Commonwealth Nations Beating America on FinTech Regulation

There’s a global competition between governments for who can best accommodate emerging financial technologies, and the United States is losing.

There’s a global competition between governments for who can best accommodate emerging financial technologies, and the United States is losing.

Just last week, Australia and the United Kingdom announced that they will strengthen their “FinTech Bridge,” a collaborative program between the two nations that will facilitate the entry of FinTech start-ups into each jurisdiction’s regulatory sandbox. The agreement will also include an initiative to reduce barriers to licensing for firms that are already licensed in the other country.

The agreement is fitting, given that the two nations are some of the world’s leaders for accommodating emerging financial technology. The UK is perhaps the best known, with the Financial Conduct Authority (FCA) establishing a regulatory sandbox for FinTech firms back in 2016. The FCA describes the effort as such:

The sandbox aims to promote more effective competition in the interests of consumers by allowing firms to test innovative products, services and business models in a live market environment, while ensuring that appropriate safeguards are in place.

Sandboxes, broadly, are testing grounds for new business models. It is a concept adopted from the world of software development, where a firm can test a technological proof of concept to a limited market prior to a full-scale public release. They typically require firms to file applications to the responsible financial regulator outlining how they are innovative, their benefits to consumers, their need for testing, and resolution plans if something was to go awry. Upon acceptance, firms in the sandbox are given around 1 year to test their innovative business models or products to a defined number of customers without having to become licensed financial service providers. Firms are also assigned a regulatory officer who supports the design and implementation of the test, in order to assist firms with understanding their future regulatory compliance. The regulator can issue waivers, no-enforcement action letters, or use existing statutory exemptions to facilitate the sandbox.

The current effort in the UK has largely been hailed as a success. In a reflective report one year on from the sandbox’s establishment, the FCA noted a number of promising outcomes:

- 90 percent of firms in the first cohort of the UK sandbox expected to go on to a full market launch.

- At least 40 percent of firms which completed testing in the first cohort received investment during or following their sandbox tests (due to greater regulatory certainty).

- Many firms used the sandbox test to assess consumer uptake and commercial viability.

- Around a third of firms that tested in the first cohort used the lessons learned to significantly pivot their business model ahead of launch in the wider market.

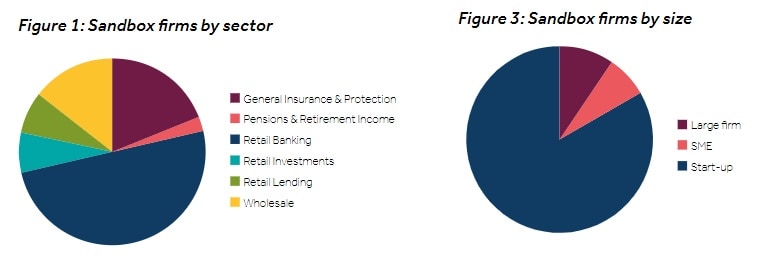

- The overwhelming majority of participants were startups and in retail banking (see figures below).

In Australia, the Securities and Investment Commission (ASIC) established an “innovation hub” in 2015. Some of the initiatives include favorable tax treatment to certain early stage FinTech investors; a potential “enhanced regulatory sandbox”; and an expanded crowdfunding regime. The enhanced sandbox will build on the original measure established in 2017, increasing the testing timeframe from 1 to 2 years and broadening the scope of activities. However, this enhanced sandbox still excludes FinTech firms that want to take household deposits and issue other financial products, such as home loans.

Partly as a result of these actions, only one-third of Australian FinTech companies see government or regulatory issues as an impediment to their expansion, although most tend to focus on relatively less regulated areas of the financial system, with only one company planning to take on the onerous regulation of retail banking.

Both approaches are far from the ideal of permissionless innovation for financial technology, as innovators must still seek the blessing of public officials before entering the sandbox and abide by certain regulations. More importantly, once firms graduate from the sandbox, they must abide by the normal, onerous regulatory structure. Further, such sandboxes are rather limited in scope. Out of 146 applications in the first year, the FCA accepted only 50, and ended up testing only 41. With a testing rate of only 28 percent, this is far below potential and could suggest that risk averse regulators will continue to throttle innovative startups. Australia fares a little better, with the Innovation Hub providing assistance to nearly 200 firms, almost 40 of which were granted new financial services or credit licenses by the end of 2017.

Despite the ample opportunity to broaden these sandboxes, more accommodative regulatory frameworks for a select number of firms is a worthy compromise. It’s certainly a more welcome structure than what the United States has provided to date. The U.S. is plagued by a largely incoherent patchwork of regulations. To operate on a national scale, FinTech firms would have to obtain licenses across all 50 states or partner with a nationally chartered bank. That process of 50-state registration can take several years and cost between $1 million to $30 million, including legal fees and direct regulatory costs. It even cost tens of thousands of dollars and many months of compliance work for a start-up to establish itself in just one state. Only one state, Arizona, has taken it upon themselves to establish their own state-based regulatory sandbox.

American financial entrepreneurs should be well placed to succeed. They benefit from access to the world’s deepest, most liquid capital markets, the most established venture capital industry, the global financial capital on the east coast and the world’s most innovative companies on the west. Despite this, the U.S. obtained a mere 33 percent of worldwide FinTech venture capital investment in 2016. Inadequate regulation surely plays an outsized role in this occurrence. According to a report on FinTech regulation issued last week by the Government Accountability Office:

…one firm we interviewed that funds fintech start-ups told us that one of their fintech firms spent half of the venture capital funds it had raised obtaining state licenses. As a result, some firms may choose not to operate in the United States. For example, one [Distributed Ledger Technology] provider we interviewed told us that although they are based in the United States, they operate abroad exclusively because state licensing costs are prohibitively expensive.

Subjecting innovative firms to 50 sets of independent state rules makes no sense and provides no added benefit whatsoever. At the federal level, centuries-old statutes covering bank chartering and capital raising smother innovative firms before they are given a chance to succeed. This is despite the fact that FinTech firms are primed to drastically disrupt the financial industry for the better, with regulatory data showing that the number of consumer complaints against FinTech firms is significantly lower than traditional financial institutions.

While the United States continues to have healthy development of financial technologies—thanks predominately to unparalleled access to capital and technology—it is at risk of falling behind to nations such as the United Kingdom, Australia, and many others who provide greater accommodation to technological disruption. In a later blog post, I will assess just what options the U.S. has at the state and federal level to build a 21st century regulatory system that welcomes the rise of disruptive financial technology instead of hindering it.