The Financial Crisis 10 Years Later: Restrictions on Housing Supply Makes Matters Worse

The broader financial crisis of 2007-2008 was the result of the U.S residential housing market collapse. That housing collapse itself was a consequence of an unprecedented number of weak and risky mortgages, driven predominately by the government-sponsored enterprises, Fannie Mae and Freddie Mac. When many of these mortgage holders defaulted, the mortgage-backed securities held by financial institutions around the world also buckled, leading to the financial crisis.

The broader financial crisis of 2007-2008 was the result of the U.S residential housing market collapse. That housing collapse itself was a consequence of an unprecedented number of weak and risky mortgages, driven predominately by the government-sponsored enterprises, Fannie Mae and Freddie Mac. When many of these mortgage holders defaulted, the mortgage-backed securities held by financial institutions around the world also buckled, leading to the financial crisis.

The housing bubble leading up to the crisis truly defied gravity—between 1995 and 2006, house prices had increased by 61 percent, after adjusting for inflation. While the second post in this series focused on demand factors, notably the government’s expansion of subprime mortgage financing and low interest rates, this post will look at the supply side of the bubble—namely, how land-use regulations restricted the supply of housing, pushing up prices. Further, while local laws drove up prices during the boom, state laws that enabled borrowers to “strategically” default on their loans encouraged massive defaults during the bust.

Local Land-Use Rules and State Anti-Deficiency Laws

Rather than a nationwide phenomenon, the housing bubble was really a series of local bubbles, manifesting itself very differently in different parts of the country. Generally, the real estate bubble only actually occurred in around a dozen states, such as Florida, Nevada, Arizona, and California, were home prices rose by more than 130 percent between 2000 and 2006.

What all these states had in common was tight land-use and zoning regulations that prevented certain kinds of land from being used for homes. As shown in the figure below from Cato Institute policy analyst Vanessa Brown Calder, land-use regulation has grown exponentially overtime.

The result, as predicted by a reduction in supply, is rapidly rising prices. By contrast, in those areas with less-stringent regulation, the effect of the bubble was much smaller. For example, house prices increased by only 30 percent in Texas and Georgia, even though they were two of the fastest growing states by population. When the bubble burst, the declines were much less painful. As Randal O’Toole of the Cato Institute describes in his book “American Nightmare: How Government Undermines the Dream of Homeownership”:

A careful examination of home price data for the 50 states and 381 metropolitan areas reveals strong correlations between growth-management planning and housing bubbles. On a state level, the biggest housing bubbles—with prices rising by more than 80 percent after 2000 and then dropping by 30 to 60 percent since their peak—were in California, Florida, Maryland, Nevada, and Rhode Island. All these states except Nevada have growth-management laws… Nevada’s housing supply is constrained by the limited amounts of private land available for development. Even though several of these states are located at opposite corners of the country, the price indexes are very similar.

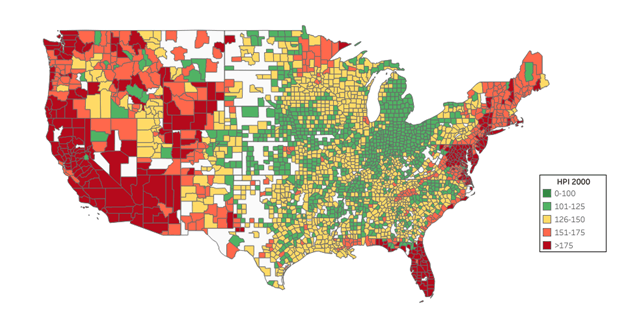

As shown in a map from the Federal Housing Finance Agency, the price change from 2000-2007 was dramatically different in different areas of the country. The areas with the largest price increases are shown in red.

There are at least two important consequences of these land use policies. First, they fed the bubble, pushing up prices. Second, they likely reinforced other ill-advised government policies. If regulation had not made housing so unaffordable, it would have been much less likely that the Clinton administration would have forced the GSEs so deep into the subprime mortgage market. As Peter Wallison of the American Enterprise Institute details in his book “Hidden in Plain Sight,” in 1989, nearly 90 percent of the U.S. housing market was considered affordable, with homes costing only three times more than annual family incomes. However, by 2005, less than 33 percent of the U.S. market was deemed affordable.

While supply-constraining regulations may have helped push the bubble to higher and higher heights, other state laws made the effect of the crash worse. So-called “anti-deficiency” or “non-recourse” laws, enacted in many of the same states with onerous land-use regulations, limit a lenders’ ability to sue a borrower after default. A non-recourse mortgage means that the mortgage is linked to the home—a borrower can walk away debt free in default. So when house prices fall and the mortgage becomes underwater (in which the debt owed is greater than the value of the property), there is a greater incentive to walk away. This is what is known as a “strategic default,” and it occurred disproportionately in states with anti-deficiency laws.

Homeowners who have built up a large amount of equity typically do not walk away from their mortgages. The problem, of course, is that new mortgages with low down payments meant that many more borrowers had little equity in their homes. As I wrote earlier, the dramatically rising house prices and lowered underwriting standards also brought many speculative investors to the market. Speculators in particular are more likely to walk away from a house if it falls in value, as they often have few ties to it. As outlined by George Mason University professor Todd Zywicki, “It is possible that the rise in default and foreclosure in the subprime market has been driven disproportionately by borrowers who lie along the speculative range of the continuum and thus have voluntarily self-selected into foreclosure.” That is to say, wealthier and more sophisticated borrowers exploited easier underwriting standards and non-recourse mortgages to speculate on rising prices, walking away from their investment homes when the market turned sour.

Throughout the 1990s and 2000s, government policy at the local, state, and federal level worked to fuel an enormous housing bubble that eventually undercut the broader financial system. But what may surprise many Americans to know is that many, if not all, of these policies remain present today. If anything, they have entrenched themselves further. In my next post, I will look at what has and has not changed over the past decade since the financial crisis.