CEI Submits Comments to the SEC on Climate Risk Disclosure, Part 2

Photo Credit: Getty

On Friday, June 11, CEI, joined by nine other free market organizations, submitted two comment letters in response to Securities and Exchange (SEC) Commissioner Allison Lee’s request for public input on how publicly traded companies should quantify and report their climate-related risks. My CEI colleague Richard Morrison wrote a comment letter focused on regulatory burdens, information markets, and the limits of producing valuable data via threat of punishment. My comment letter focuses on the flawed methodologies commonly used by climate risk disclosure advocates and the movement’s disregard of the immense risks to shareholder value entailed by the climate policies they advocate.

Among other queries, Commissioner Lee asked: What information related to climate risks can be quantified and measured? That is the foundational question. Environmental, Social, and Governance—or ESG—investors and climate activists believe that corporations should be required to report the magnitude and probability of the financial losses they could incur due to the physical impacts of climate change. They also want companies, especially fossil-fuel companies, to report their “transition” and “liability” risks—the losses they may incur as climate policies devalue and strand their assets and courts compel them to pay compensation to climate change victims.

However, objective quantification and measurement of such risks is often impossible. Climate risk assessments typically depend on multiple assumptions fraught with uncertainties. Speculative risk guestimates are of little financial value to investors. Nearly all analyses of the physical risks of climate change rely on overly sensitive climate models run with inflated emission scenarios. The assessments also often drastically underestimate the power of adaptation to reduce damages associated with even high-end warming projections.

Even analyses that purport to provide granular asset-specific analysis of climate-related impacts we have already observed rely on speculative modeling. For example, a 2018 study titled Lights Out: Climate Change Risk to Internet Infrastructure, warns that much of the Internet infrastructure of the U.S. Atlantic coast could be underwater by 2030. A leading authority on climate risk disclosure features this study in the introduction to a 60-page law review article.

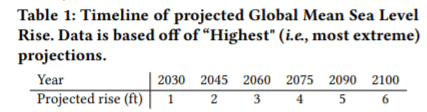

In fact, Lights Out is a cautionary tale of how dubious climate risk analysis can be. The study is explicitly based on a long-term (2018-2100) sea-level rise projection, and not just any projection but the “highest”—the “most extreme.” The study assumes sea levels will rise six feet by 2100 and one foot by 2030.

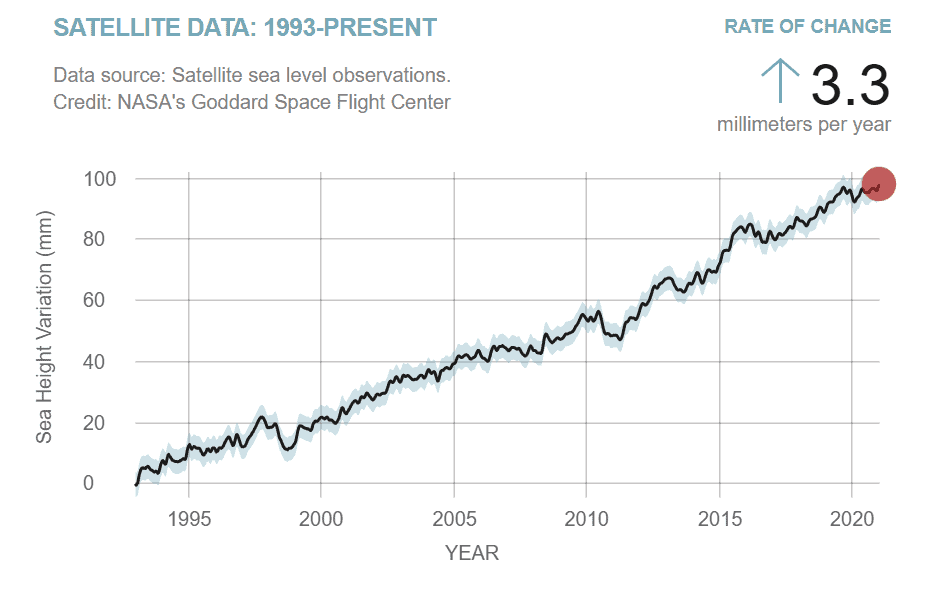

Global mean sea-levels have risen by eight to nine inches (21-24 centimeters) since 1880. The Internet infrastructure risks forecast in Lights Out materialize only if there is almost twice as much sea-level rise during 2018-2030 as there was in the preceding 138 years. The current annual rate of global mean sea level rise is 3.3 millimeters, according to the National Aeronautics and Space Administration (NASA). Lights Out assumes a 15-year rate of about 20.3 millimeters per year—more than six times faster.

The lesson here is the need for due diligence before citing climate impact assessments. Lights Out sources its “extreme” sea-level rise projection to “a collection of projected sea level rise scenarios, flood exposures, and affected coastal counties, and is amassed from a number of partner organizations.” However, the accompanying footnote takes us not to sea-level rise scenarios, models, or data but to the websites of 827 partner organizations. The study is literally non-auditable.

The nine other organizations signing on to CEI’s comments are: Committee for a Constructive Tomorrow, CO2 Coalition, Energy & Environmental Legal Institute, FreedomWorks, Heartland Institute, Heritage Foundation, National Center for Public Policy Research, 60 Plus Association, and Texas Public Policy Foundation.

Our comments develop the following points. Advocates of climate risk disclosure:

- Favor assessments based on warm-biased models run with warm-biased emission scenarios.

- Often attribute to climate change damages that chiefly reflect societal factors such as increases in population and exposed wealth.

- Overlook the increasing sustainability of our chiefly fossil-fueled civilization.

- Assume away the power of adaptation to mitigate climate change damages.

- Mislabel efforts to decapitalize companies as “protecting shareholder value.”

- Ignore the vast potential of climate policies to destroy jobs, growth, and, thus, shareholder value.

- Downplay the economic, environmental, and geopolitical risks of mandating a transition from a fuel-intensive to a material-intensive energy system.

- Downplay the regulatory impediments to building a “clean energy economy.”

- Ignore what may become the biggest transition risk—the creation of a mandate- and subsidy-fueled “clean energy” bubble.