Democratic Attorneys General Wrong on Fair Lending Laws

On Wednesday, a coalition of fourteen Democratic attorneys generals wrote a letter to the Bureau of Consumer Financial Protection urging the acting director, Mick Mulvaney, to reconsider the reinterpretation of a fair lending law, the Equal Credit Opportunity Act. Among other things, the letter claims that it would be illegal for the Bureau to rescind provisions of ECOA relating to the disparate impact standard of liability, because the statute, affirmed by Supreme Court precedent, includes language authorizing the disparate impact standard.

On Wednesday, a coalition of fourteen Democratic attorneys generals wrote a letter to the Bureau of Consumer Financial Protection urging the acting director, Mick Mulvaney, to reconsider the reinterpretation of a fair lending law, the Equal Credit Opportunity Act. Among other things, the letter claims that it would be illegal for the Bureau to rescind provisions of ECOA relating to the disparate impact standard of liability, because the statute, affirmed by Supreme Court precedent, includes language authorizing the disparate impact standard.

According to the letter, “The Supreme Court’s 2015 ruling in Texas Department of Housing & Community Affairs v. Inclusive Communities Project, Inc. dictates that the text of ECOA unambiguously provides for disparate impact liability… [holding] that disparate impact liability was provided for by the operative wording declaring that ‘it shall be unlawful . . . to discriminate against’ phrasing”.

But this is not what the statute or the court said. In Inclusive Communities, a case regarding the Fair Housing Act, recently retired Justice Anthony Kennedy stated that “antidiscrimination laws should be construed to encompass disparate-impact claims when their text refers to the consequences of actions and not just to the mindset of the actors, and where that interpretation is consistent with the statutory purpose.”

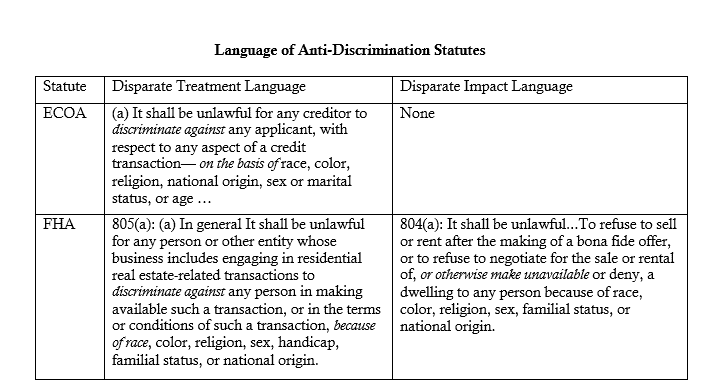

To impose disparate impact liability, a fair lending statute must invoke the “effects” of a certain policy. As detailed in the table below, the Fair Housing Act includes such language. The court thus concluded:

The results-oriented phrase “otherwise make unavailable” refers to the consequences of an action rather than the actor’s intent… this results-oriented language counsels in favor of recognizing disparate-impact liability.

ECOA, on the other hand, includes no such language, merely indicating a prohibition of discriminatory treatment. The Democratic attorneys general claim that the term “discriminate against” defines disparate impact. But as the Supreme Court made clear, and summarized in the table below, the term “discriminate against” defines disparate treatment, while language such as “otherwise make unavailable” or “otherwise adversely affect”—relating to the effects of a policy—create a disparate impact standard.

As a matter of law, the disparate impact standard of liability has no basis in ECOA. It is without foundation in the text, which the Supreme Court regarded as essential in Inclusive Communities. The Bureau of Consumer Financial Protection has the authority to rescind such provisions and should proceed with any plans to do so.