The Financial Crisis 10 Years Later: What’s Changed?

Ten years ago, the United States plunged into a financial crisis that would bring the world economy to the brink of collapse. The primary cause of the crisis, as agreed on by people across the ideological spectrum, was the meltdown of the U.S residential mortgage market. As discussed in the second and third part of this blog series, the housing bubble was overwhelmingly a result of Fannie Mae and Freddie Mac’s reckless departure from tried and true underwriting practices, the Federal Reserve’s expansionary monetary policy, and state zoning and land-use laws that restricted the supply of housing.

Nevertheless, the federal government’s narrative that emerged from the crisis was a familiar one— inherently unstable financial markets were unleashed by deregulation during the Clinton and Bush eras, allowing for unchecked greed and risk taking. But this “deregulatory era” is a myth. As Johan Norberg outlines in his book, Financial Fiasco, over 12,000 people—around five times as many as in 1960—worked full time on regulating the financial markets in Washington, D.C., alone. Thousands more were spread around the country, working in every major financial institution.

Rather than a period of deregulation, regulatory activity continued apace, growing by 20 percent between 1990 and 2008. President George W. Bush himself increased the total cost of financial regulation by 29 percent, largely from the USA PATRIOT Act and the Sarbanes-Oxley Act.

Rather, other Clinton- and Bush-era programs were the preeminent cause of the crisis. So, what has been accomplished over the past 10 years to rein in these policies? Unfortunately, very little.

Fannie and Freddie

While the Lehman Brothers failure on September 15, 2008, is perhaps the most well-known date of the financial crisis, an arguably more important event occurred just a week earlier. On September 6, 2008, Fannie and Freddie’s regulator, the Federal Housing Finance Agency (FHFA), announced that the GSEs were severely undercapitalized and would be taken over by the government.

The FHFA had two options in dealing with Fannie and Freddie. First, it could put them in receivership, where they would eventually be wound down. Second, they could put them under conservatorship, whereby they would be recapitalized and returned to private shareholders.

One would think that such a stunning failure would force the government to end Fannie and Freddie’s meddling for good. But FHFA chose the latter option, while Congress stood by and did nothing. The GSEs, to date, have cost the taxpayer around $190 billion in bailouts, with a further $5 trillion in obligations effectively guaranteed by the federal government.

That disappointing fact should not come as a surprise when you consider that the legislative response to the crisis, the Dodd-Frank Act, was passed six months before the government body assigned to study the crisis, the Financial Crisis Inquiry Commission, finished their report. That massive piece of legislation was less concerned with evidence-based policy and more with striking while the political iron was hot. Dodd-Frank became something of a Christmas tree—strung with provisions completely divorced from the financial crisis, such as regulating debit card swipe-fees or certain kinds of minerals. But nothing was done about Fannie and Freddie.

Even still, it was obvious to even the GSEs’ biggest champions that they were complicit in the housing crisis. In 2010, for example, House Financial Services Committee Chairman Barney Frank admitted he was wrong about the GSEs. “I hope by next year we’ll have abolished Fannie and Freddie. … [I]t was a great mistake to push lower-income people into housing they couldn’t afford and couldn’t really handle once they had it.”

But that never materialized, and the GSEs today remain as dominant as ever. As my colleague, John Berlau described in his paper, “Fannie Mae and Freddie Mac Still Endanger U.S. Economy,” nearly 90 percent of new U.S. mortgages are backed by Fannie, Freddie, and other government agencies, compared to just under 50 percent in the years before the crisis.

In other words, the federal government is standing behind virtually all new mortgages today. According to Berlau, “Already, stress tests conducted by the Federal Housing Finance Agency show that Fannie and Freddie may need up to $100 billion in new bailout money if there are changes in interest rates or economic volatility.”

Instead of winding down the two behemoth mortgage agencies most responsible for the crisis, taxpayers continue to back as much, if not more, mortgage debt today as they did during the bubble. The failure to end Fannie and Freddie’s rein represents perhaps the greatest missed opportunity of the crisis.

Housing Affordability

Ironically enough, the supposed purpose of the GSEs is to make housing more affordable. Yet as we have seen, housing has only become more and more unaffordable since at least the 1990s and the homeownership rate remains virtually the same as in the 1960s. The focus on increasing borrower leverage through federal mortgage programs has been ineffective at making housing more affordable. As Heritage Foundation scholar Norbert Michel recently wrote for Forbes:

The legacy of the GSEs, as it would be with any such private-public partnership, is crony capitalism, higher mortgage debt, higher home prices, taxpayer bailouts, and no appreciable expansion of homeownership.

Indeed, this problem has only gotten worse as a result of state and local regulations that make it harder to build houses. That is in part why home prices across the country are higher today than they were before the crisis. As The Wall Street Journal recently reported, fewer homes are being built per household than at almost any time in American history.

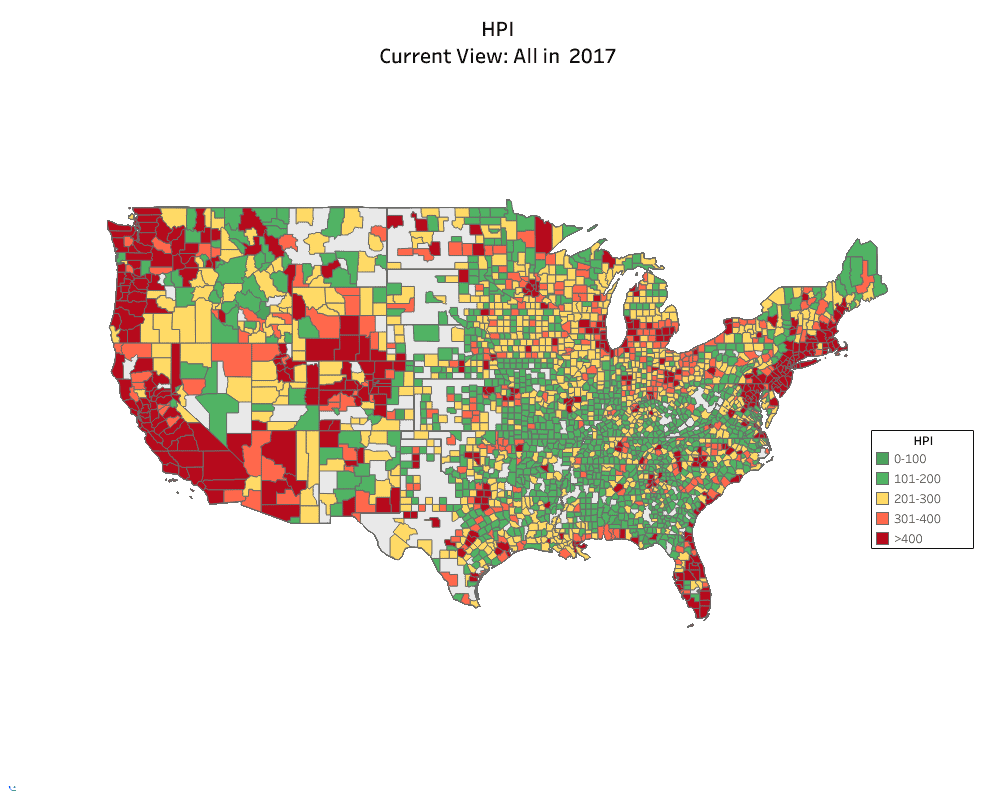

As detailed in the third blog post in this series, research from the Cato Institute has found that land-use and zoning regulation has increased exponentially over the years. Further, the National Association of Home Builders estimated in 2016 that an average house cost around $85,000 more due to regulation, up more than 30 percet since 2011. As can be seen from the FHFA House Price Index for 2017 below, many of the same states that experienced the largest bubbles are again experiencing the greatest price increases.

Today, just as decades earlier, government policies are working to restrict the supply of housing while at boosting its demand, once again driving excessive increases in housing prices. In other words, the housing system is functioning in substantially the same way it functioned before the crisis. And just as before, these housing booms cannot last.

While predicting exactly what will cause a broader financial crisis the next time around is an impossible task, it is bewildering that the same policies that caused the last housing bubble are even further entrenched than before. At the very least, the government’s housing footprint will make housing more unaffordable and more unstable, with even larger taxpayer bailouts for Fannie and Freddie when the next housing downturn comes. Clearly, neither Congress nor the federal regulators learnt the lessons of the last housing bust.

In the last part of this blog series, I will look at some reform options for how private capital and free enterprise can replace the government’s central role in the housing system.