Australian Government Tempts Mortgage Crisis

It seems that Australia’s political parties are suffering from collective amnesia. After spending the earlier half of the year criticizing banks for abrogating their responsible lending obligations—in response to a government investigation into misconduct in the industry—both of the major Australian political parties have decided that they’re going to encourage more of it.

It seems that Australia’s political parties are suffering from collective amnesia. After spending the earlier half of the year criticizing banks for abrogating their responsible lending obligations—in response to a government investigation into misconduct in the industry—both of the major Australian political parties have decided that they’re going to encourage more of it.

With less than a week to go before the federal election, Prime Minister Scott Morrison announced that a re-elected coalition government would establish a scheme to offer loan guarantees for first homebuyers. Critical aspects of the plan are left open, such as conforming loan limits, but so far it looks like the government plans to offer a credit guarantee to 10,000 first time homebuyers, allowing them to put down only 5 percent on a mortgage instead of the standard 20 percent.

The policy was announced within the context of declining property ownership rates amongst young people. Housing affordability in Australia is a serious political issue, with house prices in cities such as Sydney rivaling those in New York and San Francisco.

But the proposed mortgage guarantee won’t solve any of these problems, just as similar policies haven’t worked in the United States. At best, it will subsidize a small group of people who would likely be able to afford a home anyway, pushing up house prices for everyone else along the way. At worst, however, it will lead to increased mortgage defaults and taxpayer bailouts.

To start with, the policy will not achieve its main purpose, making housing more affordable. If anything, higher leverage will drive up house prices. This is particularly true in a supply-constrained market like Australia.

Increasing demand through lower down payments and greater leverage, for example, is exactly what is leading to the current house price boom in the United States. One reason is that people simply buy more house. If a first time buyer has saved $40,000 and the required down payment is 20 percent, they can look to purchase a house up to $200,000. But if the down payment is reduced to 5 percent, with the government covering the rest, they could theoretically qualify for an $800,000 home (the government is yet to announce a cap on the value of the homes that would qualify). While it may be unlikely that a buyer could opt for the maximum loan amount, you can see how this mechanism would allow both buyer and seller to ratchet up the price, particularly in a sellers’ market.

This is only made worse by constraints on the supply of housing, which is quite strict in Australia. For example, a recent Reserve Bank of Australia (RBA) study found zoning raised detached house prices 73 percent above marginal costs in Sydney, 69 percent in Melbourne, 42 percent in Brisbane and 54 percent in Perth. Critically, the study concludes, if housing demand continues to grow, such as through government-supported leverage, “existing zoning restrictions will bind more tightly and place continuing upward pressure on housing prices.”

Under the scheme, borrowers will also have to pay more over the life of the loan due to higher interest rates. A high loan-to-value ratio (LTV)—a low down payment—means that a lender has a greater stake in the property, and therefore a greater risk of not being paid back. Greater risk requires higher interest rates, which translates into higher monthly payments. For example, according to one mortgage analyst, buying a $500,000 property with a 5 percent deposit instead of 20 percent deposit will cost nearly $60,000 extra over the life of a 30-year loan. The fact of the matter is that smaller deposits mean bigger interest payments over time.

It’s also not clear why the coalition government would want to speed up the home purchases of a relatively small amount of the market. It is likely that this group of people would actually be able to afford a home anyway, but are just under the required 20 percent deposit, meaning that the scheme would transfer risk from borrowers and lenders to taxpayers for little value.

The most critical aspect of the policy, however, is the government’s coercive loosening of underwriting standards. This is a dangerous game. Lenders require borrowers to put down a solid down payment for a reason, as the less equity you have in a property, the greater the chances you are of being underwater should the market turns sour.

Mortgage default is typically triggered by negative home equity. Usually, this is due to declining house prices in a low inflation environment with large mortgage balances outstanding. One key dimension of limiting default risk, therefore, is a solid down payment.

It is well documented that high LTVs increase the probability of negative home equity, and therefore, mortgage default. For example, a 2014 RBA study found that “the probability of entering arrears increases with the loan-to-valuation ratio (LVR) at origination, and is particularly high for loans with an LVR above 90 per cent.” Indeed, another RBA report also found the opposite to be true, that down payment requirements mean that new home owners are more financially stable and have fewer subsequent difficulties.

Numerous other research reports from the U.S. demonstrate that mortgages with down payment assistance have higher rates of default. Such a situation is good for no one, as homeowners lose their homes and their savings, while taxpayers are left covering the costs of bad loans.

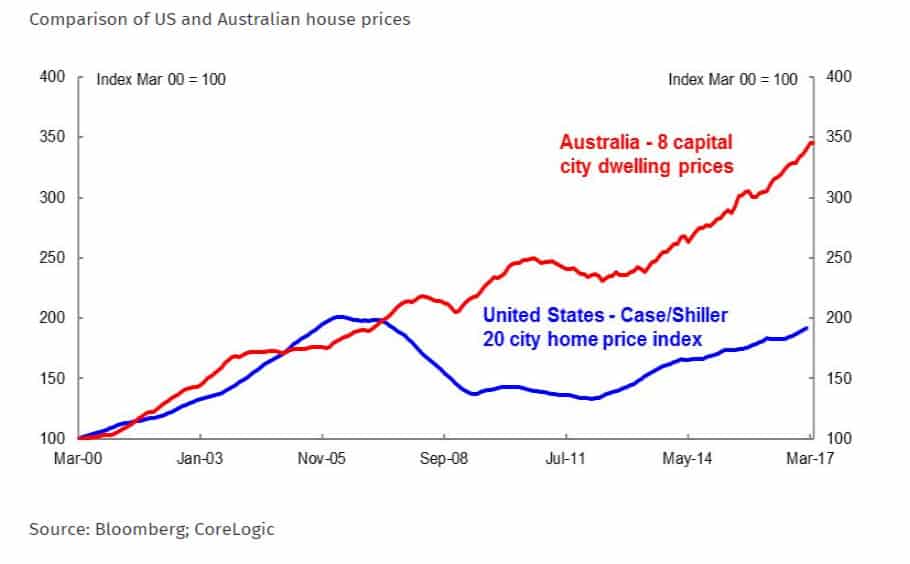

The potential risks of Australia’s extraordinary housing boom have been well documented. And yet the most important factor differentiating the Australian and U.S. mortgage market experience is that the typical Australian mortgage is prudently underwritten. As a recent Treasury Department report wrote, “Australia had a comparable run up in dwelling prices prior to the financial crisis, but with better lending standards and full recourse loans, prices did not fall significantly.”

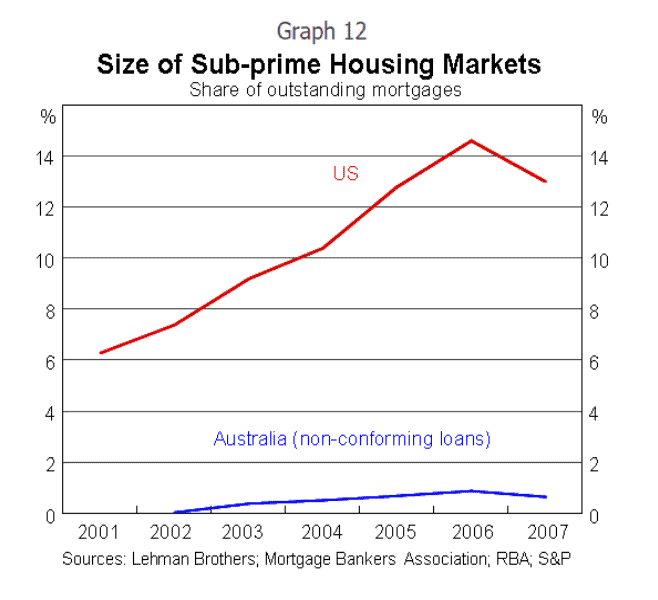

Subprime or non-conforming mortgage debt makes up a much smaller percentage of the overall Australian market than in America, and even then, Australian non-conforming loans have a less risky structure—precisely because of their lower LTVs. As one Reserve Bank Assistant Governor pointed out during the mortgage crisis:

Australian non-conforming loans have a less risky structure than US sub-prime loans. The average loan-to-valuation ratio on newly approved Australian non-conforming loans is around 75 per cent, which is lower than the average 85 per cent LVR on US sub-prime loans. There is a significant inverse relationship between LVRs and delinquency rates.

Source: Australian Department of the Treasury, “Home Ownership, Mortgage Structure and Systemic Risk.”

Source: Guy Debelle, “A Comparison of the US and Australian Housing Markets,” Reserve Bank of Australia. Note that the size of U.S. sub-prime market is significantly lower than others have found. See: Peter Wallison, Hidden in Plain Sight.

As I have written before, American housing policy has tried encouraging borrower leverage to increase homeownership for nearly a century. It has emphatically failed to either improve housing affordability or increase homeownership. Rather, it has led to an excessive increase in household leverage, which culminated in the worst financial crisis since the Great Depression. This is unequivocally not the policy that Australia should be following. Indeed, as Australia’s Treasury Department has warned, “well-intentioned policies to promote home ownership can increase systemic risk where they lead to higher household indebtedness and vulnerability.”

It is important, however, not to overstate the case. The proposed policy would apply to only a small segment of the market and only impact LTV ratios. Other key dimensions in underwriting criteria, such as credit scores and debt-to-income ratios, are equally important and won’t be impacted. But it is a worrying sign from Australia’s political parties that they are willing to forcibly denigrate underwriting standards.

Instead, it is critical that mortgages are written to withstand economic shock and a potential market downturn. Instead of last-ditch pandering to voters, the government should return to the position it supposedly held during the Royal Commission: prudent and responsible lending is critical to maintaining the safety and integrity of the Australian mortgage market.