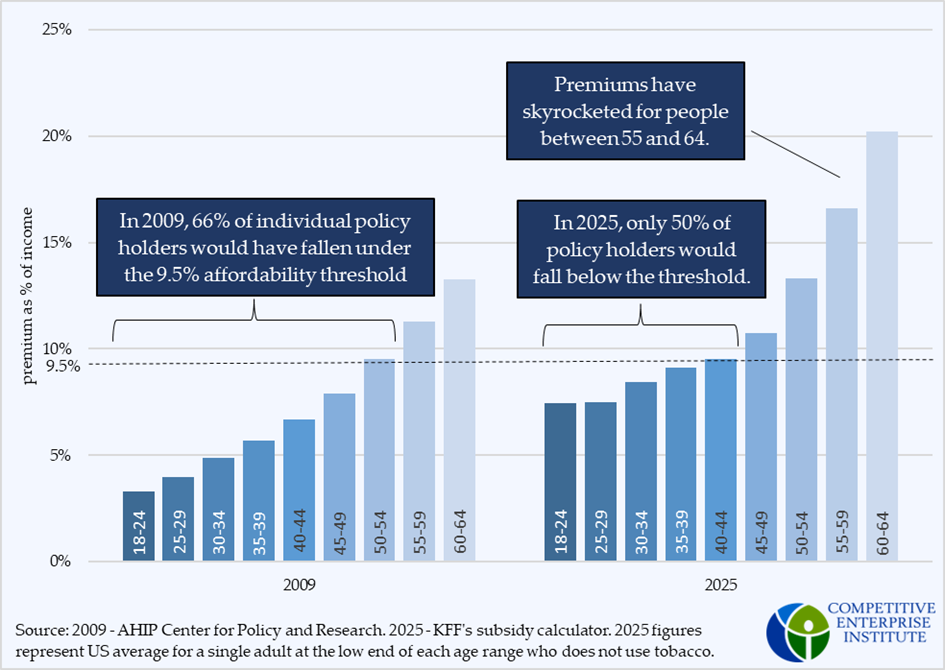

The Affordable Care Act defined affordability as a percentage of income, so to show the failure of Obamacare and why many are saying the cutoff needs to be removed, it is necessary to consider premiums as a percentage of income as well.

In 2009, the poverty level for a single-person family was $10,830. By 2025, it had risen to $15,650. In 2009, insurance premiums amounted to less than 9.5 percent of total income for 2/3 of individual policyholders, which was the “affordability threshold” set for people earning between 300 and 400 percent of the federal poverty level. The ACA could have applied that same level to those above 400 percent, meaning people in this income range would be expected to contribute a larger proportion of their income. It is likely, too, that for people earning more than 400 percent, the ACA would have set a higher affordability threshold than 9.5 percent.

People who could purchase insurance and pay less than the affordability threshold would receive no federal subsidies, because the ACA deemed insurance as “affordable” for these people. Consequently, the architects of Obamacare didn’t believe it was necessary to extend the subsidies beyond 400 percent of the federal poverty level, because few would need them with premiums of the time.

However, once Obamacare went into effect, premiums increased substantially. Now, around half of people at the income cutoff wouldn’t be able to afford insurance, according to the ACA’s affordability standard, and would deserve subsidies under the original Obamacare framework. The increase in premiums between 2009 and 2025 is most evident for people older than 50, which is why Democrats’ examples of unaffordability frequently include these individuals.

If the ACA had worked as promised, premiums would have risen much slower than they have. In fact, premiums have risen so fast, it has undercut the original design of the program, and now, politicians are calling for an expansion. In any context, it is unwise to spend additional money on a failed program without reforming it to fix the underlying problem, and it is no different with the ACA.