Financial Regulators’ Climate Fetish

Photo Credit: Getty

Financial regulators’ attention, both in the United States and globally, seems focused on issues far afield from their core mission at a time when turmoil is roiling global markets. Inflation is at a 40-year high and the public is overwhelmingly concerned with pocketbook issues. Yet financial regulators seem fixated on carbon emissions and potential global temperatures decades hence. They should refocus on their core mission and leave environmental concerns to the political branches.

In one sense, the focus is understandable. To discuss the current inflation crisis is to expose the embarrassing faux pas of those tasked with financial stability. Both Treasury Secretary Janet Yellen and Federal Reserve Chair Jerome Powell have meekly backtracked on prior statements about inflation’s cause and their ability to contain it.

Conversely, discussing carbon emission risks to the financial system that may materialize in the distant future yields glowing press and applause at international conferences.

Secretary Yellen has taken the lead in her role as chair of the Financial Stability Oversight Council (FSOC), a product of the Dodd-Frank law. The council has extraordinary power to bypass Congress and act unilaterally to address “emerging threats” to U.S. financial stability. In her first FSOC meeting Yellen called climate change an “existential threat” and urged a “rapid transition to a net-zero carbon economy.”

Federal Reserve chair Jerome Powell echoed Yellen’s sentiment, “One of our goals is to make climate change a part of our regular financial stability framework.”

Global financial regulators agree. In a July 11 speech, Pablo Hernández de Cos, chair of the Basel Committee on Banking Supervision for the Bank for International Settlements (BIS), the global central banking authority, spoke in strikingly similar terms. He described “a growing consensus that climate change is the most existential” challenge the world now faces. He too pushed for “Net Zero” carbon emissions citing the Glasgow Financial Alliance for Net Zero and the Net-Zero Banking Alliance.

He warned that the consequences of inaction would be dire, including a 1.5-degree Celsius rise in temperatures this century. He concluded his remarks by citing the critical need for global cooperation and the necessity to hear from “a broad set of external stakeholders.”

Those stakeholders apparently do not include the public, who must bear the brunt of the global climate push. The most obvious current stakeholders are protesting Dutch farmers whose livelihoods are jeopardized by climate-related regulations.

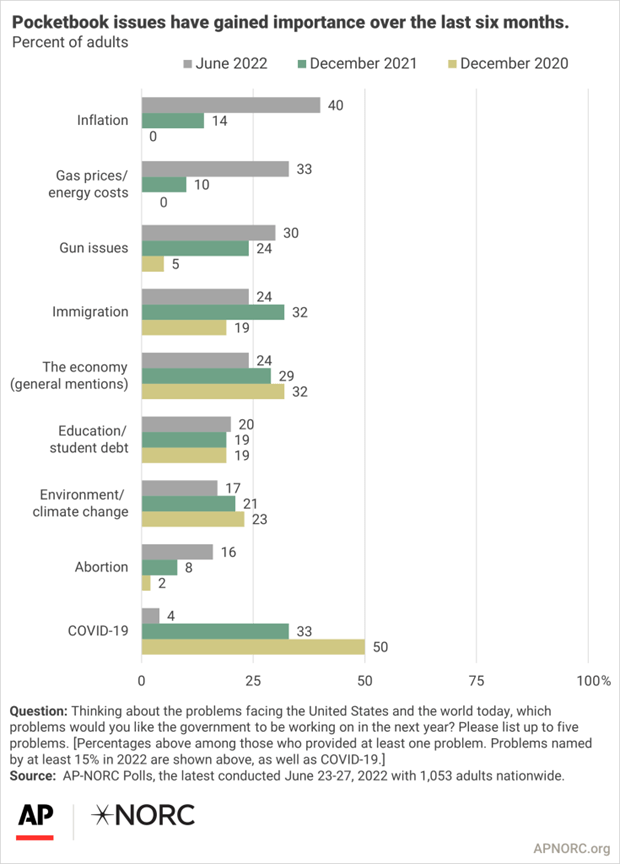

In a recent poll, Americans placed economics at the forefront of their concerns. The AP/University of Chicago poll found the top five concerns: 1. Inflation; 2. Gas prices/energy costs; 3. Gun issues; 4. Immigration; and 5. The Economy. Environment/climate change placed seventh at 17 percent—a 4 percent drop since December.

Regulators’ climate fetish also threatens cryptocurrencies, which authorities already view with suspicion because of their decentralized, private nature. Earlier this month, researchers at the European Central Bank speculated that the European Union will likely ban Bitcoin because of its energy use, even though assumptions about this topic usually come littered with fallacies.

Financial regulators should focus on their core mission of financial stability and leave climate concerns to the political branches. As Agustín Carstens, head of the BIS stated last year, financial regulators core mission is to “do no harm” to their country’s monetary system or to the citizens within it. Yet their focus on climate is doing just that at a time when their attention is urgently needed elsewhere.