Congress Should Fix Fintech Lending Model

The House Financial Services Committee marked up a whopping 22 bills last week. While many are noteworthy, such as ending Operation Choke Point, repealing the Fiduciary Rule, and relieving regional banks from excessive regulation, there was a particularly notable exclusion. Originally announced for markup, the Protecting Consumers’ Access to Credit Act of 2017 never made it to a vote. Yet, this is one of the most important bills Congress can pass this session, as it provides a legislative fix to a damaging U.S. Court of Appeals ruling, Madden v. Midland Funding.

In Madden, the Second Circuit (covering New York, Connecticut, and Vermont) held that a loan validly made by a bank can become usurious if it is sold to a nonbank financial institution. This overturned the centuries-old “valid-when-made” doctrine, which regards loans made in one state to be equally valid when sold to a party in another state.

Centuries-old common law doctrines aside, the mistaken Madden ruling poses a real problem for financial technology (Fintech) firms and the customers they serve.

Nonbank Fintech lenders are not currently chartered at the federal level. Instead, each Fintech lender is required to charter in each the state in which it originates loans. Each state sets its own regulations with regards to interest rates. Such a patchwork of different regulations means that Fintech lenders often cannot lend to customers in other states at the same interest rates that they lend to their in-state clients. This puts Fintech lenders at a competitive disadvantage, as solely state-chartered firms cannot offer consistent products nationwide that can provide benefits from economies of scale.

To work around this regulatory problem, many Fintech lenders rely on a bank-partnership model. Banks are able to make loans in any state as long as they meet their home state’s interest rate laws. Fintech lenders cannot, and have patterned with banks to take advantage of the banks’ capability to do so. Banks originate the loans and sell them to Fintech lenders, who then service the loan and collect the payments. This is not a particularly efficient way of doing business, but it is more efficient than Fintech lenders chartering in every state in which they extend credit.

The Second Circuit’s Madden ruling, however, made this business model illegal. The court ruled that a national bank could not export a loan to a nonbank insittution and charge the same interest rate. Mercatus Center Senior Research Fellow Brian Knight summarizes the case:

In the Madden case, a New York borrower opened a credit card account with a national bank that charged an interest rate that was permitted by the bank’s home state laws but that exceeded New York’s usury cap. When the borrower defaulted, the bank sold the debt, which eventually was purchased by Midland Funding, a nonbank debt purchaser. Midland Funding sought to collect the outstanding debt, including interest that accrued after the debt had been sold. The borrower sued, and the Second Circuit held that the National Bank Act’s interest rate export did not cover the nonbank debt buyer.

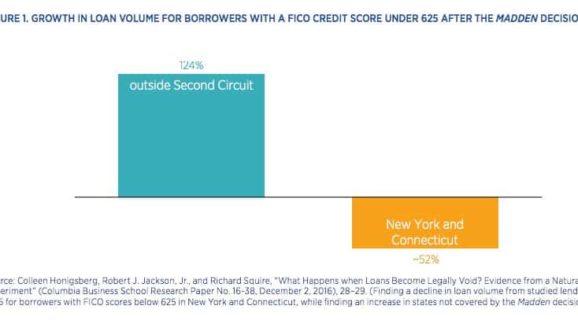

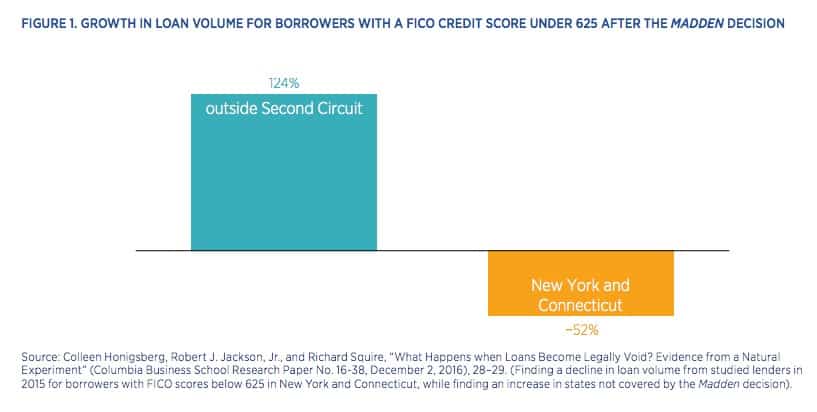

Although not involving Fintech lending, the practice has been impacted by overturning the valid-when-made doctrine. The result is to limit access to credit by inhibiting otherwise permissible banking. As Knight further illustrates, the difference in loan volume growth for less creditworthy customers has been stark:

As we can see, from 2014, the number of loans made to less creditworthy borrowers in the Second Circuit declined by 52 percent, while increasing by 124 percent outside of it. Severing the bank-partnership model has seen a decrease in credit access for those with already limited options.

The Protecting Consumers’ Access to Credit Act of 2017 provides a legislative fix to Madden. Specifically, the bill would add that a loan that is valid-when-made shall remain valid regardless of whether the loan is subsequently transferred to a third party. The valid-when-made doctrine would stand and the Fintech bank-partnership model would persist.

This is a crucial first step to fostering an open, competitive environment for Fintech companies. Technology allows lenders nationwide to offer products and services to those who are not well served by the traditional banking model, with greater competition and innovation leading to lower prices and better quality products for all.