The Financial Crisis 10 Years Later: Fannie and Freddie Fueled the Subprime Mortgage Bubble

If anything symbolizes the American dream, it is homeownership—an asset that is viewed as part of a route from poverty and exclusion to independence and responsibility. However, as detailed in Part I, for over a century, state and federal governments worked to racially segregate American neighborhoods, promoting homeownership for whites while denying it for African-Americans. The result is that decades after discriminatory treatment in housing was outlawed, the homeownership gap between minorities and whites remains large.

If anything symbolizes the American dream, it is homeownership—an asset that is viewed as part of a route from poverty and exclusion to independence and responsibility. However, as detailed in Part I, for over a century, state and federal governments worked to racially segregate American neighborhoods, promoting homeownership for whites while denying it for African-Americans. The result is that decades after discriminatory treatment in housing was outlawed, the homeownership gap between minorities and whites remains large.

Such a shameful condition motivated many well-meaning activists to pressure government housing authorities to expand homeownership opportunities to minority and low-income residents. The left saw this as a way to reduce discrimination and marginalization, solving for the problems of past racism. The right saw it as a way to build an “ownership society” and give low-income earners a stake in the American dream, an anti-communist tactic first envisioned by Woodrow Wilson.

From the 1990s to the 2000s, both political parties bent the federal mortgage agencies to their will, continually relaxing underwriting standards to promote homeownership. Along with historically low interest rates, this lead to an explosion in subprime lending, which fueled the housing bubble and spread toxic mortgages throughout the financial system. Rather than a failure of the free market, the federal government was directly complicit in the mortgage market’s spectacular ramp-up and eventual collapse.

Fannie, Freddie, and the Fed

The federal housing system dates back to the Great Depression, when the Federal Housing Administration and Federal National Mortgage Association, otherwise known as Fannie Mae, were established. FHA’s role was to provide insurance for mortgages, while Fannie’s initial role was to buy mortgages that had been insured by FHA. In 1970, the Federal Home Loan Mortgage Corporation, known as Freddie Mac, was established to compete directly with Fannie, and the two were able to purchase conventional mortgages.

Fannie and Freddie did not themselves lend to homebuyers, but would buy home loans from the bank or mortgage lender, keeping them on their books or packaging them up into securities and selling them to investors. In this way, they create a liquid secondary market, so the bank got its money back and could lend even more to prospective homebuyers.

Both Fannie and Freddie are collectively known as “government-sponsored enterprises.” As a financial institution, a GSE is the worst of all possible worlds—privately owned but directed by the government, allowing the company to pocket profits in good times and saddle taxpayers with losses in bad times. Because of their implicit government backing, the two were seen as safe investments, and could therefore borrow at around 35 basis points lower than any private firm, allowing them to expand further than any of their competitors. Both are also exempt from the usual safety and soundness regulations such as strict capital requirements, holding only one-quarter of the capital required by commercial banks.

The GSEs historically focused on reducing housing costs for the broader middle class through their secondary market operations. But during the 1980s and 1990s, powerful activist groups demanded that banks reduce their lending standards, such as reliance on creditworthiness and higher down payments, and organized protests against those that would not, claiming that higher standards disproportionately hurt low-income earners and minorities. For example, in congressional testimony, one community activist, Gale Cincotta, made clear that “lenders will respond to the most conservative standards unless the GSEs are aggressive and convincing in their efforts to expand historically narrow underwriting.”

Under enormous pressure from these groups, the Clinton administration decided to expand federal government servicing of low-income and minority borrowers through various “affordable-housing goals.” Imposed in 1992, the different goals created a quota system requiring a certain percentage of the loans that the GSEs acquired each year to have been made to borrowers in financially isolated communities or those who were at or below the median income in the communities in which they lived.

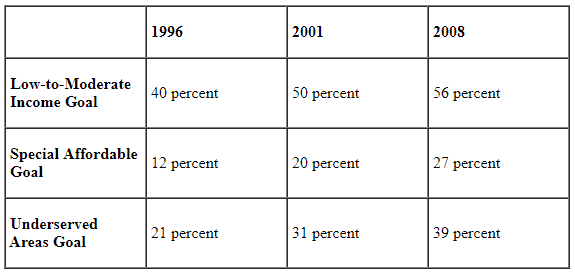

The initial low-to-moderate income quota for Fannie and Freddie was around 30 percent per year, a goal that was not too hard for them to meet. But the LMI goal was continually raised, to 40 percent in 1996, then 50 percent in 2001, and up to 56 percent in 2008. Impressively for a government agency, the GSEs hit their targets—by June 30, 2008, 57 percent of the 55 million mortgages in the financial system were non-traditional, meaning either subprime or otherwise of low quality.

As these goals were continuously raised, the GSEs found it harder and harder to find creditworthy borrowers. So in response, Fannie and Freddie had to reduce their underwriting standards, in other words, diving deep into the subprime mortgage market. This involved either reducing the accepted credit score, lowering the required down payment, raising the debt-to-income ratio, or accepting low or no documentation. As early as 1995, for example, the GSEs were buying mortgages with 3-percent down, and by 2000, they were accepting loans with zero down payment. By 2006, 45 percent of first time homebuyers were putting nothing down.

Source: Peter Wallison, “What Really Caused the World’s Worst Financial Crisis—and Why It Could Happen Again”

Interestingly, however, the affordable housing goals also induced non-subprime customers to take out larger loans for bigger homes with a smaller down payment. Lower down payments made more credit available for mortgages and thus enlarged the market for more expensive housing. For example, if a borrower had $10,000, and mortgages typically required 10 percent down, they could afford a $100,000 home loan. However, if the loan only required 5 percent down, they could now afford a $200,000 loan.Source: Peter Wallison, “Hidden in Plain Sight.”

By 2007, 37 percent of loans with down payments of 3 percent or less went to borrowers with incomes above the median. Many were speculative investors who either bought second homes or refinanced to get a bigger home. In 2000, James Grant of Grant’s Interest Rate Observer found that only 1 percent of subprime mortgages were second mortgages, while by 2006, 31 percent of subprime mortgages were second mortgages to exploit rising prices.

Fannie and Freddie, with their implicit government guarantee, were able to borrow at artificially low rates and become increasingly leveraged, dominating the home mortgage market. This drove underwriting standards lower and lower throughout the entire market. In order to compete, private lenders had to follow the GSEs underwriting standards. Indeed, as Michael Cembalest, the chief investment officer at JP Morgan, explained, “the ultimate goal [was] pushing private sector banks to adopt the same standards” as Fannie and Freddie. To be sure, the private sector made many poor decisions in going along with Fannie and Freddie, but it was the GSEs that lured many to make irresponsible loans through their secondary market operations.

The result of the government’s expansion into the subprime mortgage market was that by the time of the financial crisis, more than half of all mortgages in the United States were subprime or otherwise low quality mortgages, and the various federal government agencies were directly backing 76 percent of them. The federal government, through the GSEs, drove the subprime bubble. Columnist David Frum summarized the American housing system well for the National Post in 2008:

The shapers of the American mortgage finance system hoped to achieve the security of government ownership, the integrity of local banking and the ingenuity of Wall Street. Instead, they got the ingenuity of government, the security of local banking and the integrity of Wall Street.

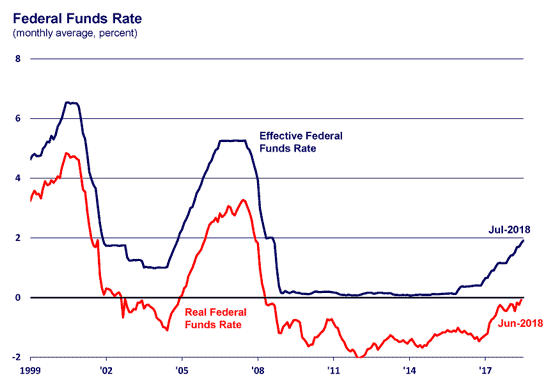

While the GSEs were aggressively providing credit to more marginal borrowers on increasingly easy terms, the Federal Reserve was drastically lowering interest rates in order to stave off a minor economic correction in the early 2000s. While we may have evaded smaller recessions, the Fed worked to throw fuel on the fire of the largest house price bubble in American history. Between 2001 and 2006, the Federal Reserve pursued the most expansionary monetary policy in perhaps 50 years. As detailed below, in January of 2001 the federal funds rate was above 4 percent, but just two years later the rate had dropped so low that it went negative for two and a half years.

Source: Federal Reserve Bank of Chicago.

Such a massive influx of credit helped spur on the housing binge. Between the GSEs’ dangerously low underwriting standards and the Federal Reserve’s easy money policies, it was virtually guaranteed that there would be an enormous housing boom. But that wasn’t the full story. As I will detail in the next post, state and local housing policies worked to restrict the supply of housing, driving prices up even further during the boom, while encouraging borrowers to walk away from their mortgages during the bust.