CEI Issues Comment to EPA on Greenhouse Gas Emissions and Fuel Efficiency Standards for Medium- and Heavy-Duty Engines and Vehicles

Comments Submitted by Marlo Lewis (Senior Fellow, Competitive Enterprise Institute), Wayne Brough (Chief Economist and Vice President of Research, Freedom Works), Daniel Simmons (Vice President for Policy, Institute for Energy Research), and Karen Kerrigan (President & CEO, Small Business and Entrepreneurship Council).

Docket ID No. EPA–HQ–OAR–2014–0827 and NHTSA–2014–0132

Via electronic delivery to: [email protected]

Re: Greenhouse Gas Emissions and Fuel Efficiency Standards for Medium- and Heavy-Duty Engines and Vehicles – Phase 2

Thank you for the opportunity to comment on the Environmental Protection Agency (EPA) and National Highway Traffic Safety Administration’s (NHTSA) proposed rule Greenhouse Gas Emissions and Fuel Efficiency standards for Medium- and Heavy-Duty Engines and Vehicles – Phase 2. The individuals listed above respectfully present our views in this joint letter. Please direct inquiries about ideas and information discussed herein to Marlo Lewis, Senior Fellow, Competitive Enterprise Institute, 1899 L Street, NW, Washington, D.C. 20036, 202-331-2267, [email protected]

This comment letter develops the following points:

-

The rule threatens the economic viability of small trucking firms, hundreds of which have gone out of business due to increasing regulatory costs. The proposal says not one word about the plight of small truckers or the greater relative burdens it will place on them.

-

Although the ostensible purpose of the rule is to reduce greenhouse gas (GHG) emissions and oil imports, the climate and energy-security benefits of the rule are entirely speculative and vanishingly small at best.

-

Most of the projected benefits are fuel savings for heavy duty vehicle (HDV) owners and operators. However, EPA and NHTSA provide no solid evidence that the trucking industry’s alleged “under-investment” in fuel-saving technology is due to market failure. In fact, some of the agencies’ “hypotheses” suggest that truckers are simply behaving like prudent buyers.

-

As in the Phase 1 rulemaking, EPA and NHTSA ignore a more credible and obvious explanation of the alleged “energy efficiency gap.” EPA’s diesel-engine emission standards, both by directly reducing the fuel efficiency of diesel engines, and by crowding out fuel economy-related R&D investment and consumer spending, created the problem the agencies purport to solve via additional regulation.

-

It may be unrealistic to expect an agency to take responsibility for the very problem it seeks more power over industry to solve. Nonetheless, given the administration’s high-profile commitment to “transparency,” EPA and NHTSA should have at least addressed the issue. They have not done so.

I. The rule threatens the economic viability of small trucking firms.

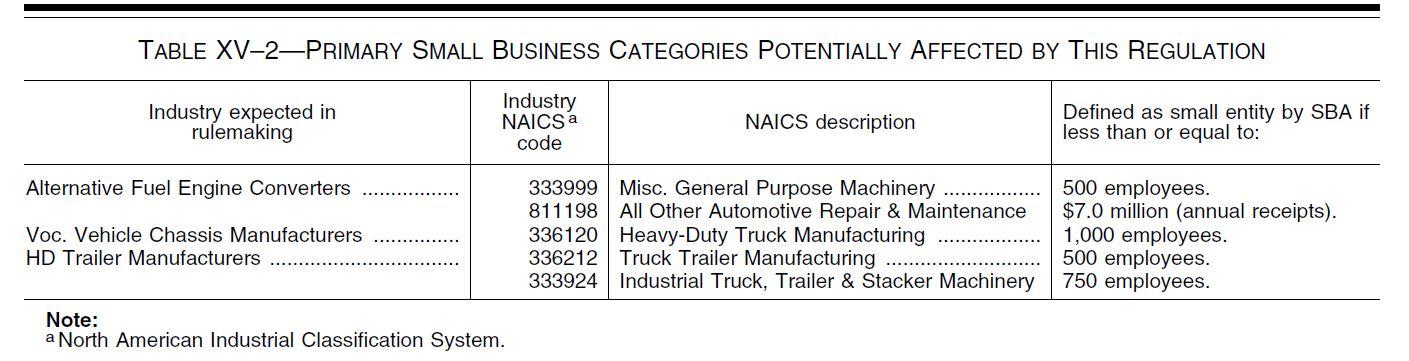

In scores of places, the rule acknowledges that regulations impose a greater relative burden on small firms than on large. Accordingly, pursuant to the Small Business Regulatory Enforcement Fairness Act (SBREFA), EPA convened a Small Business Advocacy Review (SBAR) Panel to consider “flexibility provisions . . . specific to small businesses.” However, in every instance, the entities in question are small manufacturers, not vehicle owners and operators.

Specifically, the agencies propose regulatory flexibilities for manufacturers of box trailers, non-box trailers, non-highway trailers, alternative fuel converters, emergency vehicle chassis, custom chassis, off-road vocational vehicle chassis, and gliders. Not once does the 627-page proposal mention small trucking firms.

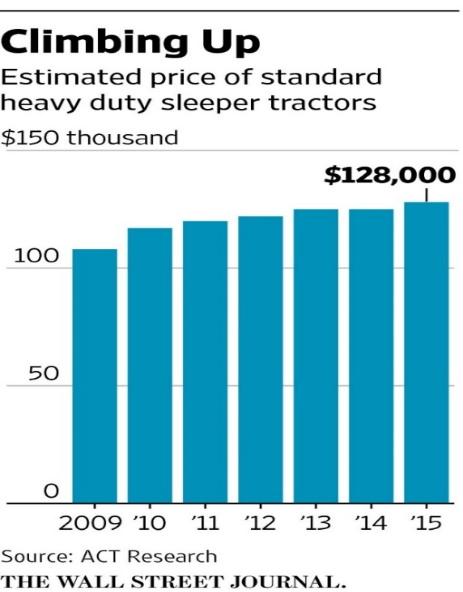

We recognize that the rule’s requirements apply to manufacturers, not customers. Nonetheless, small-business truckers are an important category of stakeholders. As a recent Wall Street Journal article observes, small operators “make up the vast majority of the roughly 470,000 for-hire fleets on the road today.” Indeed, companies “operating six or fewer trucks . . . make up 89% of all fleets.” Although large firms are increasing wages and hiring drivers, new regulations, “including rules capping emissions and limiting drivers’ hours on the road,” are making it harder for small firms to hire workers, raise wages, or even survive:

Small and midsize trucking companies are finding they are ill-equipped to adapt [to the new regulations]. Hundreds of these firms, with an average fleet size of about a dozen vehicles, have gone out of business in the past two years, according to Avondale Partners LLC. Others have sold out to larger competitors, which are more likely to have cash reserves or access to financing to weather changes in the industry.

A chart from the article shows how the cost of new trucks has increased since 2009:

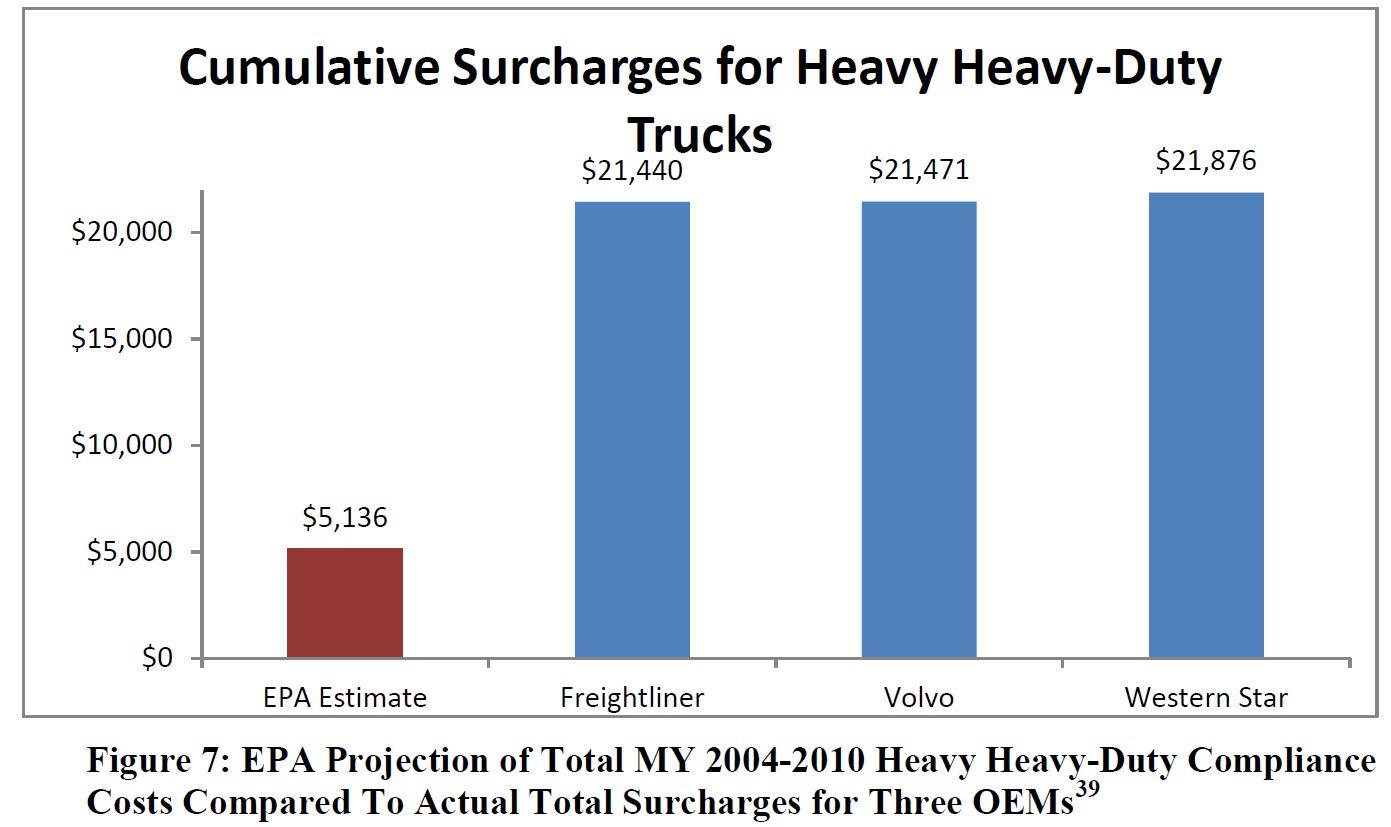

A study prepared for American Truck Dealers (a division of the National Automobile Dealers Association) finds that EPA emission standards adopted in 1997, 2000, and 2001, which phased in between 2004 and 2010, increased the inflation-adjusted cost of new semis by more than $21,000. For each phase of the regulations, the study compares the actual costs with the costs projected in EPA’s regulatory impact analyses. Cumulative actual costs were more than four times bigger than EPA’s estimate.

From January 2000 to January 2015, the CPI increased by roughly 38% while small owner-operator net income increased by 11%. The typical independent owner-operator incurred a loss of $11,260 in purchasing power. Thus, small truckers have been losing ground under existing regulatory burdens.

We urge the agencies to proceed with special consideration for the rule’s impacts on small trucking companies. The agencies claim the rule’s fuel savings will more than offset the higher cost of compliant vehicles. However, even if realized, the projected fuel savings will be of no benefit to firms that go out of business because they can’t afford to buy compliant trucks.

The agencies also show no awareness of the comparatively greater risks small truckers incur from regulation-induced maintenance problems. A large firm with hundreds of vehicles will not lose business when a mandated new technology malfunctions and one or more trucks must be sent to the shop for repairs. But in small firms, such unanticipated downtime can cut weekly income and damage reputations. Consider the experience of owner-operator Tilden Curl, who testified at an EPA/NHTSA listening session in Olympia, Washington:

Curl detailed his truck ownership and fuel economy starting with a 1995 Peterbilt he bought for $65,000. After 10 years with the truck, Curl had invested just less than $95,000 in maintenance and repairs, including a rebuild and transmission. The last year he owned the truck he averaged 6.58 mpg.

In October 2008, Curl purchased a new aerodynamic, emission-compliant 2009 Kenworth for $140,000. In seven years of ownership, Curl drove the truck more than 752,000 miles and had $105,000 in maintenance and repairs. He suffered significant downtime that hurt his income and reputation as a reliable carrier, he told the panel. And, in the end, the truck was only able to achieve 6.15 mpg.

Finally giving up on the ’09 truck, Curl bit the bullet and bought a 2016 Kenworth earlier this year for $167,000. He had originally planned to pay off the 2009 Kenworth and sock away what was the truck payment toward his retirement, he told the panel.

“As I see it, these regulations, and a rush to push technology beyond tested capabilities, have cost me my retirement. There is no mechanism in place to compensate small-business truckers for the costs of these mandates,” he said. “We cannot afford for this to happen again.”

Nowhere in the proposal do the agencies acknowledge EPA’s penchant for low-balling regulatory costs, the precarious economics of small-business trucking, and the existential risks small truckers face when technology mandates impair vehicle reliability. We have been told that EPA consulted OOIDA to address small trucker concerns. However, to all appearances, the rule is a bull in a china shop.

II. The rule’s climate and energy security benefits are vanishingly small at best and completely unverifiable.

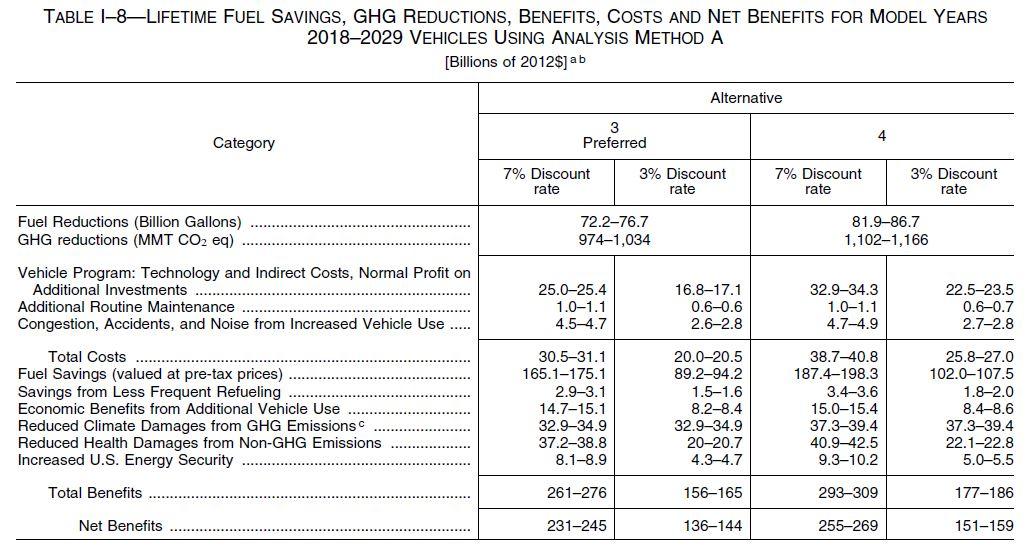

The proposed standards, which phase in during model-years 2021–2027, apply to four types of HDVs: (1) combination tractors (semi-trucks), (2) trailers pulled by combination tractors, (2) heavy-duty pickups and vans, and (4) vocational trucks (a wide-ranging assortment of trucks and buses). The agencies estimate that the technologies needed to comply with the proposed standards will cost $25 billion but that the rule will generate $230 billion in net benefits over the lifetime of vehicles sold in the regulatory timeframe, including $170 billion in fuel savings.

Although the ostensible objectives of the rule are to reduce GHG emissions and oil consumption, the climate and energy-security benefits, if any, are speculative and no one will actually experience them.

Climate Change Impact

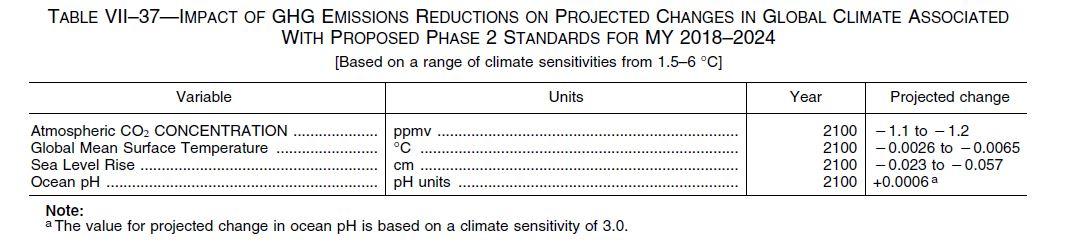

Based on the unverifiable assumption that each ton of carbon dioxide-equivalent (CO2e) GHGs emitted imposes a “social cost” of $37-$77 during 2012-2050 (assuming a 3% discount rate), the agencies project $34 billion in cumulative climate benefits from emission reductions over the lifetimes of the covered vehicles.

Yet the agencies also estimate that by 2100, the rule will decrease atmospheric CO2 concentration “approximately 1.1 to 1.2 parts per million by volume (ppmv).” That miniscule change would, in turn, reduce global mean temperature by “approximately 0.0026 to 0.0065°C” and global mean sea level rise by “approximately 0.023 to 0.057 cm” (depending on whether climate sensitivity is as low as 1.5°C or as high as 6°C). It would also reduce ocean acidification by 0.0006 pH.

Such tiny decreases in global warming and sea-level rise cannot be distinguished from the noise of inter-annual variability. Similarly, the tiny projected decrease in ocean acidification is orders of magnitude smaller than natural inter-seasonal and inter-regional variations. Such changes would have no detectable effect on heat-related mortality, weather patterns, coral calcification rates, or any other climate-related indicator people care about. Hypothetical climate benefits during the lifetimes of vehicles subject to the rule would be even more microscopic. In short, the rule’s multi-billion-dollar climate benefits exist only in the virtual world of integrated assessment models (IAMs) – computer models that combine speculative climatology with speculative economics.

Energy Security Impact

The agencies argue that the “concentration” of global petroleum production in “potentially unstable” countries poses a significant energy-security risk to the U.S. economy. They worry that turmoil or conflict in those nations could cut global petroleum supply by as much as 10%, “leading to an unprecedented price shock.” They are also concerned that OPEC could use “monopoly power” to “restrict oil supply relative to demand.”

While such risks are possible, their likelihood is small and diminishing. Despite ongoing warfare in Middle East, UN sanctions that cut Iran’s oil exports nearly in half, Russia’s invasion of Crimea, and continuing warfare in Ukraine, the price of crude oil is lower than at any time since February 2009. U.S. motorists enjoyed the lowest Labor Day gasoline prices in a decade. The decline in oil and gasoline prices, despite geopolitical tensions, is a testament to the ingenuity of U.S. producers, who have used directional drilling and hydraulic fracturing to increase domestic production every year since 2008.

Rather than restrict output to raise prices, OPEC is following a “no production cuts” policy, with Saudi Arabia increasing output to a record 10.4 million barrels per day (MMBD) in the second quarter of 2015. Perhaps OPEC members simply don’t want to lose even more market share to North American producers. Or perhaps they want to drive oil prices below the U.S. fracking industry’s production costs. Whatever the case, the proposed rule would do nothing to diminish Russia and OPEC’s share of world oil production.

Other policies would more effectively shift global production from Russia and OPEC to the United States and Canada. Those include repeal of the crude oil export ban, timely approval of major infrastructure projects such as the Keystone XL Pipeline, and allowing more oil and gas exploration in U.S. coastal waters and federal lands, such as the Alaska National Wildlife Refuge (ANWR). The White House recently declined to comment on an Energy Information Administration (EIA) study finding net economic benefits from oil exports, and the administration’s policies on Keystone and ANWR are counterproductive.

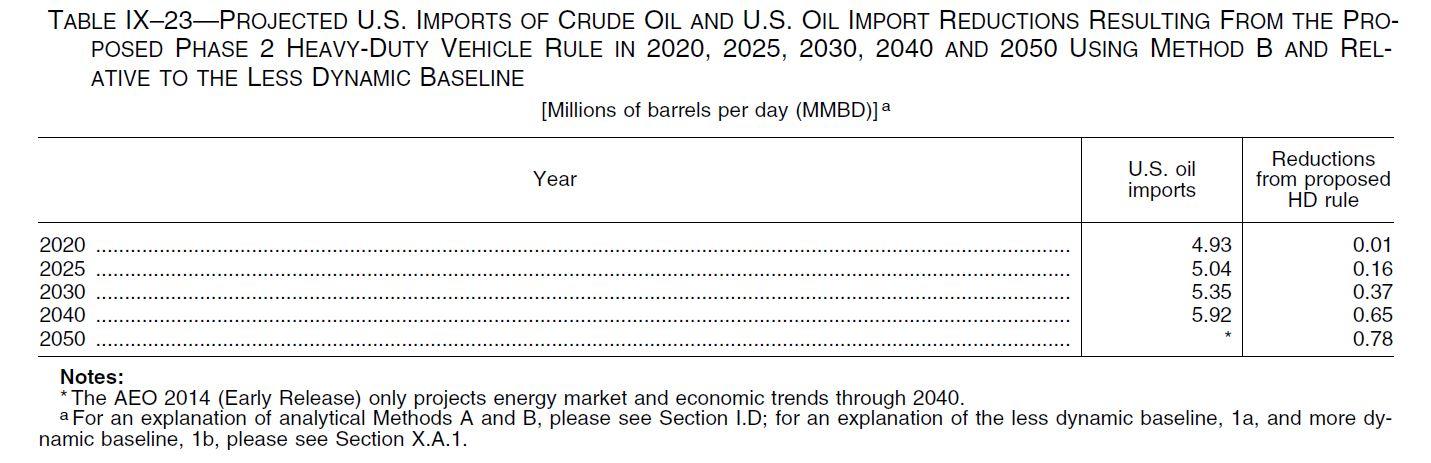

NHTSA estimates its fuel economy standards will reduce U.S. oil imports by 0.16 MMBD in 2025, 0.37 MMBD in 2030, and 0.65 MMBD in 2040. So by 2040, the rule would avoid 10% of projected imports.

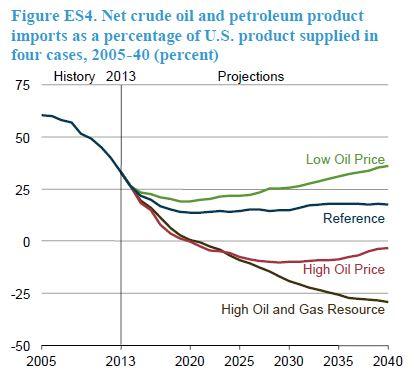

Imports as a share of total production declined from 60% in 2005, to 40% in 2012, to 27% in 2014. EIA expects the decline in import dependence to continue. The agency’s 2015 Annual Energy Outlook (AEO 2015) forecasts net U.S. oil and petroleum product imports in four cases. In the reference case, the net import share falls from 33% in 2013 to 17% in 2040.

If imports as a share of consumption fall to 17% in 2040, and the proposed rule cuts imports by 10%, it will reduce national consumption by 1.7%. Such a minor change would do little to ameliorate price shocks from major disruptions in global petroleum supply.

III. The rule implies that truckers, like children, are incapable of discerning and/or pursuing their own best interest.

If the proposed rule will have no detectable effect on climate change or energy security, what is the point? The new standards will save truckers a bundle of money, EPA and NHTSA contend. According to their calculations, the rule will increase the cost of new trucks and trailers by $20 billion to $30 billion over the lifetimes of the vehicles, but it will also cut fuel consumption by more than 70 billion gallons, saving truckers approximately $90 billion to $170 billion in reduced fuel expenditures. In other words, truckers will reap net benefits of approximately $70 billion to $140 billion.

This should immediately raise a red flag. Trucking companies are in business to make money. As the agencies acknowledge, “Unlike light-duty vehicles – which are purchased and used mainly by individuals and households – the vast majority of HDVs are purchased and operated by profit-seeking businesses for which fuel costs represent a substantial operating expense.” Indeed, for many truckers, fuel is the single biggest operating expense, exceeding drivers’ wages and benefits combined.

Clearly, nobody has a keener incentive to purchase cost-effective fuel-saving technology than people who haul freight for a living. Demand for fuel-efficient trucks should, in turn, spur manufacturers to develop, produce, and market such vehicles.

If every dollar invested to improve fuel economy yields savings of $4-$6, why hasn’t the market already made those investments? If the agencies’ recommended package of fuel-saving technologies is such a great bargain, why do truckers need a regulation compelling them to buy it?

The proposed rule implies that truckers, like children, are incapable of discerning and/or pursuing their own best interest. Or it implies that manufacturers are too dim or lazy to expand market share by developing vehicles that give their customers a competitive edge.

EPA and NHTSA don’t put things that way, of course. As in the Phase 1 rulemaking, the agencies offer “hypotheses” drawn from economics literature to explain the “paradox” of under-investment in fuel economy. None of the explanations provides solid evidence of market failure. In fact, some indicate truckers are just behaving like prudent buyers. Let’s look at each in turn.

IV. The agencies’ “hypotheses” neither demonstrate market failure nor persuasively explain the “paradox” of “under-investment.”

The agencies summarize five hypotheses.

(1) Imperfect Information in the New Vehicle Market. One possible reason for the supposed under-investment is that information “about the effectiveness of some fuel-saving technologies” is “inadequate or unreliable.” But if the relevant information is inadequate or unreliable, how do EPA and NHTSA know the rule will deliver billions in net benefits to truckers?

The hypothesis implies that the agencies possess technical information unavailable to industry. That is implausible, because EPA has made considerable efforts since the early 2000s to share fuel-economy information with the trucking industry, its leading firms, and trade associations. Surely the agencies’ general position that fuel-saving technology more than pays for itself is now well known throughout the industry, which has been subject to fuel-economy regulation since 2011.

Through its voluntary SmartWay Transportation Partnership Program, EPA “has worked closely with truck and trailer manufacturers and truck fleets over the last ten years to develop test procedures to evaluate vehicle and component performance in reducing fuel consumption and has conducted testing and has established test programs to verify technologies that can achieve these reductions.” The program is a partnership between EPA and the freight goods industry, including the American Trucking Association and 2,380 truck carrier firms. All of the top 25 U.S. long-haul trucking companies are SmartWay Partners.

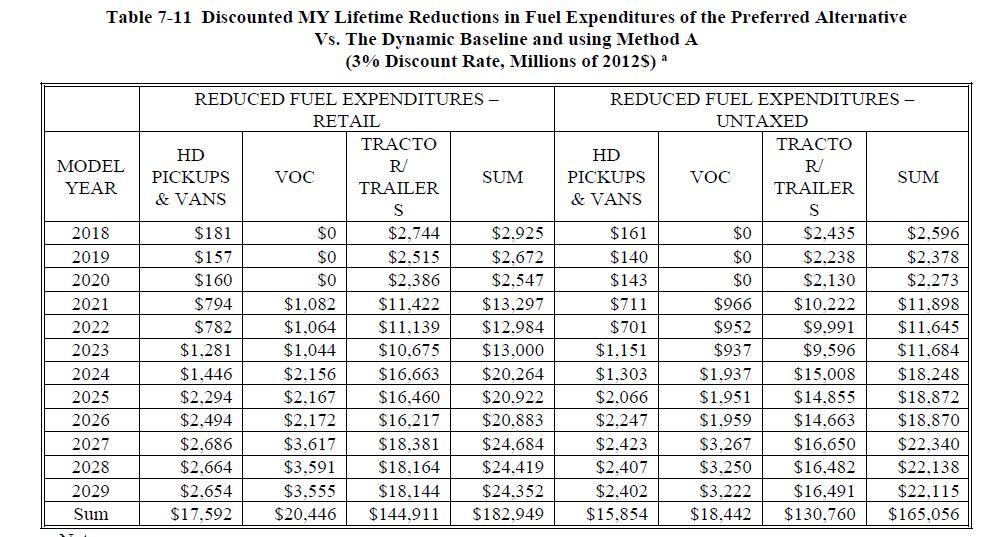

With all the ‘verified’ fuel-saving information EPA has been providing, semi-truck owners should exhibit the smallest gap between actual investment in fuel economy and what the agencies consider optimal. Yet that’s where the alleged “energy efficiency gap” is largest. EPA and NHTSA estimate the rule will save semi-truck owners $144.9 billion in fuel expenditures – seven times more than the rule will save vocational truck owners ($20.4 billion) and eight times more than it will save HD van and pickup owners ($17.5 billion).

Note: The agencies also assume long-haul truckers will reap the biggest return on investment. Semi-truck owners will have to spend more ($12.7 billion) than vocational truck owners ($7.8 billion) and HD pickup and van owners ($4.9 billion) to comply with the rule. However, the projected benefit-cost ratio for semi-truck owners (11.4:1) substantially exceeds those for vocational trucks (2.6:1) and HD vans and pickups (3.5:1). So the gap is largest for that segment of the HDV market that has the most agency-provided information. In short, the hypothesis does not explain why truckers (supposedly) under-invest in fuel-saving technology.

(2) Imperfect Information in the Resale Market. The agencies hypothesize that buyers in the new vehicle market may not be willing to pay more for fuel-efficient vehicles if buyers in the used market are unwilling “to pay adequate premiums” for improved fuel economy. But why would buyers in the used market shun vehicles that (allegedly) repay the price premium many times over?

To our knowledge, nobody claims the resale market fails to consider the value of technologies that enhance vehicle reliability, performance, comfort, and amenities. After all, people generally are willing to pay more for a better vehicle, whether it’s new or used.

Why should fuel economy be the exception to the rule? Maybe fuel-saving technology doesn’t add much to the price of used trucks because its money-saving potential is unproven or over-rated.

(3) Principal-agent problems causing split Incentives. According to this hypothesis, those who own trucks are often different from those who operate the vehicles. The agencies’ discussion here is terse. According to the Phase 1 rulemaking, operators may have “strong incentives to economize” on fuel consumption whereas owners may place a higher priority on capital investment that “improves vehicles’ durability or reduces their maintenance costs.” Even if such split incentives exist, it would still not necessarily follow that owners under-invest in fuel economy.

There are tradeoffs — opportunity costs — in every investment decision. Whether it is smart to invest more or less in fuel economy relative to vehicle durability or any other value depends on each firm’s unique circumstances. As the Phase 2 rulemaking acknowledges, “In general, businesses that operate HDVs face a range of competing uses for available capital other than investing in fuel-saving technologies, and may assign higher priority to these other uses, even when investing in higher fuel efficiency HDVs appears to promise adequate financial returns.” Spot on. The agencies, however, do not seem to grasp what that observation implies. EPA and NHTSA are in no position to divine an appropriate tradeoff for the industry as a whole, because the right tradeoff varies from firm to firm, and within each firm at different times.

Besides, just because truck operators make the actual fuel purchases does not necessarily mean owners ignore fuel costs. An owner may delegate many purchasing decisions for many things to other people. He is nonetheless responsible for the firm’s bottom line. The tradeoffs the firm makes between fuel economy and other investments inevitably show up in the firm’s balance sheets.

Strangely, the Phase 2 rulemaking postulates a split incentive that works the other way – supposedly, owners care about fuel costs but drivers don’t unless offered “financial incentives.” That the literature on split incentives is itself split on whether principal or agent undervalues fuel economy is reason enough to be skeptical of this alleged market failure.

(4) Uncertainty about Future Cost Savings. Another possible reason companies don’t adopt fuel-saving technology as fast as EPA and NHTSA deem appropriate is that “HDV buyers may be uncertain about future fuel prices, or about maintenance costs and reliability of some fuel efficiency technologies.” Thus buyers may discount potential future savings at higher rates than those used in the agencies’ analysis. “In contrast, the costs of fuel-saving or maintenance-reducing technologies are immediate and thus not subject to discounting.” Exactly! Whereas the costs of investment in fuel-saving technology are certain and immediate, the payoff depends on unknown quantities — the future price of fuel and, perhaps more importantly, the “lifetime, expected use, and reliability of the vehicle.”

According to the previously cited report prepared for American Truck Dealers, owners of trucks and engines designed to meet EPA’s model year (MY) 2004 and 2007 emission standards experienced “significant reliability, operating cost, and fuel economy concerns.”

For example, it has been reported that for the eighth largest carrier in the U.S., “maintenance costs for Schneider’s 2007 model trucks were about 28.2% higher than vehicles manufactured before October 2002.” Reliability is critical for commercial fleets and owner-operators both because of the costs of keeping trucks in operation and the even greater potential costs associated with out-of-service equipment. In addition to higher truck prices and operating costs, anticipated reliability issues are often cited as contributing to the marketplace disruptions discussed herein.

Companies are just being prudent when they invest less in fuel-saving technology than they would if Congress required EPA and NHTSA to compensate truckers for every dollar of projected fuel savings that fails to occur. As the agencies acknowledge in the Phase 1 rulemaking, mandatory investment in fuel-saving technology “requires purchasers to assume a greater level of risk than they would in its absence, even if the future fuel savings predicted by a risk-neutral calculation actually materialize.”

(5) Adjustment and Transactions Costs. According to this hypothesis, drivers may be slow or reluctant to make the operational adjustments required for effective use of new fuel-saving technologies, and owners may be reluctant to incur costs associated with driver training or faster fleet turnover. This hypothesis is tantamount to saying there are costs of innovation. That is true in general, yet competition continually drives firms in most industries to innovate or get left behind. What makes fuel-saving technology the exception to the rule?

The Phase 1 rulemaking offers this explanation: “Because of the diversity in the trucking industry, truck owners and fleets may like to see how a new technology works in the field, when applied to their specific operations, before they adopt it.” Yes! Companies want real — road-tested — information about alternative investments. As Phase 2 similarly acknowledges, “businesses that operate HDVs may be concerned about how reliable new technologies will prove to be on the road, and whether significant additional maintenance costs or equipment malfunctions that result in costly downtime could occur.”

Truckers, apparently, take the agencies’ benefit-cost estimates with several grains of salt. That does not surprise us. After all, EPA and NHTSA are stakeholders – organizations with an interest in the rules they develop and administer. Regulators have an incentive to over-estimate the benefits and low-ball the costs of their rules, for at least three reasons. (1) New regulations typically increase agencies’ power, prestige, budgets, and/or staff. (2) When mandated technology malfunctions and vehicles are taken out of service, it’s the owners, not the agencies, who must pay for repairs and risk losing customers. (3) Ideological zeal for ‘greening’ the U.S. transport system is honored in both agencies.

All of which is to say, the market is not failing when businesses choose to be guided by real-world results rather than agency forecasts. To their credit, the agencies’ Phase 1 rulemaking acknowledges that “there may be no market failure” in the risk-aversion induced by adjustment and transaction costs, which, unlike the promised payoffs from fuel-economy investments, “are typically immediate and undiscounted.”

V. Alternative hypothesis: EPA’s diesel-engine emission standards have hindered HDV fuel economy.

Trucking industry profit-margins are thin and fuel is the single biggest operating expense. Consequently, truckers, especially those who haul freight long distances in “combination tractors” (semis), should have a strong incentive to purchase vehicles incorporating cost-effective improvements in fuel economy, and manufacturers, in turn, should have a strong incentive to compete for their business. Yet the agencies claim to find a gap between current fuel efficiency and what is technically achievable at reasonable cost. How can that be?

To some extent truckers may just be behaving like prudent buyers, as discussed above. Many reportedly feel they have been burned by previous technology mandates. Before incurring the certain and immediate costs of purchasing agency-approved fuel-efficiency technology, they want to see results – how much fuel is actually saved and what are the longer-term effects on truck reliability and maintenance costs.

Considerable evidence suggests another, complementary explanation: EPA’s emission-control standards for diesel trucks caused or contributed to the very problem – stagnant fuel economy – the agencies now propose to solve with more rules. The Competitive Enterprise Institute (CEI) presented a case for a ‘government failure’ hypothesis in its comment on the Phase 1 rulemaking. Because EPA’s Response to Comments either inadequately addressed or simply ignored some of CEI’s arguments, we will restate and update the alternative hypothesis here.

Opportunity Costs: Manufacturers

Every dollar engine manufacturers spend on R&D to make vehicles compliant with EPA diesel emission standards is a dollar they cannot spend on R&D to increase HDV fuel efficiency. Such expenditures are substantial.

EPA’s Regulatory Impact Analysis (RIA), published in 2000, for its year 2007 diesel emission standards rule estimated that:

-

Engine manufacturers would spend $385 million over five years on HDV diesel-engine design R&D and $220 million in catalyst systems R&D, yielding a “total R&D outlay for improved emission control of more than $600 million.”

-

Each of 11 major engine manufacturers would spend $7 million annually to deploy a “team of more than 21 engineers and 28 technicians to carry out advanced engine research.”

In other words, over a five-year period, up to $600 million that might have been invested in fuel-economy R&D was instead invested in emission-control R&D. In addition, up to 540 engineers and technicians who might otherwise have spent all or much of their time developing fuel-saving technology instead likely spent all or much of their time developing emission-control technology.

EPA’s enforcement actions also diverted substantial resources that might otherwise have been available to enhance fuel-saving technology.

During the 1990s, seven major truck manufacturers sold 1.3 million trucks equipped with “defeat devices” that bypass or disable on-board emission control systems. “These devices altered the engines’ fuel injection timing and, while this improved fuel economy, it also increased nitrogen oxide emissions by two to three times the existing regulatory limits,” GAO explained. EPA launched what it described as the “largest Clean Air Act enforcement action” in its history. The case was settled via consent decrees under which the manufacturers agreed to pay $83 million in civil penalties, invest almost $110 million in NOX control R&D, and spend more than $850 million to produce cleaner engines by October 1, 2002.

The booming market in unlawful defeat devices was itself a reflection of the high value long-haul truckers place on cost-effective fuel-saving technology. How ironic that EPA punished manufacturers who promoted fuel savings by mandating $1 billion in expenditures for technologies that did not enhance fuel efficiency or even (as discussed below) reduced it!

Opportunity Costs: Buyers

Every dollar owners spend to buy and maintain trucks compliant with diesel emission standards is a dollar they cannot spend on improved fuel-saving technology. The RIA for the 2007-2010 emission standards estimated that the rule would increase vehicle cost by $3,230 in the first year, declining to $1,870 in later years, and increase operating costs by $4,600.

In November 2008, NERA Economic Consulting published a report on customer responses to the 2007 rule. NERA found that the rule increased the unit cost of a Class 8 truck by $7,000 between MYs 2006 and 2007 – more than twice what EPA estimated. In addition, NERA projected that EPA’s 2010 NOX standard would increase the cost of a Class 8 truck by another $7,000-$10,000.

In March 2010, Kevin Jones, a reporter for The Trucker magazine, interviewed Daimler Trucks North America President and CEO Martin Daum at the Louisville, Ky. Mid-America Trucking Show. Daum told Jones that EPA’s emission standards added $20,000 to the cost of an 18-wheeler over the previous six years. As noted above, the 2012 report for American Truck Dealers estimates that during 2004-2010, EPA emission standards cumulatively increased the cost of Class 8 trucks by more than $21,000.

Clearly, the standards took large bites out of customers’ budgets – dollars truckers could not spend on fuel-saving technology. The regulation-induced increase in the cost of new trucks since 2004 is roughly twice the estimated cost of the technology upgrades semis will have install to comply with the Phase 2 GHG/fuel economy rule.

Truckers also incurred significant reliability and maintenance costs as a result of the penalties EPA imposed on the manufacturers who installed fuel-saving defeat devices. As part of the settlement agreement, manufacturers agreed to “accelerate by 15 months the schedule for meeting new, more stringent engine standards to October 2002 instead of the original mandatory date of 2004.” According to GAO, “Trucking companies maintain they need 18 to 24 months to road test an engine’s reliability in all weather and operating conditions and to develop their future purchasing plans.” The consent decree did not allow time for adequate road-testing, and many truckers experienced costly engine problems.

For example, one company reported that roughly one-half of its 140 new heavy-duty engines experienced an engine valve failure prior to 50,000 miles. In addition, these officials noted that roughly 20 percent of their heavy-duty vehicles with the new engines are out of service at any given time due to maintenance concerns, compared to 5 percent for the remainder of their fleet. Several of these officials expressed a concern that some companies may have difficulty absorbing increased costs from such maintenance problems.

Tradeoff: Emission Standards and Fuel Economy

In its Response to Comments (RTC) on the Phase 1 rulemaking, EPA acknowledged but summarily dismissed CEI’s hypothesis that mandatory investment in pollution control “crowds out” investment in fuel economy.

Only if access to capital is significantly constrained would the industry consider these as alternative investments. The same principles apply for access to expertise: truck companies could hire additional engineers and technicians to work on either fuel efficiency or emissions reduction. In the absence of evidence of “crowding out” of investments in fuel economy, we are left with the puzzle of what appears to be a great deal of lack of adoption of cost-effective fuel-saving technology.

That response is unpersuasive. Regulatory mandates can have disruptive impacts on the market for new vehicles, leading to surges in buying pre-compliant vehicles (“pre-buying”) followed by revenue losses and layoffs (“sales cliffs”). As the agencies acknowledge:

Several of the heavy-duty vehicle manufacturers, fleets, and commercial truck dealerships informed the agencies that for fleet purchases that are planned more than a year in advance, expectations of reduced reliability, increased operating costs, reduced residual value, or of large increases in purchase prices [as a result of technology mandates] can lead the fleets to pull-ahead by several months planned future vehicle purchases by pre-buying vehicles without the newer technology. In the context of the Class 8 tractor market, where a relatively small number of large fleets typically purchase very large volumes of tractors, such actions by a small number of firms can result in large swings in sales volumes. Such market impacts would be followed by some period of reduced purchases that can lead to temporary layoffs at the factories producing the engines and vehicles, as well as at supplier factories, and disruptions at dealerships.

The report prepared for American Truck Dealers contains a chart showing the regulation-induced surge in pre-buy orders before consent decree standards took effect in 2002, following by a slump, and another surge in pre-buy orders in 2006 before the MY 2007 standards took effect, again followed by a slump.

Manufacturers experienced non-trivial employment impacts as a consequence of the pre-buy/sales cliff swings:

For example, when faced with declining sales following the pre-buy, Volvo laid off 300 workers in March of 2001 and another 300 workers in April of that year. In 2006, Volvo’s Deputy Chief Executive Officer warned that the new environmental regulations would cause such a precipitous decline in sales that Volvo would have no choice but to lay off more people. Volvo ended up laying off nearly 600 workers in 2006; the direct result of the new emissions mandates. Also in 2006, Peterbilt cut their workforce by almost half. Freightliner laid off nearly 1,800 workers in 2007, followed by another layoff of 2,100 workers, and the complete shut down a manufacturing plant in 2009.

Clearly, EPA emission standards have the power to “significantly constrain” manufacturers’ sales and work forces in particular years. Why should access to capital and expertise be immune to such effects? As a general matter, moreover, we find it hard to believe manufacturers would incur no opportunity costs from continual increases in regulatory stringency and a $1 billion enforcement action.

The RTC simply ignores the other side of the equation – the opportunity cost imposed on truck buyers by emission standards that increase the cost of new vehicles.

More importantly, the RTC also ignores the point, widely acknowledged in the literature, that it is difficult and/or costly to boost (or maintain) diesel fuel economy while reducing diesel emissions. Consider this excerpt from a paper by diesel emission-control expert W. Addy Majewski:

We should also mention that there is a certain cost for meeting these ambitious emission standards with future diesel engines. This cost consists of two components: (1) the cost of the emission control equipment and (2) a fuel economy penalty. The first component can vary greatly depending on the technology (some of which relies on expensive precious metal catalysts). The fuel economy penalty may be derived from a number of sources. First, traditionally there has been a correlation between engine-out NOX emissions and fuel consumption in the diesel engine, where higher engine efficiency and better fuel economy are associated with higher NOX. Second, exhaust after-treatment devices are associated with a varying additional fuel economy penalty caused by such factors as increased pressure drop and energy consumption for the regeneration of filters and/or NOX adsorbers. In the case of SCR catalysts, while there may be no direct fuel economy penalty, operating costs are increased by the cost of urea.

Despite decades of technological advances, the Volkswagon scandal indicates that emission standards continue to impose a fuel-economy tradeoff on diesel-powered passenger vehicles. Why did VW take the insane risk of installing unlawful defeat devices in 11 million vehicles? Apparently, VW believed cheating on emissions tests was the only way to give consumers all the fuel-economy and performance they wanted at prices they could afford. As a recent article in Wired explains:

Once the sting of the lie fades, the US customers who bought 482,000 of those cars will feel the real pain. Because Volkswagen will be forced to recall those vehicles and somehow make them meet federal standards. There are two apparent ways to do that, and owners who value performance, fuel economy, and trunk space won’t like either.

One is to “reflash” the engine control module, recalibrating the software so the car always runs the way it does during EPA testing, and always meets emission standards.

The downside here is that to achieve the drastic drop in NOX emissions, the cars in test mode sacrificed some fuel economy, or performance. Just how much is hard to say, but any drop in torque – one great thing about diesels is how they accelerate off the line – will not make drivers happy. And a drop in mileage would likely cost VW, since hundreds of thousands of drivers would have to spend more on fuel than VW promised at the time of sale. . . .

The standard way of making a diesel run cleanly is to use selective catalytic reduction, a chemical process that breaks NOX down into nitrogen and water. Part of that process includes adding urea to the mix. The super effective system can eliminate 70 to 90 percent of NOX emissions, and is used by other diesel manufacturers like Mercedes and BMW. The downside is that it adds complication to the system, and cost – $5,000 to $8,000 per car. And you need to periodically add the urea-based solution to your car to keep it working.

GAO’s report on EPA’s 1998 enforcement action against truck manufacturers who sold 1.3 million illegal defeat devices has already been noted. That this unlawful practice was the industry norm for years also attests to a non-trivial tradeoff between lower emissions and higher mileage.

As mentioned, because the settlement agreement accelerated from January 2004 to October 2002 the schedule for producing less polluting vehicles, which did not allow truck owners adequate time to road-test those vehicles, owners engaged pre-buying. In the months preceding the October 2002 deadline, demand for new vehicles with older technology surged. According to GAO, roughly 19,000 to 24,000 (20%-26%) of the 93,000 large semis (Class 8 trucks) produced during April to September 2002 were pre-buys. Conversely, sales of compliant vehicles after the deadline were much lower than EPA had projected. Data for the first 13 of the 15 months “show that about 148,000 fully or partially compliant heavy-duty diesel engines are on the road, compared to EPA’s estimate of 233,000 such compliant engines for the entire 15-month time frame.”

GAO found three main reasons for the pre-buy surge: (1) Trucks equipped with older emission-control technology costs several thousand dollars less than trucks with the new emission-control technologies; (2) the settlement agreement did not give the market time to sort out the effects of the new technologies on truck durability and maintenance; and (3) the technologies were expected to reduce fuel economy. GAO stated:

The four companies that pre-bought large numbers of trucks before the October 2002 deadline did so primarily because they were concerned about the higher price and unproven reliability of the new engines, according to company officials. They said that the new engines would have added from $1,500 to $6,000 to the purchase price of a new heavy-duty truck—whose base cost is about $96,000—and would have reduced fuel economy by 2 to 10 percent. For 2002, these additional costs could have ranged from about $4 million to $27 million per company in purchase price and about $3 million to $90 million per company in fuel costs. These trucking officials said that these additional costs would have been problematic for some companies because, according to one representative, the industry only returns 3 or 4 cents per dollar invested

Industry expected further adverse impacts on fuel economy from EPA’s 2007 diesel emission standards rule:

Because the technologies needed to meet the 2007 standards are much more advanced than those associated with prior upgrades, the trucking companies are concerned that the new engines will cost much more and decrease fuel efficiency much more than EPA predicted in 2000 when it was developing the standards. Consequently, according to representatives of 9 of the 10 trucking companies we contacted, companies most likely will once again decide to buy trucks before the deadline, but in larger numbers than they did in response to the consent decrees. This could again disrupt markets and postpone needed emissions reductions.

Specifically, trucking industry representatives opined that the 2007 standards would reduce fuel efficiency by 3-5%. That’s a big deal for an industry where fuel is the single biggest operating expense and profit margins can be as low as 2 cents per dollar earned:

In addition, these officials are concerned that the 2007 trucks will experience another 3 to 5 percent loss in fuel economy – added to the 3 to 5 percent loss resulting from the consent decrees – that could increase their companies’ fuel costs by millions of dollars per year. Even minor increases in business costs can have adverse effects in the trucking industry, according to trucking industry officials we contacted, because these companies’ profit margins are very narrow – sometimes only 2 cents per dollar earned. The officials claim that the highly competitive nature of the trucking business precludes companies from passing such significant cost increases to their customers.

In short, the industry representatives interviewed by GAO estimated the 2007 Rule combined with the consent decree could lower heavy-truck fuel economy by as much as 10%.

In April 2007, Robert Guy Matthews reported in the Wall Street Journal that new trucks compliant with EPA diesel emission standards “got worse mileage” than older trucks. The fuel-economy penalty was big enough to affect company bottom lines:

Previous-generation trucks average about nine or 10 miles to each gallon of diesel fuel. New engines designed to meet the more-stringent federal mandate on truck exhaust get about one mile less to the gallon. That may not seem like much, but it all adds up for large fleet owners that operate trucks crisscrossing the country.

“For every additional mile-per-gallon lost, it costs us about $10 million in [total annual] fuel costs,” said YRC Worldwide Chief Executive Bill Zollars. YRC is one of the largest transportation providers in the country, operating a fleet of 20,000 trucks. . . .

Freightliner LLC, the largest heavy-duty truck maker in North America, confirmed that some loss of fuel economy was inevitable for engines to comply with the new standards. Certain parts of the engine must run at a higher temperature to burn off pollutants, and that requires more fuel.

To meet EPA’s MY 2004 NOX emission standards, new trucks required exhaust gas recirculation (EGR) technology. EPA predicted that fuel injection, variable geometry, and turbocharging would offset any EGR-associated fuel-economy penalty, and projected no drop in fuel economy from the MY 2007-2010 requirements. According to the report prepared for American Truck Dealers:

EGR systems may be effective at reducing NOX emissions, but they undeniably reduce the fuel economy performance that would otherwise have been achieved. For example, Judy McTigue, director of marketing and planning research for Kenworth Trucks, stated that “2007-compliant engines equipped with exhaust gas recirculation systems suffered a fuel economy penalty of 5% to 9%.” EGR systems also contributed to a loss of 50 to 100 horsepower from heavy-duty engines.

If we also factor in the opportunity costs of EPA’s emission standards program — foregone investment in fuel-saving technology R&D, foregone purchases of more fuel-efficient trucks – it is possible that EPA’s regulatory and enforcement actions account for all of perceived problem of lagging fuel economy in the heavy truck sector. Were it not for truckers’ use of regulatory avoidance strategies – buying trucks equipped with defeat devices in the 1990s, pre-buying older engines, and low-buying compliant engines in the 2000s — heavy-truck fuel economy might be even lower.

VI. Conclusion

The proposed rule is silent about the potential impacts of new GHG and fuel economy standards on small trucking firms. History suggests the standards will increase equipment costs, operating expenses, and engine malfunctions by more than the agencies anticipate. The rule evinces no awareness that small firms already struggle to cope with existing regulations, and that additional regulatory burdens may drive many small owner-operators out of business.

EPA and NHTSA acknowledge the reality of a “NOX-CO2 tradeoff,” but only as a rationale for using the “same test procedures” for both NOX and CO2 to discourage engine manufacturers from gaming emission tests. They discuss several “hypotheses” to explain industry’s alleged “under-investment” in fuel-saving technology without ever wondering whether the regulatory environment in which truckers operate might have something to do with it.

Substantial evidence indicates that, during the 2000s, EPA’s diesel-truck emission standards held back HDV fuel efficiency and imposed significant opportunity costs on both manufacturers and truckers. Insofar as there is an “energy-efficiency gap,” it appears to be an example of regulation-induced government failure rather than of market failure.

It may be unrealistic to expect an agency to take responsibility for the very problem it seeks more power over industry to solve. Nonetheless, given the administration’s high-profile commitment to “transparency,” EPA and NHTSA should have at least addressed the issue. They have not done so.