CEI Comments on Volcker Rule Relief

View CEI Led Coalition Letter in Support of Volcker Rule Relief

Re: Proposed Revisions to Restrictions on Proprietary Trading and Certain Interests in, and Relationships with, Hedge Funds and Private Equity Funds (84 FR 2778, Feb. 8, 2019).

On behalf of the Competitive Enterprise Institute (“CEI”), we are pleased to provide the following comments on the notice of proposed rulemaking to implement amendments to section 13 of the Bank Holding Company Act, commonly known as the Volcker Rule, contained in section 203 and 204 of the Economic Growth, Regulatory Relief, and Consumer Protection Act, S. 2155, Pub.L. 115–174 (“EGRRCPA“).

Founded in 1984, CEI is a non-profit research and advocacy organization that focuses on issues of overregulation. A major objective of CEI is on removing regulatory barriers that inhibit access to capital for businesses, consumers, and entrepreneurs. CEI has been involved in previous efforts to reform the Volcker Rule, first commenting on the rule’s revision in 2017.[1]

At issue in this proceeding is a regulation to implement EGRRCPA. In CEI’s view, the proposed regulation is contrary to the statute. The proposed regulation would regulate a number of banks that should be exempt under the statute—primarily, banks with more than $10 billion in assets but less than 5% trading assets. The agencies cannot expand the scope of regulated entities beyond that set forth by Congress, and for that reason the proposed regulation is invalid.

I. The Text of the Proposed Regulation Is Inconsistent With the Text of the Statute

EGRRCPA amended 12 U.S.C. § 1851(h)(1) to include the following:

[T]he term “insured depository institution” does not include an institution-…

(B) that does not have and is not controlled by a company that has-

(i) more than $10,000,000,000 in total consolidated assets; and

(ii) total trading assets and trading liabilities, as reported on the most recent applicable regulatory filing filed by the institution, that are more than 5 percent of total consolidated assets.

The agencies correctly describe the language of the statute initially,[2] and then again correctly later in a footnote.[3] Nonetheless, their proposal does not accurately follow the statutory text. “The usual meaning of the word ‘and,’[in (B)(i)] is conjunctive, and ‘unless the context dictates otherwise, the ‘and’ is presumed to be used in its ordinary sense.” See Reese Bros. v. United States, 447 F.3d 229, 235–36 (3d Cir. 2006). But, the proposed regulations, 12 CFR §§ 44.2, 248.2, 351.2, 17 CFR§§ 75.2, 255.2, have negated part B of the statute without properly changing the word “and” to “or,” as underlined and bolded below:

(r) Insured depository institution . . . does not include:…

(2) An insured depository institution if it has, and if every company that controls it has, total consolidated assets of $10 billion or less and total trading assets and trading liabilities, on a consolidated basis, that are 5 percent or less of total consolidated assets. (Emphasis added.)

The phrase “more than $10,000,000,000 in total consolidated assets” in the statutory text has been transformed to “$10 billion or less” in the regulation, and the “more than 5 percent” of traded assets in the statutory text has been transformed into “5 percent or less.” Contrary to the rules of grammar dealing with negatives, the “and” between subsections (i) and (ii) was not transformed to an “or”; for that reason the resulting proposed regulation is not consistent with the statute.

Normally, the term “and” in a statute is understood to be a conjunction. When a conjunction is negated it becomes a disjunction. It is conceivable that, in certain circumstances, the context of the term might justify another reading, but the agencies have made no showing whatsoever that this is the case here. In fact, the agencies appear to be oblivious to the need to do so. Not a single sentence of the proposal presents any justification for the agencies’ approach.

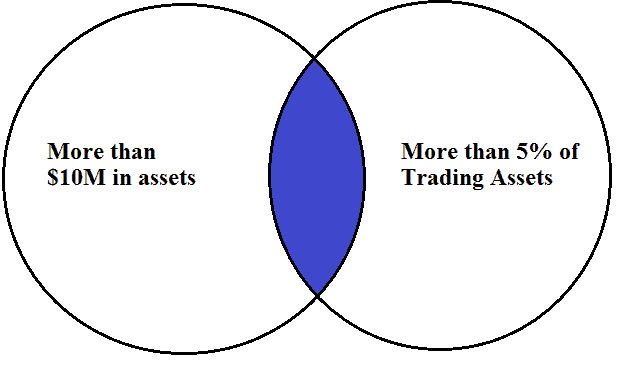

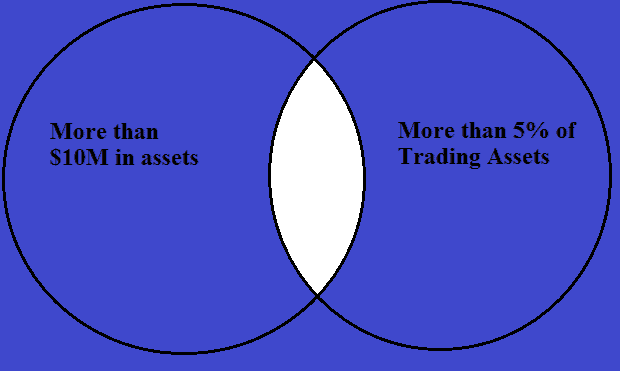

The statute is intended to reduce the category of regulated institutions to those that are combinations of two characteristics—having more than $10 billion in assets, and trading assets and liabilities that exceed 5 percent of total assets. The agencies, however, have ignored the fact that regulated banks must have both of these characteristics rather than either one individually. The end result of their approach is to regulate more institutions than those specified by Congress.

The cause of this is the agencies’ treatment of the term “insured depository institution”. Leaving aside (for the sake of simplification) the factor of control, under the statute a regulated “insured depository institution” is one that has both (1) more than $10 billion in total assets and (2) more than 5 percent total trading assets and trading liabilities. But this means that if a bank does not have both characteristics, then it should not be regulated. If, for example, it has one but not the other, then it is not regulated. But under the agencies’ proposal, if a bank has either characteristic by itself, then it is regulated. This is contrary to the statute.

AN ICE CREAM ANALOGY

We can analogize the situation to a hypothetical involving ice cream. Imagine that ice cream products, in general, have been an extensively regulated category, but then a new statute narrows that category to consist of only mint chocolate ice cream. Clearly, to fall into that new category, an ice cream must be both mint and chocolate. If an ice cream is not mint, or if it is not chocolate, then it is excluded from regulation under the statute’s new, narrower definition.

In short, the statute creates two alternative criteria for excluding certain types of ice cream from regulation: all ice cream that isn’t mint is excluded, and all ice cream that isn’t chocolate is excluded. But under the agencies’ proposal, there is only one exclusion criterion—ice cream that is neither mint nor chocolate. This is clearly contrary to the statute—the latter excludes both plain mint and plain chocolate from regulation, while the proposal includes them.

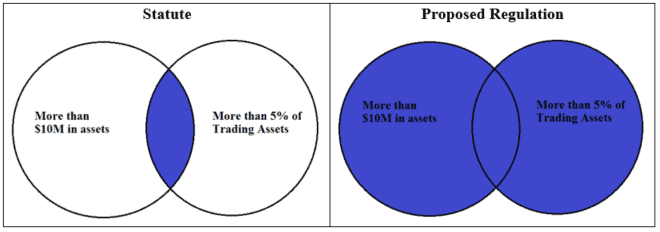

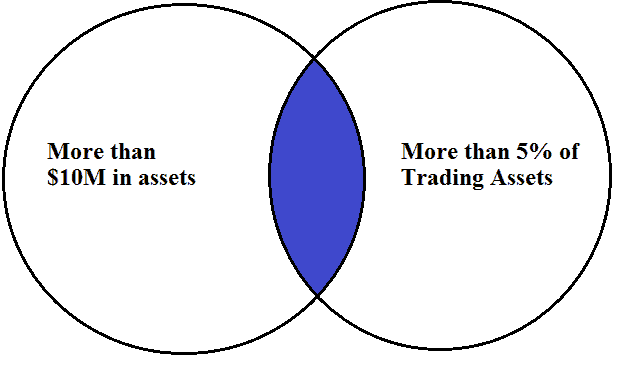

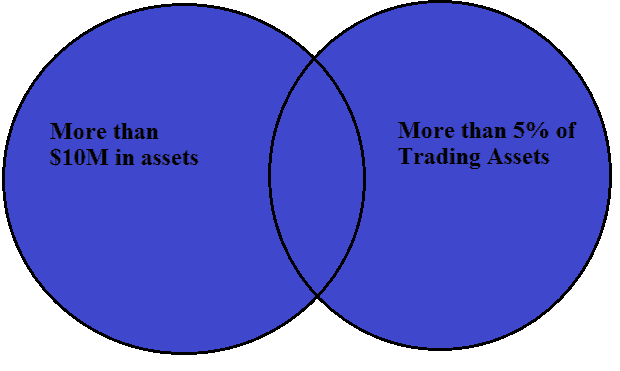

LOGIC TABLES AND VENN DIAGRAMS ALSO DEMONSTRATE THE PROPOSAL IS INCONSISTANT WITH THE STATUTE

The well-accepted rules of basic logic, including logic tables and Venn diagrams, also show that the proposed regulation does not have the same meaning as the statute. This can be seen in Appendix A, which sets out the full series of steps used to create the diagrams. The end results of the statute and the proposed regulation are shown below, where the shaded sections represent those banks that fall under regulation:

As can be seen above, the shaded section of the proposed regulation far exceeds that of the statute, because the regulation has a far different meaning than the statute. This is clearly illegal.

II. The History of the Statutory Volcker Rule Similarly Demonstrates the Proposed Regulation Is Contrary to the Law

On February 3, 2017, President Trump issued Executive Order 13772, a “Presidential Executive Order on Core Principles for Regulating the United States Financial System.” That order stated: “It shall be the policy of my Administration to regulate the United States financial system in a manner consistent with the following principles of regulation, which shall be known as the Core Principles:

(a) empower Americans to make independent financial decisions and informed choices in the marketplace, save for retirement, and build individual wealth;

(b) prevent taxpayer-funded bailouts;

(c) foster economic growth and vibrant financial markets through more rigorous regulatory impact analysis that addresses systemic risk and market failures, such as moral hazard and information asymmetry;

(d) enable American companies to be competitive with foreign firms in domestic and foreign markets;

(e) advance American interests in international financial regulatory negotiations and meetings;

(f) make regulation efficient, effective, and appropriately tailored; and

(g) restore public accountability within Federal financial regulatory agencies and rationalize the Federal financial regulatory framework.”

Executive Order 13772 also required that the Secretary of the Treasury issue a report that “shall identify any laws, treaties, regulations, guidance, reporting and recordkeeping requirements, and other Government policies that inhibit Federal regulation of the United States financial system in a manner consistent with the Core Principles.”

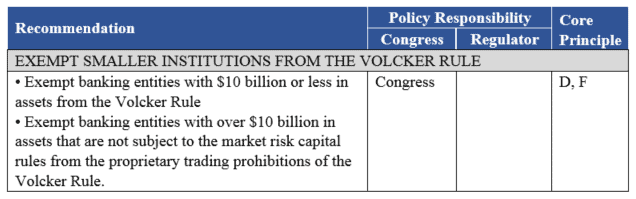

On June 12, 2017 the U.S. Department of the Treasury issued its first report under this executive order, entitled “A Financial System That Creates Economic Opportunities” with the subtitle “Banks and Credit Unions.”[4] The report’s executive summary stated: “Banks with $10 billion or less in assets should not be subject to the Volcker Rule. Treasury also recommended that the proprietary trading restrictions of the rule not apply to banks with greater than $10 billion in assets unless they also exceed a threshold amount of trading assets and liabilities.”[5] Congress did exactly what Treasury recommended in the portion of the EGRRCPA, except that Congress exempted such institutions from the Volcker Rule entirely rather than just from the proprietary trading restrictions.

The report explained in detail Treasury’s view that the Volcker Rule should not apply in two separate situations—either in the case of low total assets or in the case of a low percentage of trading assets:

Applying the Volcker Rule to firms whose failure would not pose risks to financial stability, or to firms that engage in little or no proprietary trading or covered funds activities, imposes substantial regulatory burdens but offers little benefit. Therefore, as described below, firms that are small or do not engage in significant proprietary trading should not be subject to the Volcker Rule.[6]

Treasury went on to explicitly explain why even banks with more than $10 billion in total assets should nevertheless not be subject to the full Volcker Rule if the percentage of their trading assets were low:

Banks with over $10 billion in assets should not be subject to the burdens of complying with the Volcker Rule’s proprietary trading prohibition if they do not have substantial trading activity. A further exemption from the proprietary trading prohibition should be provided for all consolidated banking organizations, regardless of size, that have less than $1 billion in trading assets and trading liabilities and whose trading assets and trading liabilities represent 10% or less of total assets.[7]

In Appendix B to its report, Treasury created a “Table of Recommendations” which included the following[8]:

All of the above examples show how the proposed regulation is inconsistent with the recommendations of Treasury adopted by Congress.

Congress implemented the suggestions by Treasury in EGRRCPA, which was first introduced, in slightly modified form, five months after the report’s publication. Originally, Treasury recommended exempting those institutions greater than $10 billion in total assets but with “less than $1 billion in trading assets and trading liabilities and whose trading assets and trading liabilities represent 10% or less of total assets” from the proprietary trading prohibitions. Congress made this exemption a stricter, only applying to institutions with trading assets less than 5% of total assets, but wider exemption, exempting such institutions from the Volcker Rule entirely.

Congress implemented almost exactly what Treasury had asked for, and yet now in creating the regulation to implement it, the agencies are oblivious to those recommendations of Treasury. Many of the institutions that Treasury itself has said should not have the proprietary trading prohibitions in the Volcker Rule would still be under such restrictions in the proposed regulations. There is no basis for the proposed regulation’s interpretation of the statute in the text or history of this statute.

The decision by Congress to implement the Treasury proposal was a compromise position. In the House of Representatives, the Financial CHOICE Act of 2016, H.R.5983, was first introduced in 2016 and showed strong support for abolishing the Volcker Rule entirely. When it was re-introduced in the Financial CHOICE Act of 2017, H.R. 10, it passed the House with a vote of 233 to 186. With many in the House seeking to entirely abolish the Volcker Rule, the Treasury proposal acted as a kind of middle ground that could garner broader support. After passing the House, the Financial CHOICE Act of 2017 was received in the Senate and referred to the Senate Committee on Banking, Housing, and Urban Affairs on June 13, 2017, one day after the Treasury report was published. So there were competing proposals before the committee: to entirely abolish the Volcker Rule or limit the full rule to those with more than $10 and a large percentage of trading assets. Congress chose the latter. The approach of the proposed regulations was never considered by Congress.

There is evidence in the congressional record that Congress knew precisely which institutions would still be effected by the Volcker Rule. In a letter entered into the record called “FACT versus Fiction” and signed by “From the offices of U.S. Senator Joe Donnelly (D-IN) U.S. Senator Heidi Heitkamp (D-ND) U.S. Senator Jon Tester (D-MT) U.S. Senator Mark Warner (D-VA),” it states: “Congressman Barney Frank, one of the authors of Dodd-Frank, has written that if this ‘bill became law tomorrow… There would be no change at all in the law as it applies to J.P.Morgan Chase; Bank of America; Wells Fargo; Morgan Stanley; Citicorp; or Goldman Sachs.’”[9]

Those six institutions listed by members of Congress in the committee which created this bill are institutions that have both more than $10 billion in total assets and more than 5% trading assets relative to total assets. The banks listed are the only banks with more than $50 billion in total assets that would be covered under a proper interpretation of the rule.[10] There are a few other U.S. banks which have both more than $10 billion in total assets and more than 5% trading assets relative to total assets, but none of the listed banks have less than 5% trading assets.[11] Under the proper interpretation of the statute, those six institutions would still be subject to the Volcker Rule.

Moreover, the chairman of the relevant House subcommittee personally informed the agencies that their proposed rule “directly contradicts the statute.”[12] The chairman specifically identified the “and” in the proposed regulation as incorrect, noting that it should instead be an “or.”[13] The letter ends in a request that we echo in our comments: “I urge you to respect this hard-fought legislative agreement through the use of our precise and carefully considered statutory text as you proceed to implement the EGRRCPA.”[14]

III. The Agencies’ Proposal Fails to Carry Out the Purpose of the Amended Volcker Rule

The text of the EGRRCPA remains the most important factor in implementing the revised Volcker Rule. However, even when looking past the text to what the Volcker Rule was intended to achieve as a matter of policy, it is clear that our reading more faithfully accomplishes its original purpose.

The Dodd-Frank Act was instituted as a response to the financial crisis. As one prong of that response, the Volcker Rule aimed to limit federally insured banks’ ability to engage in proprietary trading and to invest in or sponsor hedge or private equity funds. The theory behind the rule was that proprietary trading by some of the largest and most “systemically important” financial institutions was a proximate cause of the financial crisis.[15] By prohibiting certain types of “risky trading,” the Volcker Rule would prevent a repeat of the crisis.

However, the original Volcker Rule did not consider all instances of proprietary trading as “too risky.” For example, it leaves other entities such as hedge funds to continue the practice. It also includes exemptions for trading in government securities and for market-making and hedging activities. It is clear, therefore, that not all assets, industries, and institutions need to be covered by the rule to achieve its desired effects.

The theory behind the original Volcker Rule was flawed and the policy response unnecessary.[16] An even greater flaw, however, was to broadly apply the Volcker Rule to institutions that pose little-to-no risk to the broader financial system and to those that engage in negligible asset trading.

The original Volcker Rule is concerned with the potential of systemically important commercial banks to fail as a result of proprietary trading. Yet small and medium size banks are not “systemically important,” and a substantial number of larger institutions do not engage in even a small amount of asset trading. The breadth of the regulation is therefore confusing. If these banks are not large and interconnected enough to pose a “systemic risk,” or if they do not engage in “risky trading,” then why are they covered by the regulation?

Given that the rule was designed to reduce the likelihood of systemic failure, it would make more sense to apply the Volcker Rule to those “large” institutions that do engage in large amounts of trading. This is the position advanced by the 2017 Treasury Department Report, which advocated that banks under $10 billion in assets and banks over $10 billion in assets with relatively limited trading assets and liabilities should be exempt from requirements of the Volcker Rule.[17] As highlighted above, the report stated:

Applying the Volcker Rule to firms whose failure would not pose risks to financial stability, or to firms that engage in little or no proprietary trading or covered funds activities, imposes substantial regulatory burdens but offers little benefit. Therefore… firms that are small or do not engage in significant proprietary trading should not be subject to the Volcker Rule.[18]

This is precisely what the amended Volcker Rule seeks to do: if you are one of the largest institutions (over $10 billion in consolidated assets) and are involved in a large amount of trading (total trading assets and trading liabilities, on a consolidated basis, that are more than 5 percent of total consolidated assets), you are covered by the rule. Such a reform does not betray the original intent of the Volcker Rule. If anything, it is a much more sensible application of the policy than what was originally promulgated, covering only those institutions that pose a genuine risk as defined by the policy.

The difference in the level of coverage between the two interpretations is drastic. Under the correct interpretation of the statute, the Volcker Rule would cover only 26 banks. Under the agency’s proposal, the Volcker Rule would cover hundreds more banks.

Indeed, this more tailored construction is what was originally envisioned for the rule. Paul Volcker himself explained that he thought the rule would only impact the four of five largest banks,[19] an indication that these were the only institutions that engaged in the kind of activities that were intended to be prohibited.[20]

The correct interpretation more faithfully fulfills the purpose of the Volcker Rule by tailoring its prohibitions rather than applying it to all banks even if they engage in negligible trading. CEI has long supported this more tailored construction. In the past, we have advocated for the tailoring of the rule to the trading of the very largest banks by integrating the rule into the regulation of Global Systemically Important Financial Institutions (G-SIBS).[21] As one CEI scholar wrote during the Congressional debates over what became the EGRRCPA, “If the Volcker Rule should exist at all, it should at least focus on the few largest firms that have significant trading activities.”[22]

IV. Conclusion

The Economic Growth, Regulatory Relief, and Consumer Protection Act of 2018 was the first significant piece of financial reform passed since the Dodd-Frank Act of 2010. It is imperative that the regulatory agencies charged with implementing the statutory amendments do so in a way that faithfully executes the Congressional mandates.

Unfortunately, the current proposed rule to revise the Volcker Rule is not faithful to the text of EGRRCPA. The text is explicit, and agencies do not have the authority to finalize a rule that conflicts with it. The proposal is an illegal usurpation of Congress’ legislative power.

CEI respectfully submits that the above regulatory agencies implement the correct statutory mandate set forth in the EGRRCPA, as described in section I of these comments. The proposed rule should be revised to only include banks that have both total consolidated assets of $10 billion or more and more than 5 percent trading assets, as the statute requires.

Respectfully submitted,

Devin Watkins, Attorney

[email protected]

Sam Kazman, General Counsel

[email protected]

Daniel Press, Policy Analyst

[email protected]

John Berlau, Senior Fellow

[email protected]

Competitive Enterprise Institute

1310 L Street NW, 7th Floor

Washington, DC 20005

(202) 331-1010

Appendix A

Formal Logic Proves That the Regulation’s Meaning Does Not Match the Statute

It is a well-settled principle of logic that “the negation of a conjunction is logically equivalent to the disjunction of the negations of its conjuncts.”[23] This principle is known as “De Morgan’s Law” or “De Morgan’s Theorems”; it states that the proposition that NOT (P AND Q) is equal to (NOT P) OR (NOT Q).

It follows that for the resulting statement to have the same meaning, negating a sentence with an “and” transforms the “and” into an “or.” This was not done in the proposed regulation, and so the proposed regulation does not have the same meaning as the statutory language. This can be demonstrated via a logic table:

Correct Understanding of the Statutory Language

|

(A) Has > $10M in assets |

(B) Trading > 5% total assets |

A and B |

Company Does Not Have (A and B) |

Is an “insured depository institution” |

|

TRUE |

TRUE |

TRUE |

FALSE |

TRUE |

|

TRUE |

FALSE |

FALSE |

TRUE |

FALSE |

|

FALSE |

TRUE |

FALSE |

TRUE |

FALSE |

|

FALSE |

FALSE |

FALSE |

TRUE |

FALSE |

Regulation’s Incorrect Understanding of the Statutory Language

|

(A) Has > $10M in assets |

(B) Trading > 5% total assets |

Company Has Not A and Not B |

Is an “insured depository institution” |

|

TRUE |

TRUE |

FALSE |

TRUE |

|

TRUE |

FALSE |

FALSE |

TRUE |

|

FALSE |

TRUE |

FALSE |

TRUE |

|

FALSE |

FALSE |

TRUE |

FALSE |

The two logic tables are not equivalent concerning the meaning of an “insured depository institution”, because the regulation is not equivalent to the statutory meaning.

Venn Diagrams Demonstrate the Proposed Regulation Is Inconsistent With the Statute

There is a double negative in the statutory language (when defining an “insured depository institution”), and so each of the two negation steps will be shown below in a different Venn diagram below:

Statutory Language:

|

|

Bolded text in the left column is represented by the shaded section in the diagram |

|

“insured depository institution” does not include an institution-… (B)that does not have and is not controlled by a company that has- (i)more than $10,000,000,000 in total consolidated assets; and (ii)total trading assets and trading liabilities, as reported on the most recent applicable regulatory filing filed by the institution, that are more than 5 percent of total consolidated assets. |

|

|

“insured depository institution” does not include an institution-… (B)that does not have and is not controlled by a company that has- (i)more than $10,000,000,000 in total consolidated assets; and (ii)total trading assets and trading liabilities, as reported on the most recent applicable regulatory filing filed by the institution, that are more than 5 percent of total consolidated assets. |

|

|

“insured depository institution” does not include an institution-… (B)that does not have and is not controlled by a company that has- (i)more than $10,000,000,000 in total consolidated assets; and (ii)total trading assets and trading liabilities, as reported on the most recent applicable regulatory filing filed by the institution, that are more than 5 percent of total consolidated assets. |

|

Incorrect Proposed Regulation:

|

|

Bolded text in the left column is represented by the shaded section in the diagram |

|

(r) Insured depository institution, unless otherwise indicated… does not include:…every company that controls it has, total consolidated assets of $10 billion or less and total trading assets and trading liabilities, on a consolidated basis, that are 5 percent or less of total consolidated assets. |

|

|

(r) Insured depository institution, unless otherwise indicated… does not include:… every company that controls it has, total consolidated assets of $10 billion or less and total trading assets and trading liabilities, on a consolidated basis, that are 5 percent or less of total consolidated assets.

|

|

[1] Comments of the Competitive Enterprise Institute In the Matter of the Volcker Rule, Docket No. OCC-2017-0014, September 21, 2017, https://cei.org/sites/default/files/Volcker%20Rule%20-%20Comments%20-%2020160921.pdf.

[2] 84 FR 2780.

[3] A footnote also correctly describes the statute at 84 FR 2785 n. 40 (“Specifically, Section 203 of EGRRCPA provides that the term ‘insured depository institution,’ for purposes of the definition of ‘banking entity’ in section 13(h)(1) of the BHC Act (12 U.S.C. 1851(h)(1)), does not include an insured depository institution that does not have, and is not controlled by a company that has: (1) More than $10 billion in total consolidated assets; and (2) total trading assets and trading liabilities, as reported on the most recent applicable regulatory filing filed by the institution, that are more than 5 percent of total consolidated assets.” )

[4] A Financial System That Creates Economic Opportunities, Treasury (Jun. 6, 2017), https://www.treasury.gov/press-center/press-releases/Documents/A%20Financial%20System.pdf; see also Press Release, Treasury (Jun. 6, 2017), https://www.treasury.gov/press-center/press-releases/pages/sm0106.aspx.

[5] Id. at 14.

[6] Id. at 72-73.

[7] Id. at 72-73.

[8] Id. at 132.

[9] FACT versus Fiction, (Dec. 5, 2017), https://www.banking.senate.gov/download/12-4-myth-fact-on-fin-reg-reform-billheitkamp-tester-donnelly-warnerdocx; see also Executive Session to consider the nomination of The Honorable Jerome H. Powell and S. 2155, the Economic Growth, Regulatory Relief and Consumer Protection Act (Dec. 5, 2017), https://www.banking.senate.gov/hearings/executive-session-to-consider-the-nomination-of-the-honorable-jerome-h-powell-and-s-2155-the-economic-growth-regulatory-relief-and-consumer-protection-act.

[11] Id.

[12] https://bit.ly/2VEPuPS

[13] Id. at 2.

[14] Id. at 4.

[15] Julie A.D. Manasfi, “Systemic Risk and Dodd-Frank’s Volcker Rule,” William & Mary Business Law Review, Vol. 4, Iss. 1, 2013.

[16] For the conceptual flaws of the rule, see: Daniel Press and John Berlau, “The Case Against the Volcker Rule,” OnPoint, No. 238, Competitive Enterprise Institute, November 30, 2017, https://cei.org/sites/default/files/Daniel%20Press%20and%20John%20Berlau%20-%20The%20Case%20against%20the%20Volcker%20Rule%20%281%29.pdf; and John Berlau and Daniel Press, “Why Wall Street Loves Glass-Steagall,” OnPoint, No. 231, Competitive Enterprise Institute, August 2, 2017, https://cei.org/sites/default/files/John%20Berlau%20and%20Daniel%20Press%20-%20Why%20Wall%20Street%20Loves%20Glass-Steagall%20%282%29.pdf. For an alternative policy response to the problem of taxpayer bailouts, see: Daniel Press, “It’s Time to Eliminate Volcker Rule and Federal Deposit Insurance,” Morning Consult, August 16, 2017, https://morningconsult.com/opinions/time-eliminate-volcker-rule-federal-deposit-insurance/.

[17] U.S. Dep’t of the Treasury, A Financial System that Creates Opportunities: Banks and Credit Unions, page 8, (June 2017).

[18] Id.

[19] Andrew Clark, “Paul Volcker tells Senate: risky banking activity is like pornography,” The Guardian, February 2, 2010, https://www.theguardian.com/business/2010/feb/02/paul-volcker-senate-banking-testimony.

[20] See, for example: Group of Thirty Working Group on Financial Reform, “Financial Reform: A Framework for Financial Stability,” January 15, 2009, http://group30.org/images/uploads/publications/G30_FinancialReformFrameworkFinStability.pdf.

[21] Daniel Press and John Berlau, “CEI Comments to Office of the Comptroller on Volcker Rule,” Comments of the Competitive Enterprise Institute, September 21, 2017, https://cei.org/content/cei-comments-office-comptroller-volcker-rule.

[22] Daniel Press, “What Should Congress Do About the Volcker Rule,” OpenMarket, Competitive Enterprise Institute, November 29, 2017, https://cei.org/blog/what-should-congress-do-about-volcker-rule.

[23] Irving M. Copi, Carl Cohen and Kenneth McMahon, Introduction to Logic 349 (14th ed. 2014), http://angg.twu.net/tmp/2016-optativa/copi__introduction_to_logic.pdf