Central Bank Digital Currencies Threaten Global Stability and Financial Privacy

Executive Summary

As digital currencies go mainstream around the world, governments and international financial bodies are seeking to develop ways to regulate them. Some countries have opted to issue their own central bank digital currencies (CBDCs). Central bankers and their political allies claim that CBDCs can help address a range of supposed global finance ills, from terrorist financing to money laundering. However, CBDCs could give governments a powerful tool for economic and social control and unprecedented intrusion into the private financial lives of billions of people. Some authoritarian regimes and developing countries have already embraced digitized currencies while banning or discouraging nongovernmental cryptocurrencies.

Western governments are rushing to follow suit with promises of financial inclusion, greater protection against illegal activity, more efficient monetary policy, and smoother cross-border transactions. Yet, when inevitable design tradeoffs are examined, these benefits shrink or vanish. Conversely, CBDCs’ negative implications for global and domestic financial stability and financial privacy become magnified under scrutiny. Less overtly, these governments and central bankers see CBDCs as countering challenges to their authority by authoritarian regimes and big technology companies.

Already, stablecoins have produced many of the benefits CBDC proponents promise without the inevitable frictions and unforeseen issues that multi-jurisdictional CBDCs would create.

In the end, CBDCs are a solution in search of a problem. Many CBDC promoters have sat at the pinnacle of financial power for decades. The post-World War II global order endowed domestic and international financial regulators with immense power, with mixed results. But private competition is exposing flaws that become exacerbated in times of high inflation and pandemics. Citizens have seen mismanaged currencies and incompetence or abuse by civil servants, and doubt that any benefits would outweigh the potential costs. Private cryptocurrencies, especially stablecoins, are solving problems, innovating, and creating opportunities in a way that central bankers cannot.

Western nations should scrap CBDC plans and promote stablecoins as the answer to perceived threats to global financial stability posed by authoritarian regimes and big technology companies.

Introduction

As digital currencies go mainstream around the world, governments and international financial bodies are seeking to develop ways to regulate them. Some countries have opted to issue their own central bank digital currencies (CBDCs). Central bankers and their political allies claim that CBDCs can help address a range of supposed global finance ills, from terrorist financing to money laundering. However, CBDCs could give governments a powerful tool for economic and social control and unprecedented intrusion into the private financial lives of billions of people. Some authoritarian regimes and developing countries have already embraced digitized currencies while banning or discouraging nongovernmental cryptocurrencies. For instance, China has declared all cryptocurrencies illegal1 and banned Bitcoin mining.2 India seems poised to take the less drastic step of banning cryptocurrencies for payments but allow trading.3

Policy makers in freer and wealthier nations have been more open to the promise of cryptocurrencies and wary of government alternatives, until now— but that is changing. A newfound urgency has emerged for adopting CBDCs among developed country policy makers that seems unconnected to any financial and payment system flaws. Financial regulators usually only implement currency changes of this magnitude following strenuous cost-benefit analysis. For instance, U.S. policy makers have spent two decades debating whether to abandon the penny. By contrast, CBDC promoters invoke lofty platitudes and theoretical harms, rather than data-driven analysis, in a rush to transform the financial system.

This is a major change. Previously, Western governments and the international standard-setting Bank for International Settlements (BIS) had adopted a cautious approach toward CBDCs because of the high costs and risks involved. For example, a 2018 BIS report cited a) limited benefits for payments compared with private alternatives, b) risks to the current commercial banking system, and c) a greater role for central banks in allocating economic resources.4

Now central banks and financial regulators around the world—warning of the power of authoritarian regimes and big technology companies, but perhaps most fearing ordinary citizens exercising newfound monetary freedoms—seek to preserve status at the cost of innovation, while jeopardizing financial stability. It is a price not worth paying.

Western leaders should adhere to a “do no harm” approach and look for ways to encourage innovation and choice. In the end, private and open competition is the best way to check the ambitions of authoritarian regimes and massive technology companies, while ensuring stability and prosperity.

This paper examines official rationales behind the advocacy for central bank digital currencies, underlying motivations, and implementation risks, as Western governments move forward.

The Bank for International Settlements and Western Governments Change Course on CBDCs

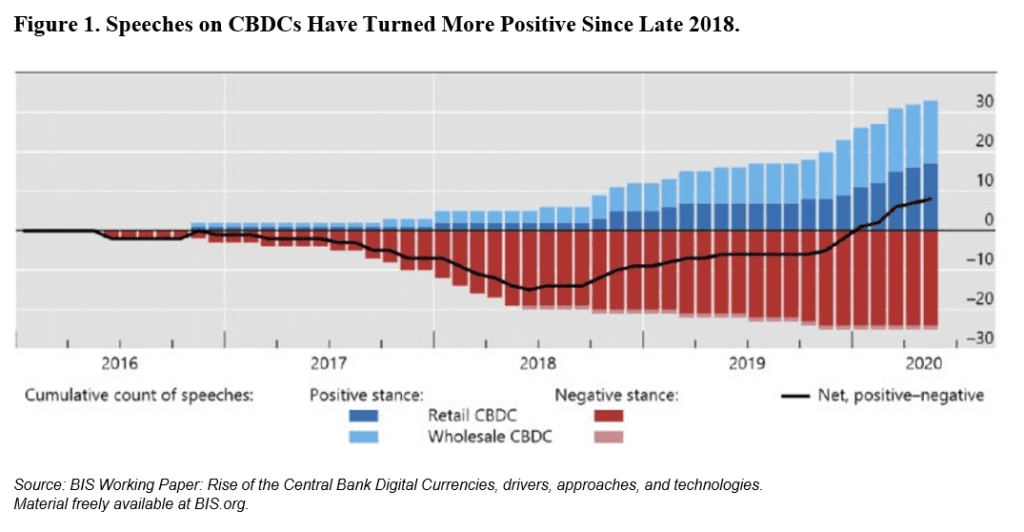

Internationally, the Bank for International Settlements reported in January 2021 that 86 percent of countries are currently researching CBDCs and that 60 percent are at proof-of-concept stage—up 6 percent and 18 percent, respectively, from 2019.5 Domestically, Federal Reserve Chair Jerome Powell and Federal Reserve Governor Lael Brainard have promoted a CBDC or “digital dollar.” At a February hearing before the Senate Banking Committee, Powell said that a digital dollar was a “high priority project for us.”6 In a May 2021 speech, delivered at a conference hosted by the cryptocurrency news site CoinDesk, Brainard outlined familiar CBDC rationales. She noted: “Four developments—the growing role of digital private money, the migration to digital payments, plans for the use of foreign CBDCs in cross-border payments, and concerns about financial exclusion—are sharpening the focus on CBDCs.”7

Although the above comments include qualifiers regarding challenges and technical hurdles, the rhetorical change—from caution toward enthusiasm for CBDCs—is stark. In December 2019 testimony, then-Treasury Secretary Steve Mnuchin told the House Financial Services Committee: “As it relates to the Fed, and Chair Powell and I have discussed this at length. I think we both agree that in the near future, in the next five years, we see no need for the Fed to issue a digital currency.”8 That echoed Brainard’s remarks at a 2018 San Francisco Fed conference: “There is no compelling demonstrated need for a Fed-issued digital currency.”9 That same year, a BIS report stated: “While specifics will vary according to a country’s circumstances and economic conditions … payment-related motivations for issuing CBDC appear at this time not to be compelling for most jurisdictions.”10

Chinese and Big Tech Pressure Spurred CBDC Change of Heart The rhetoric began changing in late 2018, thanks to two main factors, as Brainard later explained at the 2021 CoinDesk conference:

With technology platforms introducing digital private money into the U.S. payments system, and foreign authorities exploring the potential for central bank digital currencies (CBDCs) in cross-border payments, the Federal Reserve is stepping up its research and public engagement on CBDCs.11

China began researching digital currencies in 2014. Its first-mover status, combined with its dismal human rights record, economic power, and global ambitions, should cause concern.12 Following China’s lead, other governments began exploring issuing their own CBDCs. But it was Facebook’s announcement of plans to launch a stablecoin—a cryptocurrency usually backed by reserve assets, such as cash, commodities, commercial paper, or government securities— named Libra, since rebranded Diem, that spurred Western forays into digital currencies. A March 2021 BIS report, citing Libra directly, said that CBDC arrangements were “preferable” to private alternatives.13

Current Rationales Do Not Justify the Push for CBDCs

Despite the rhetorical change, reasons for caution remain. Western democracies should counter Chinese ambitions by allowing an open crypto marketplace where new entrants can compete with big technology companies on trust, a key competitive advantage. Neither Chinese ambition nor large technology companies’ adoption advantages justify Western governments issuing CBDCs.

The costs imposed by governmental adoption of CBDCs would be huge. Design choices and inherent tradeoffs will limit CBDCs’ effectiveness while inviting instability, eroding privacy, and transferring power from private parties to government bodies. Policy makers need to acknowledge and examine these tradeoffs, which are usually downplayed by CBDC supporters.14

CBDC supposed benefits fall into four broad categories:

- Increasing financial inclusion;

- Curbing illegal activity;

- Increasing monetary stability; and

- Enabling more efficient payment systems, particularly for cross-border payments.

However, when design tradeoffs and risks are considered, the supposed benefits diminish or vanish. As Bank Policy Institute (BPI) President and Georgetown Adjunct Law Professor Gregory Baer states in an April 2021 paper:

[M]any discussions of CBDCs list a variety of putative benefits, without acknowledging that many of them are mutually exclusive (because they are predicated on different program designs) or effectively non-existent (because the program design that produces them comes with costs that are for other reasons unbearable.15

Financial Inclusion

Supporters claim that CBDCs will help increase financial inclusion or help to “bank the unbanked.” As Treasury Secretary Janet Yellen stated during a February 2021 virtual conference:

Too many Americans don’t have access to easy payments systems and banking accounts, and I think this is something that a digital dollar, a central bank digital currency, could help. … [I]t could result in faster, safer, and cheaper payments, which I think are important goals.16

Meanwhile, Brainard argues that the COVID-19 crisis showed financial system gaps that CBDCs could help fill, as people waited for government- provided financial relief.17

Despite those concerns, the percentage of unbanked Americans has been dropping, and CBDCs will not ease many people’s reasons for avoiding the banking system. A recent Federal Deposit Insurance Corporation (FDIC) survey found that only 5.4 percent of Americans lack bank accounts, the smallest ever share of the population.18 The stated reasons in the FDIC survey included the following:

- 20 percent lack enough money to meet minimum balance requirements;

- 16 percent do not trust banks;

- 8 percent cite problems regarding personal identification documents, credit, or former bank account;

- 7 percent believe that avoiding a bank allows them greater privacy;

- 7 percent believe that bank account fees are too high;

- 2 percent believe that bank account fee changes are too unpredictable;

- 2 percent believe that banks do not offer some needed products or services;

- 2 percent believe that bank locations are not conveniently located; and

- 2 percent believe that banks’ business hours are inconvenient.19

CBDCs would not significantly lessen these financial woes. They may enable faster payments should another COVID-like crisis occur, but those will likely be funneled through fee-charging accounts at banks or other providers. Moreover, trust and privacy concerns regarding federal involvement will not dissipate compared to those regarding commercial banks (although trust in central banks is higher than in other potential issuers). According to Pew Research, only 2 percent of Americans trust the federal government to do what is right “just about always,” while only 22 percent trust it to do what is right “most of the time.”20 In 2018 the Bank of International Settlements acknowledged:

A CBDC … does not necessarily alleviate all the constraints to access; for some segments of the population, barriers to the use of any digital currency may be large, and the preference for trusted alternatives, such as cash, is strong.21

Financial inclusion is a worthy regulatory goal, particularly in countries where sparse population or wealth means erratic bank access. But the U.S. has the world’s most mature financial system. And the federal government itself, through the Dodd-Frank financial law, has forced a significant number of people into unbanked status.22 Dodd-Frank’s Durbin Amendment—which puts below-cost price controls on what banks and credit unions may charge retailers for processing credit card transactions—forced cost-shifting away from retailers to consumers, which sharply reduced the number of free checking accounts for low-in-come consumers. A 2014 study by the George Mason University Law and Economics Center found that the amendment helped push around 1million people out of the banking system.23

Illegal Activity

CBDC proponents also argue that they will help curb illegal activity because of transaction traceability. As a May 2021 Treasury Department policy paper stated: “Cryptocurrency already poses a significant detection problem by facilitating illegal activity broadly including tax evasion.”24 At a May 2021 House Financial Services Committee hearing, Rep. Brad Sherman (D-CA) declared: “Cryptocurrencies, if they succeed, will have appeal to only two groups, narco-terrorists and tax evaders.”25 The United Nations estimates total global money laundering at up to

$2 trillion annually.26

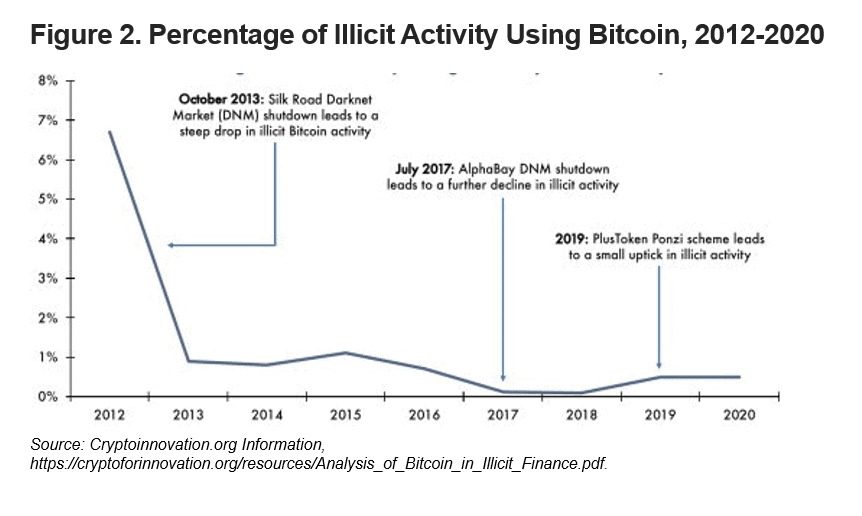

Yet, despite perceptions spread via scary stories about ransomware, hacks, and clandestine online markets, cryptocurrencies enable little illicit activity. And that number has drastically shrunk. Illicit transactions accounted for less than 1 percent of crypto activity from 2017 to 2020, according to the blockchain analytics firm Chainalysis.27 An April 2021 report from Beacon Global Strategies arrived at the same conclusion after compiling and analyzing data from multiple sources indicated in the graph below.28

Criminals prefer cash, which allows for anonymity, but no developed country financial regulation authorities, from the Federal Reserve to the Bank of England29 to the European Central Bank, seek its abolition.30 As Brainard stated in her 2021 speech at the CoinDesk conference: “The Federal Reserve remains committed to ensuring that the public has access to safe, reliable, and secure means of payment, including cash.” 31

The persistent popularity of cash informs this policy approach. A 2014 San Francisco Fed paper stated that, “consumers choose to use cash more frequently than any other payment instrument, including debit or credit cards,” especially for smaller transactions.32 This is especially the case in the United States and the United Kingdom.33

Increased Monetary Stability

One area where CBDCs might provide efficiency is monetary policy. A November 2020 Federal Reserve review of the CBDC literature states: “As a new form of central bank money, CBDC has the potential to affect central banks’ wider policy objectives, either by acting as a new monetary policy tool or through its effects on the portfolio choices of households and the probability of bank runs.”34

However, several considerations must accompany this supposed benefit.

First, a CBDC alone will not increase currency stability, which is driven by economic forces beyond CBDCs’ influence. As the March 2021 BIS report notes, “A CBDC cannot, in itself, make a currency more stable.”35

Second, evidence casts doubt on central bankers’ ability to stabilize national economies. As financial analyst Norbert Michel—then with the Heritage Foundation, now with the Cato Institute—testified in 2018 before the House Financial Services Committee’s Subcommittee on Monetary Policy and Trade:

Several studies suggest that data deficiencies caused key pre-Fed-era data to appear more volatile than their Fed-era counterparts, and there is even some evidence that the Fed era has included more economic instability than before the Fed’s creation.36 [Emphasis in original]

Third, as discussed in the next section, design choices may limit monetary policy influence if CBDCs prioritize other goals.

Fourth, policy makers must weigh any efficiencies against costs imposed in terms of loss of privacy and of financial stability.

Cross-Border Payments

CBDC proponents claim they could help facilitate international payments. As Fed Governor Brainard stated in her 2021 speech at the CoinDesk conference:

Cross-border payments, such as remittances, represent one of the most compelling use cases for digital currencies. The intermediation chains for cross-border payments are notoriously long, complex, costly, and opaque. [I]nternational collaboration on standard setting and protections against illicit activity will be required in order to achieve material improvements in cost, timeliness, and transparency.37

At a recent G7 meeting, heads of “government promised such collaboration.38 But policy makers downplay the scope of cooperation needed—which will require painstaking negotiations as countries work to safeguard financial sovereignty. As Brainard acknowledged, “a poorly designed CBDC issued in one jurisdiction could create financial stability issues in another.”39

The more countries involved the more strained negotiations become. The BIS acknowledges the difficulties, if understatedly:

Yet a single [internationally coordinated multi-CBDC] system raises a raft of policy issues for central banks. The (shared) management of the rulebook and governance arrangements for the shared system will be just one aspect. The wider implications of issuing a CBDC for monetary policy, financial stability, and payments policy will need to be worked through for each central bank, potentially requiring trade-offs in the final design. For example, central banks will need to evaluate whether they are willing to relinquish some system control and monitoring functions to an operator, for which the governance arrangements would need to be (jointly) agreed. Negotiating these trade-offs across multiple central banks will be a challenge.40

The tradeoffs could include capital controls to limit CBDC holdings by non-citizens or non-residents, which would decrease CBDCs’ usefulness.41 Political tensions could erupt if people flocked to foreign CBDCs during times of economic stress or as an investment vehicle.42

Finally, two solutions exist that could bypass potential frictions. First are private cryptocurrencies. As Fidelity Digital Assets Research Director Ria Bhutoria noted in November 2020:

Bitcoin may offer a superior option in remittances that have been burdened by slow speeds and high fees, especially to and from countries that face capital controls or struggle with high levels of inflation.43

In fact, as Alex Gladstein of the Human Rights Foundation explains, Bitcoin’s growing prowess has catalyzed cross border payments via peer-to-peer marketplaces like LocalBitcoin and Paxful that enable Bitcoin exchanges for local currency almost anywhere.44 XRP, whose linked company Ripple is currently embroiled in litigation with the Securities and Exchange Commission, has also positioned itself here.45 Others will follow.

Moreover, as the Bank Policy Institute’s Gregory Baer points out, easing current Anti-Money Laundering and Know Your Customer (AML/KYC) or Combatting Financing of Terrorism (AML/CFT) regulations would promote cross-border payment efficiency.

The solution to revitalizing correspondent networks and speeding cross-border transactions has always been obvious: establishing objective, pre-defined criteria for AML/CFT and sanctions compliance and granting banks a safe harbor from enforcement if they meet them. That is true whether the payment is in commercial bank money or in a CBDC.46

CBDC Benefits Are Dubious but the Downsides Are Certain

If implemented, CBDCs will increase governments’ financial regulatory power, with implications from macroeconomics to cybersecurity to financial privacy. CBDC supporters often present public digital money as a best-of-all-worlds—as BPI’s Gregory Baer describes it, “in some analyses, a ‘greatest hits’ approach to CBDC benefits is presented”—while glossing over necessary and complex tradeoffs.47 Yet, as the American Bankers Association noted a June 2021 statement submitted to the House Banking, Housing, and Urban Affairs Committee:

The proposed benefits of CBDCs to international competitiveness and financial inclusion are theoretical, difficult to measure, and may be elusive, while the negative consequences for monetary policy, financial stability, financial intermediation, the payments system, and the customers and communities that banks serve could be severe.48

Furthermore, a June 2020 International Monetary Fund paper stated:

Launching a CBDC is a multi-dimensional undertaking that extends beyond the central bank’s normal information technology project management frameworks.

… The new currency could lead to major disruptions affecting monetary policy transmission, financial stability, financial sector intermediation, the exchange rate channel, and the operation of the payment system.49

Beyond financial stability, tradeoffs will limit CBDCs’ usefulness. A February 2021 Federal Reserve report, in a rare acknowledgment, said:

It is important to consider that a CBDC that is designed to support monetary policy transmission or economic stimulus payments, for example, would be quite different than a CBDC that is designed to be an alternative to cash. Without clear objectives, it would be difficult to establish business requirements for a CBDC.50

Two Binary CBDC Choices Exist, and Two clear Winners Emerge, Given Governmental Priorities

CBDCs will either be “maximalist,” with central banks administering digital accounts, or “minimalist,” with commercial banks or other providers intermediating transactions and administering accounts. Furthermore, CBDCs will be either a) token-based, with cash-like properties, or b) account-based, with transactions credited and debited to and from account holders, similar to ledger transfers between merchants and credit cards and regular bank accounts.

Sen. Sherrod Brown (D-OH) and other supporters of the maximalist version want the Federal Reserve to administer individual accounts.51 (This idea originated in the 1980s.52) As a practical matter, it is unfeasible.

Private sector financial services providers already employ 20,000 people on KYC/AML compliance.53 Central banks have neither the expertise, manpower, nor desire to handle the technical issues inherent to enforcement of Know Your Customer and Anti-Money Laundering rules. As a March 2020 BIS paper notes:

For the central bank, the indirect CBDC implies loads similar to those of today’s system. By contrast, the direct CBDC would require massive technological capabilities, as the central bank processes all transactions by itself, handling a volume of payments traffic comparable with that of today’s credit or debit card operators.54

CBDCs could also be account-based. A token-based system verifies the token, while account-based verify account holders. A token-based CBDC would have anonymity traits that would hinder KYC/AML enforcement.55 That is a nonstarter for central banks.

Thus, design choices necessitate minimalist, account-based CBDCs, whereby banks or other financial services providers administer CBDC accounts and verification happens via the account holder. Given that reality, the proffered benefits of CBDCs diminish. For instance, this model limits financial inclusion because bank-administered CBDC accounts would come with fee and privacy concerns that currently dissuade many unbanked individuals from seeking commercial bank accounts.57 AML/KYC rules would require CBDCs to capture transaction data, creating a trove for government snoopers and rogue hackers. As the American Bankers Association noted in its June 2020 statement: “In many cases privacy is mutually exclusive with the objectives of AML/KYC programs.”58

CBDCs Would Fully or Partially Nationalize Banking and Create Myriad Financial Stability Risks

A February 2021 Federal Reserve report described CBDC adoption as a “potential sea change in the relationship of the central bank with the public.”59 Even if intermediated through commercial banks, it would involve an unprecedented partial nationalization. In fact, a March 2021 report by Bank of America’s brokerage arm, BofA Securities, on the prospects for adoption of a digital euro, concluded that eurozone banks could become “collateral damage” in the process.60

CBDC accounts would become direct liabilities of the central bank, rather than of FDIC-insured banks.61 This has both macro-and microeconomic implications.

First, the Federal Reserve would become a direct and advantaged competitor to private banks.62 In fact, a June 2020 Philadelphia Fed paper warned that it could enable a “deposit monopoly.”63 Depending on CBDC demand, central banks may have to hold less liquid, riskier securities, thereby influencing prices and market conditions.64 According to the Bank of International Settlements, the issuance of CBDCs may give central banks a monopoly in the provision of maturity, liquidity, and credit risk allocation.65 That would entangle central banks in credit allocation and invite politicization of the lending system as central banks become lenders of first resort.66

Second, CBDCs could jeopardize the fractional-reserve lending system. Because CBDCs would be merely assets under custody, banks could not lend them out as they do ordinary deposits.67 They could charge administrative fees to comply with KYC/AML burdens. These fees would deter use.

CBDCs could deprive private banks of their most reliable source of income: interest on loans. As BPI’s Gregory Baer notes: “The most significant impact would be a diminishment of the fractional reserve banking system in the United States, under which banks engage in maturity transformation by taking deposits and making loans.” Currently, U.S. banks fund more than $10 trillion in loans.68 This includes $2.1 trillion in consumer mortgages, $1.6 trillion in consumer loans, and $498 billion in small business loans.69 Loss of this revenue could incentivize banks to engage in riskier lending strategies and raise transaction fees, which would disproportionately burden low-income customers.

Third, passive demand for CBDCs could create volatility in government- debt markets.70 In normal times, volatility could also arise from CBDC inflows and outflows to other types of money. During economic downturns, digital runs for the perceived safety of central bank-issued currency could add to immediate and unforeseen economic stresses.71

Fourth, CBDC centralization and nationalization would invite hackers and terrorists seeking fortune or havoc. Potentially, hundreds of millions of CBDC accounts held by thousands of banks across the U.S. would create numerous points of attack for hackers.72 And unlike cash, which has physical properties that help deter large-scale fraud, digital money faces no such obstacle.

CBDCs Are Not Worth the Risk to Financial Privacy and Freedom

As Bank of International Settlements General Manager Agustín Carstens stressed during a March 2021 teleconference, central bankers’ most important charge is to “do no harm” to their country’s monetary system.73 Yet, even if policy makers could solve all challenges for adoption of CBDCs, from design to cooperation, and minimize the risks, CBDCs could still do much harm. The threats to economic freedom and financial options and potential for abuse are great.

Stablecoins Threaten Central Bankers’ Preeminence

Central banks, like any other institution, are self-interested. Their interests include maintaining relevance and prestige and thwarting competition. Stablecoins offer such competition. For central bankers, CBDCs offer a way to ban stablecoins or regulate them away.

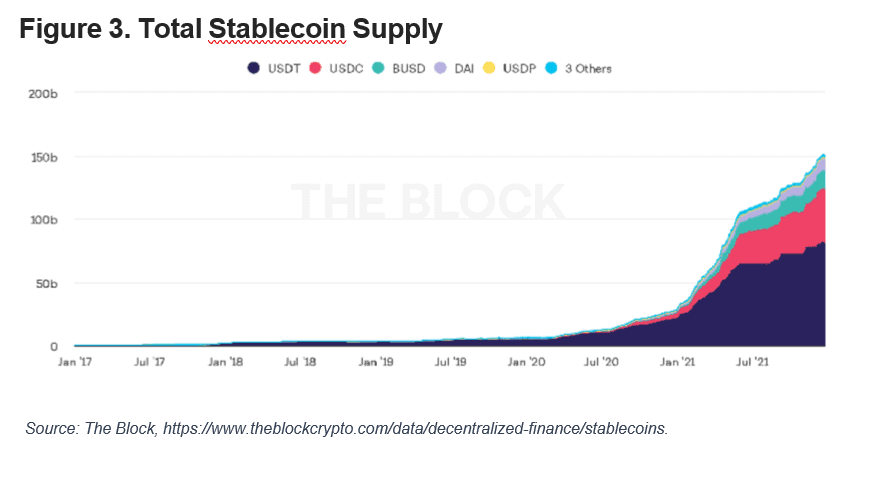

Stablecoins make the crypto ecosystem possible. They are private cryptocurrencies pegged to the value of a central bank-issued currency or some other stable monetary measure, such as gold or other commodities.

The five largest stablecoins account for two-thirds of all trading volume, despite representing less than 4 percent of market capitalization.74 By one estimate, 80 percent of Bitcoin trading volumes involved stablecoin Tether on one side.75 Stablecoins also dominate decentralized finance (DeFi), which allows users to lend, borrow, and collect interest on cryptocurrencies without a trusted intermediary. Nine of the top 10 DeFi protocols rely heavily on stablecoins.76

Stablecoins’ rapid growth shows their value and utility. In 2019, Genesis Capital, an institutional lender, reported that demand for stablecoins rose from 9.6 percent in the first quarter of that year to 37.2 percent in the fourth.77 In the first 11 months of 2021, stablecoin volume exploded from $30 billion to $161 billion.78

The approaching version of the Internet known as Web3 is based largely on two concepts: stablecoins and smart contracts that execute upon predefined conditions. Coupled together, they promise to create revolutionary ways of economic interaction. For instance, self-driving cars could pay each other to change lanes and computers could pay each other for extra storage space.79

Stablecoins can also help people to rise out of poverty. They can help maintain purchasing power and skirt capital controls amid currency devaluations or economic strife. They can offer political dissidents financial refuge from grossly mismanaged regimes like Venezuela or dictatorships like China.80 Even famously volatile Bitcoin has outperformed native currencies of major emerging economies, including Brazil, China, India, and South Africa. The Emerging Market Bond Index (EMBI) measures stability of 25 to 40 such countries. In late 2020, the one-year EMBI volatility was 31.8 percent, while Bitcoin’s was 12.4 percent.81

As the use of stablecoins has grown, self-regulating mechanisms have emerged alongside it. Currently, stablecoins USDC and Paxos publish monthly audit reports of smart contracts and reserves.82 Others, like DAI, are automated and managed by a decentralized community of Maker DAO holders—overseers of the Maker protocol, a set of smart contracts that make DAI possible.83 Still others are managed algorithmically through seigniorage shares.84

The New York Attorney General’s Office recently audited and settled with the producers of stablecoin Tether over alleged misstated reserves. Tether and related trading platform Bitfinex agreed to pay a fine and to bar New York users.85 In fact, Tether claims to have stopped serving U.S. customers entirely.86 It also recently settled with the Commodity Futures Trading Commission.87 Authorities should prosecute fraud, but fears that Tether’s reserves were nonexistent proved unfounded. A May 2021 audit revealed that Tether was backed by a combination of cash, commercial paper, secured loans, and commodities.88

Ultimately, no stablecoin can exist without trust in an environment with low barriers to entry and open competition. As Norbert Michel noted in his 2018 testimony:

In a competitive currency environment, the relative price of the competing currencies will rapidly incorporate information about current market conditions and about the supply of, and demand for, the various currencies available for exchange. Unsuccessful currencies will affect a few people a little, whereas successful ones—vetted by competitive processes—can affect many people in a more powerful manner.89

Yet, as stablecoins have emerged as a primary competitor, they have become a target for central bankers.

The Bank of International Settlements and central bankers around the world acknowledge that they would like to see stablecoins either banned or regulated into oblivion.

- In August 2020, Fed Governor Brainard cast doubt on stablecoins’ regulatory and legal status while promoting the Fed-created public payment option FedNow.90

- Bank of England Governor Andrew Bailey said in November 2020 that CBDCs would replace private stable- coins as people became more comfortable using them.91

- And in March 2021:

- A BIS paper (cited earlier) described CBDCs as a means to help “avoid competition from global stablecoins” and “preferable to proposals that involve the creation of a global private sector global stablecoin.”92

- Bank of Korea Governor Lee Juyeol stated: “When the central bank-issued digital currency is introduced, the demand for bitcoin and other cryptocurrencies as

means of payment will decrease.”93

- A Bank of America report described some countries, including China and the United Arab Emirates, working together to design mutually interoperable CBDCs as “defending their territory from cryptocurrencies,” which they want to discourage people from using.94

Short of banning stablecoins, central bankers and international bodies seek to subject them to the onerous Know Your Customer and Anti-Money Laundering rules that banks routinely face. The Financial Action Task Force, a global body that advocates for KYC/AML regulations,95 stated in October 2019 that stablecoins should “never be outside of the scope of anti-money laundering controls.”96 According to the BIS, this includes an “appropriate registration or licensing regime, which allows for adequate information and monitoring, combined with prudential requirements in appropriate cases.”97 If stablecoins cannot comply with these standards, the BIS-funded Financial Stability Board urges bans.98 This includes completely decentralized stablecoins, with no point of authority for compliance.99

In a March 2020 paper, the International Organization of Securities Commissions, a global association of securities regulators, admitted that such compliance may be “challenging” but that “systemically important stablecoin arrangements will need to adapt.”100 In November 2021, a collection of U.S. federal regulators under the banner the “President’s Working Group” called for Congress to place most stablecoins under “a federal prudential framework on a consistent and comprehensive basis” and threatened to move forward unilaterally if Congress failed to act.101

Central Bankers See Tech Firms as a Major Threat

Regulators are especially concerned by the specter of large technology companies entering financial markets. They usually distinguish between existing stablecoins and “global stablecoins,” or “systematically important” stablecoins, by which they mean produced by major technology companies.102

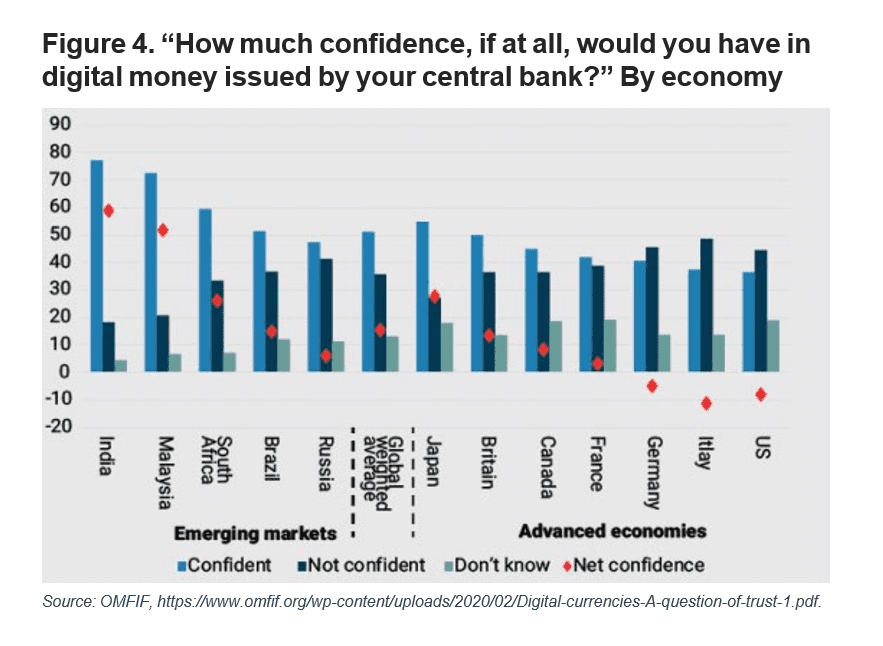

Yet, these companies may face resistance for their stablecoin products because of perceived trust issues. Some tech companies have generated mistrust through what many see as arbitrary and politicized governance of their social network forums.103 In a 2020 survey by the Official Monetary and Financial Institutions Forum (OMFIF) that asked 13,000 individuals in 13 countries, aged 16 to 75, which institutions they considered the most trustworthy, central banks scored highest at net positive 13, followed by payments services providers like PayPal, commercial banks, and credit card companies. Major technology companies finished last, at nearly a net negative 10.104 Through this and other survey results, the OMFIF concluded: “In developed markets, it appears unlikely that tech companies will be entrusted with monetary transactions.”105

In the United States, Italy, and Germany, central banks are also underwater in net trust for central bank-issued CBDCs. France’s and Canada’s central banks also have low, though net positive ratings.

This mistrust of central banks is somewhat deserved. Unlike even the largest tech companies, governments can set rules for themselves and their private competition. An April 2021 Republican congressional staff report described Brainard’s promotion of FedNow as “a striking endorsement of a public payment option framed in direct competition to a private sector innovation. It is particularly troubling given that the Fed itself … can determine the legal and regulatory status of its own competition.”106 [Emphasis in original] A European Central Bank report added: “Although central bank liabilities are not subject to regulation and oversight, in issuing the digital euro the Eurosystem should still aim at complying with regulatory standards.”107 Authorities afford private competition no such discretion.

Governments have reason to fear competition. As even CBDC-friendly scholars like Harvard’s Kenneth Rogoff admit, “the biggest threat to the value of currency is often the government itself.”108 It is not only mismanaged countries like Venezuela; currency debasement occurs worldwide. As a 2014 Bank of England report noted, “Modern-day advocates of a return to free banking, like promoters of digital currencies, have been motivated in part by their disapproval of monetary management as practiced by central banks.”109 Only open competition with private competitors will produce the best options and allow central banks to fulfill their mandate to “do no harm” to financial stability.

Governments’ Dismal Track Records on Safeguarding Sensitive Information

Botched monetary policy is not the only reason to fear government-controlled digital currency. Policy makers in the

U.S. and other Western democracies acknowledge that account-based CBDCs will compromise privacy.110 These authorities discuss “appropriate protections,” balance, privacy vouchers, and other measures.111 But Know Your Customer and Anti-Money Laundering rules will ensure governments track, record, and identify every or nearly every CBDC transaction. Privacy and KYC/AML are mutually exclusive and regulators will always choose more data when they can get it. As the March 2021 Bank of International Settlements paper cited earlier notes: “Privacy here means that the consumer’s data are used only in steps strictly necessary for the specific purpose of determining whether a transaction is lawful and, if this the case, executing it.”112

This level of government oversight could drag regulators into contentious political debates. As the American Bankers Association stated: “For controversial but locally-regulated purchases such as cannabis and firearms, a CBDC would entangle the Federal Reserve as a national arbiter of social issues.”113

Furthermore, governments have dismal track records in safeguarding sensitive data. For instance, in the past decade, the IRS apologized for targeting Tea Party groups, including by asking them invasive questions like the content of their prayers.114 Lesser known, IRS bureaucrats have leaked sensitive information about culturally disfavored groups.115 This year many high-profile individuals had their tax returns leaked.116 Last year it was the president.117 States are no better. In a recent case, Supreme Court Justice Samuel Alito scolded California bureaucrats as “grossly negligent” in their handling of sensitive nonprofit data.119 There is no reason to believe that cavalier treatment of sensitive data would not also occur at the Federal Reserve.

Adding alarm is the potential CBDC programmability. As journalist Brandon Van Neikerk explains in Bitcoin Magazine, programmable money would embed “digital packets of code that have a set of rules that can be defined by the creator and even an authorized distributor.”119 This would allow unprecedented, centralized control. As Van Neikerk points out:

Imagine a digital dollar that is equal to one U.S. dollar. This digital dollar could:

- Be tracked across every movement, where the account that is credited appends that information to the digital dollar, in perpetuity.

- Be stopped, returned to the source, returned to the previous account or even destroyed at any moment.

- Have a set of inherent rules at the source, such as a lifespan of one year, and a specified amount of depreciation per unit of time.

- Can be credited to only certain accounts, such as users who have a social credit score

of > X.120

That would have dire consequences for everyone, especially in countries with authoritarian regimes like China, where the government has established a social credit system that gives it the power to designate individuals as “Dishonest Persons Subject to Enforcement” and restrict their ability to travel, buy property, borrow money, or do anything else.121

Chinese officials eagerly await full adoption of a digital yuan. Yao Qian, a former head of the People’s Bank of China’s Digital Currency Research Institute, said in a 2018 paper that it will offer “a new way for economic control.”122 Other Chinese officials have stated that it could be used to enforce party discipline.123

China is now trying to export its CBDC model to the Bank for International Settlements.124 Worse, some Western democracies seem willing to follow China’s lead, albeit with milder aims. In discussing CBDCs, Tom Mutton,

a Bank of England director, stated in June 2021:

You could introduce programmability—what happens if one of the participants in a transaction puts a restriction on [future use of the money]?

There could be some socially beneficial outcomes from that, preventing activity which is seen to be socially harmful in some way. But at the same time it could be a restriction on people’s freedoms.125

Mutton called on the British government to decide the programmability, but given governments’ obsession with AML/KYC, some level of snooping seems inevitable.

Finally, as Van Neikerk further points out:

What we have seen in many countries around the world is the digitization and centralization of identity. Phase 1 is through bank apps on a cross-border acceptance level. This allows governments

to have a mandatory digital identification process in place to set the foundation for CBDCs.

It starts with private bank apps (which most banks already have) in a central application (a singular “bank/identity” app), but this central app can then be used for:

- Enabling citizens to confirm who they are, to anyone

- Allow the citizen to store all identification documents in one place

- Allow the citizen to use the application as a digital signature

- Allowing the government to provide their ‘services’ in one portal

- Allowing the citizen have cross-border identity

- And finally, to link payments to identification

The pieces of the puzzle are slowly coming together.

This application will, of course, be owned by the government who would also want to link the “payments” side of the application to the central bank. They wouldn’t want to privatize this arm through private banks.

Thus comes other potential mechanisms of the app, such as social credit scores (similar to what China has now).

When the central powers have your identity and they control the flow of money in an absolute manner; they will undoubtedly be able to control your behavior going forward.

A better social score, based on who knows what, could lead to lower interest rates. Maybe it could lead to some subsidies every year, straight from the government for “being good.” These hypothetical situations are not too far-fetched.126

Conclusion

Central bankers and international standard setters are naturally motivated to seek self-preservation and relevance. In Western democracies, CBDCs are a solution in search of a problem. Many CBDC promoters have sat at the pinnacle of financial power for decades. The post-World War II global order endowed domestic and international financial regulators with immense power, with mixed results. But private competition is exposing flaws that become exacerbated in times of high inflation and crisis, including pandemics. Citizens have seen mismanaged currencies and incompetence or abuse by civil servants, and doubt that any benefits would outweigh the potential costs.

Private cryptocurrencies, especially stablecoins, are solving problems, innovating, and creating opportunities in a way that central bankers cannot.

What remains for central banks is symbolism and relevance. The European Central Bank maintains that a digital euro would be “a digital symbol of progress and integration in Europe.”127 The BIS stated in 2018 that a CBDC would “help foster the public’s understanding of central banks’ roles and need for independence.”128 The Federal Reserve noted in February 2021 that a CBDC would help support its “broader work in consumer protection and community development.”129 An August 2020 report by the consultancy The Block claims that CBDCs “may help a central bank remain relevant in a world that continues to shift towards cashless payments over time.”130 From regulators’ perspective, these goals may have merit, but they fade in importance when weighed against the huge risks that CBDCs would pose for financial privacy and monetary stability.

Stablecoins, if allowed to prosper, could open a vast array of wealth-creating opportunities. Because of their crucial role in cryptocurrency trading markets, they earn substantially higher interest than savings-account central bank currency holdings. As cryptocurrency journalist Michael J. Casey noted in September 2021:

[I]ntermediary-free blockchain and smart-contract execution enables near real-time settlement of tokens and cuts out a lot of the hidden human and legal friction in the traditional credit business.131

That lack of friction translates into consumer gain. The higher interest rates that stablecoins offer consumers are only the beginning of their possibilities. Stablecoins could well fuel the coming Internet phase known colloquially as Web3. As smart contracts automate back-end management functions, ordinary citizens will benefit. In the future, cars will rent themselves, computers will lend their excess storage, and decentralized applications will share videos via predefined criteria—stablecoins will enable these and countless other and currently unimaginable transactions. This world is fast approaching. Regulators should embrace it, not seek to control it.