New Research, Same Story: Government Housing Policy Doesn’t Work

The Urban Institute today published an updated report, titled Nine Charts about Wealth Inequality in America. As part of the project, the authors highlight the difference in homeownership of ethnic minorities, as homeownership is one of the keys to building wealth in the United States.

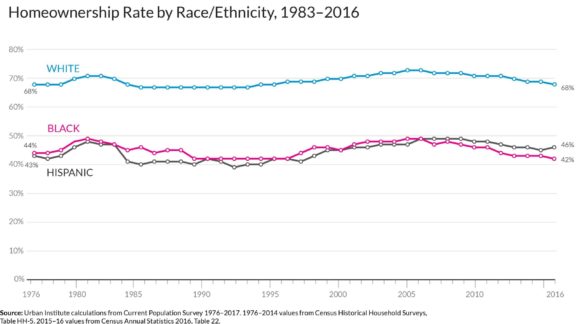

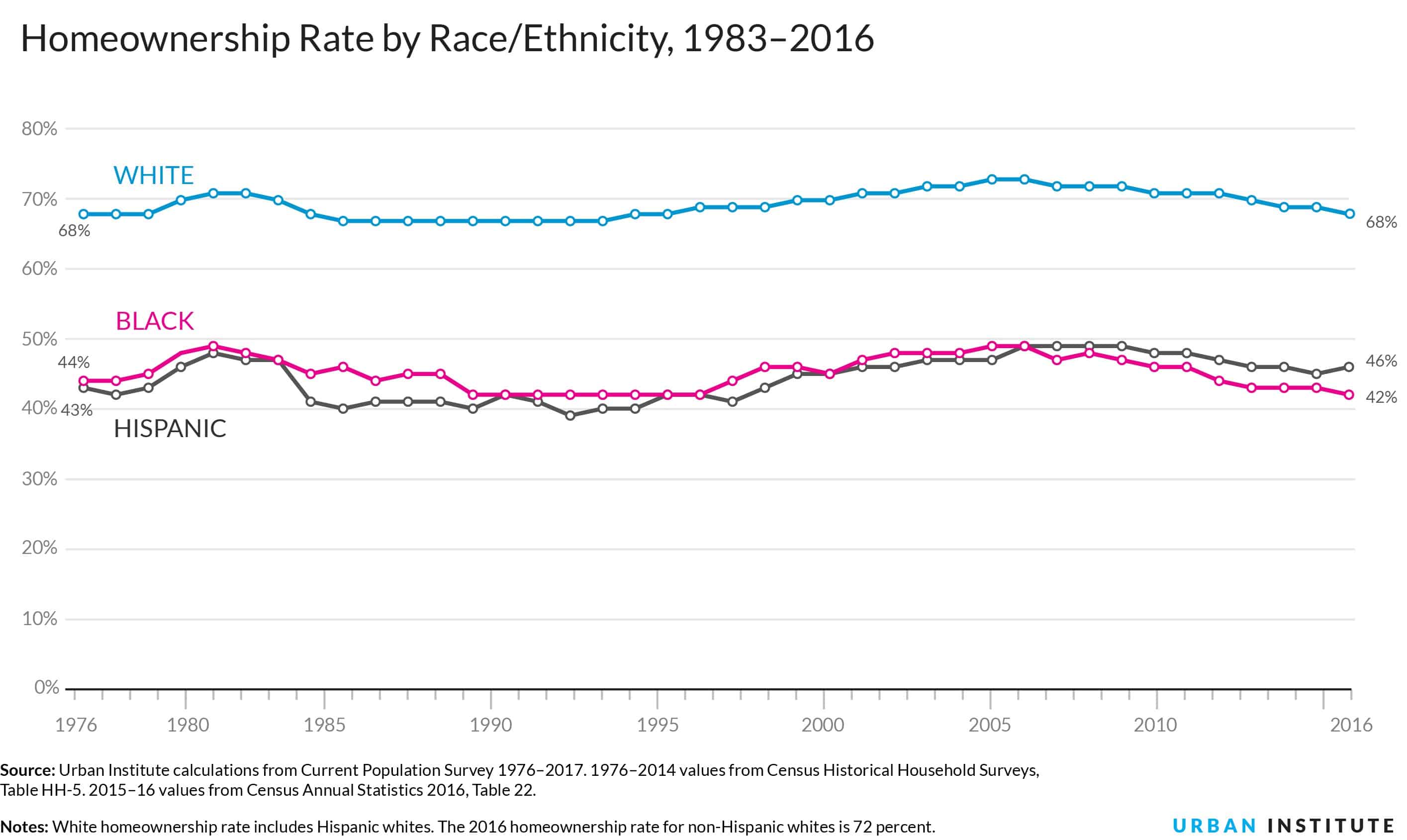

What the Urban Institute found is by no means new, but it is worth repeating. Since at least the 1970s, federal government programs to encourage homeownership have been a stunning failure. Just take a look at the chart below.

In 40 years, despite a slew of programs and subsidies, the racial homeownership gap has barely improved. In 1976, 44 percent of African American families and 43 percent of Hispanic families owned their own home. By 2016, Hispanics improved 3 percent and African Americans fell by 2 percent.

This is not due to a lack of trying. The federal government has enacted audacious minority and low-income housing goals for decades. The Community Reinvestment Act of 1977, for example, forced banks to make loans to residents of low and moderate income neighborhoods. It made it explicitly clear that banks had a legal duty to make high-risk home loans to subprime borrowers. Further, beginning in the late 1990s, the Clinton administration forced the two government mortgage behemoths, Fannie Mae and Freddie Mac, to lower their underwriting standards in order to meet affordable housing goals—at least 50 percent of their loan portfolios in subprime housing.

These policies were not without consequence. The government meddling in housing policy helped fuel the housing bubble that lead to the 2007-2008 financial crisis. By 2008, 76 percent of subprime mortgages were on the government’s books, with nearly $8 trillion in debt. Yet, despite billions of dollars of subsidies and burdensome regulations that led to the worst financial crisis in modern history, the government has failed to improve the homeownership rates of racial minorities.

One would think that such a stunning failure would force Congress to rethink its role in housing policy. Yet astonishingly, nine years on from the financial crisis, Fannie Mae, Freddie Mac, and the Community Reinvestment Act are still yet to be dealt with. Taxpayers continue to back 75 percent of newly written mortgages and as much mortgage debt today as they did during the crisis. Despite all the evidence, Congress is still blind to their ways.

Promoting affordable housing to low-income and minority households is a laudable goal, but using the government to do so has been an utter failure. A better approach would entail relieving banks of the substantial regulatory burden placed upon them, thus forcing their attention to paperwork and compliance instead of serving the needs of their community. Creating a competitive, free-market banking system will serve the needs of minority and low-income communities better than a top-down, government-led approach.