CEI Comments to Senate Banking Committee on JOBS Act 4.0

Senator Pat Toomey

Ranking Member, Senate Banking Committee

455 Dirksen Senate Office Building

Washington, D.C 20510

Dear Senator Toomey,

On behalf of the Competitive Enterprise Institute (CEI), it is our pleasure to submit the following comments authored by CEI Adjunct Fellow Paul Jossey in response to your request for feedback on the Jumpstart Our Business Startups (JOBS) Act 4.0 discussion draft released earlier this year.

CEI is a Washington-based free-market public policy organization, founded in 1984, that studies the effects of regulations on job growth and economic well-being. Our mission is to advance the freedom to prosper for consumers, entrepreneurs, and investors. CEI has long promoted policies that would improve capital formation for all types of startups and entrepreneurs and improve wealth-building opportunities for retail American investors. CEI strongly advocated for the many of the proposals included in the original JOBS Act spearheaded by you in Congress and signed into law by President Obama in 2012.

While the JOBS Act 4.0 discussion draft was initiated by Banking Committee Republicans, we encourage bipartisan support of the legislation and hope to see the bill or similar legislation pass the full Congress and be signed by the president. We thank you for the opportunity to provide this feedback and look forward to working with you to advance policies that improve capital formation, encourage investor opportunities, support entrepreneurship, and reduce regulatory barriers and burdens.

Sincerely,

John Berlau Matthew Adams

Director of Finance Policy Government Affairs Coalitions & Manager

Competitive Enterprise Institute Competitive Enterprise Institute

[email protected] [email protected]

Competitive Enterprise Institute

1310 L Street NW, 7th Floor

Washington, DC 20005 U.S.

Senate Committee on Banking, Housing, and Urban Affairs

534 Dirksen Senate Office Building

Washington, D.C. 20510

Dear Senators,

The Competitive Enterprise Institute (CEI) responds to the request of many members of the Senate Banking Committee for feedback on the discussion draft of the JOBS Act 4.0 released on April 4, 2022.[1] While all sections of the bill have merit, comments herein focus on three sections and provide additional proposals to improve capital formation in the United States, particularly via the private markets. Noted sections are: Sec 204: S.3939 – Small Entrepreneurs’ Empowerment and Development (SEED) Act of 2022; Sec. 305: S.3967 – Improving Crowdfunding Opportunities Act; and Sec. 307: S.3966 – Facilitating Main Street Offerings Act. CEI stands ready to assist staff in implementing these proposals.

- Private Market Capital Remains Concentrated in Elite Zip Codes Showing Need for Further Exemptions

Private capital raising is clustered around a few elite zip codes with high concentrations of wealthy accredited investors and cultures of entrepreneurship. Venture capitalists and angel investors tend to invest in startups within short distances from where they are located.[2] This has real effects on American prosperity. One study found areas that lack access to accredited ‘angel’ networks experience reduced startup activity and compounded negative economic impacts.[3]

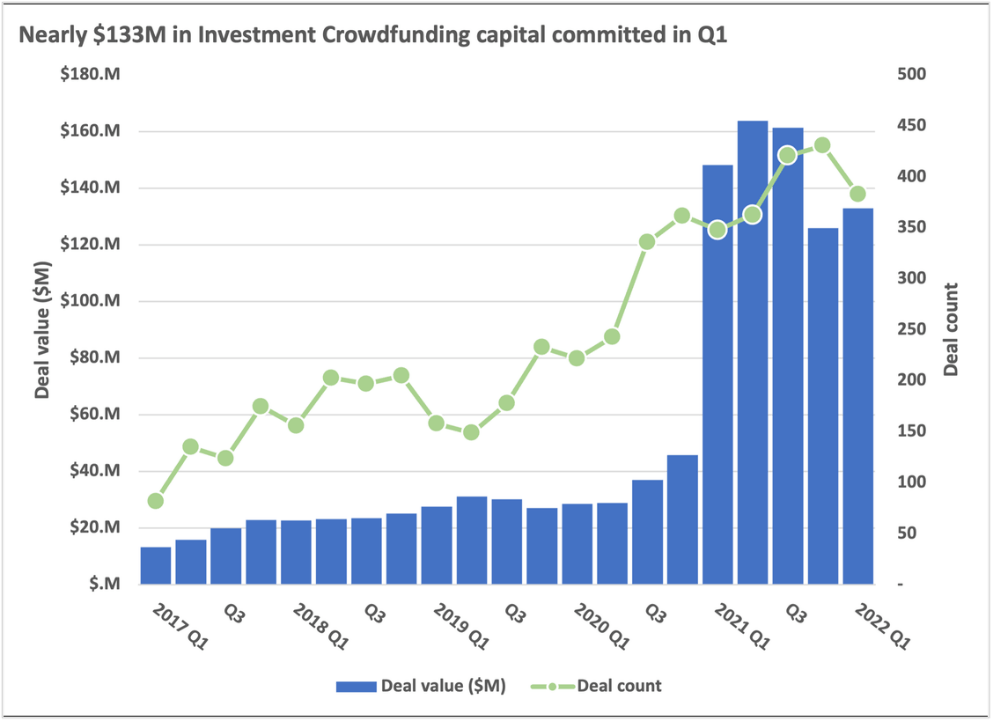

Title III of the JOBS Act of 2012,[4] which the Securities and Exchange Commission (SEC) implemented as Regulation Crowdfunding (Reg CF), sought to remedy this situation by opening the private market to retail investors. After a shaky start fueled by SEC hostility,[5] Reg CF has bloomed. Despite the concentration of major intermediary portals in California, preemption of state securities laws and Reg CF’s online nature has reduced geographic barriers to private capital. Particularly after SEC deregulatory efforts which went into effect in March 2021,[6] Reg CF has matured into a vibrant exemption and an example of the benefits of deregulation.[7]

Source: Crowdfund Capital Advisors

But an additional lower-level exemption like the Small Entrepreneurs’ Empowerment and Development (SEED) Act of 2022 as proposed by Senators Tim Scott (R-SC) and Jerry Moran (R-KS) could also help. The SEED Act’s preemption of federal and state securities laws for issuers offering up to $500,000 per 12-month period would lessen the cost of capital, which Reg CF issuers often complain.[8]

Whether allowed to offer securities on the existing Reg CF portal infrastructure or through not-yet-created exchanges, the reduction in disclosure burdens would aid entrepreneurs outside existing capital-rich locales.

- Congress Should Preempt Secondary Trading from State Securities Laws

Two sections of the JOBS Act 4.0 address preemption for secondary trading. Sec. 305: S.3967 – Improving Crowdfunding Opportunities Act, sponsored by Senator Jerry Moran (R-KS) would preempt secondary trading for Reg CF instruments. Sec. 307: S.3966 – Facilitating Main Street Offerings Act, also sponsored by Senator Moran would preempt secondary trading for Regulation A (known as Reg A+). These bills are crucial for the continued private-market success. Currently, both are federally freely tradable (Reg CF after one year). But state-by-state trading restrictions have blocked development of secondary markets. These state regulations were designed for a slower, less connected world and Congress should preempt them.

The SEC has acknowledged the burdens state regimes place on these exemptions, stating that “preemption could further advance the development of a national securities market by easing the compliance obligations of investors that trade in the secondary markets.”[9] Yet it refuses to act absent “an opportunity for market participants to receive notice and comment on a specific proposal.”[10] As explained below, the current SEC leadership is unlikely to entertain such proposals given its hostility to markets.

Preempting state-level restrictions on secondary trading has additional benefits. First, it acts as a form of investor protection by adding liquidity to investor holdings. As House Financial Services Committee Ranking Member Patrick McHenry (R-NC) stated, “The liquidity provided by a secondary market is an investor protection in and of itself, because it would allow individuals whose financial situation has changed to exit these investments in times of need.”[11]

Second, preemption may provide some clarity to the cryptocurrency market for tokens deemed as “securities” by the SEC. Current SEC Chair Gary Gensler has exacerbated the confusion and uncertainty around the crypto markets left by his predecessor Jay Clayton. Mr. Gensler’s enforcement-only policy[12] has harmed innovation and thwarted opportunities for the retail investors he claims as wards.[13] His steadfast refusal to admit the folly of his approach worsens the calamities of his approach.[14] Senator Toomey (R-PA), Ranking Member of this committee, has recognized Mr. Gensler’s intransigence, after requesting detailed answers to his crypto approach. “Chairman Gensler’s responses did not answer which cryptocurrencies the SEC views as securities and which it views as commodities. Some questions went completely unaddressed.”[15]

CEI previously submitted comments to this committee on clarifying crypto regulation.[16] Whilst these comments focus on the private markets generally, preempting state-level trading restrictions would have undeniable benefits to this emerging and vibrant market currently suffocating under uncertain rules and myopic federal leadership.

- Additional Proposals to Improve Private Capital Formation[17]

Preempt state filing requirements and notice fees for Regulation A+ and Regulation Crowdfunding. State filing and notice fees serve no cognizable purpose. They do not protect investors, facilitate capital, or improve markets. They are regressive, expensive, and disproportionately hurt smaller issuers. Reg A+ fees are littered with waste, inconsistencies, and timing issues, with no related benefit.[18] This model departs from Regulation D 506(b), where issuers invoke state filing costs only after local sales. Reg A+ and Reg CF issuers place all offer documents on EDGAR[19] making them publicly available for fraud investigations. At the least, Congress should reconcile Reg A+ issuers that often pay fees to all possible jurisdictions with Reg CF where at most issuers pay two.[20]

Raise the Regulation A+ Offer Limit to $100 million. Congress should raise the Reg A+ 12-month aggregate offer limit to $100 million. After previous considerations, the Commission has now raised it to $75 million.[21] Given the usual pace it may be several more years before it is raised again, despite Congressional directive. Congress should skip this potentially years-long wait while keeping Reg A+’s biennial review.

Raise the Regulation Crowdfunding Offer Limit to $20 million. Congress should raise Reg CF’s 12-month aggregate offer limit to $20 million and add a statutory requirement like that in Reg A+ that the Commission biennially review it. The Commission raise to $5 million took almost four years and another change will likely follow this pace. Without significant encouragement to monied investors, Reg CF adoption will remain hampered despite recent spectacular gains.

Simplify or eliminate individual limits for Regulation A+ and Regulation Crowdfunding. Congress should remove individual formulas for unaccredited investors in Reg A+ and Reg CF and replace them with hard dollar amounts per investment, not aggregate per 12 months. The Commission has now eliminated Reg CF accredited investor limits. But both Reg A+ and Reg CF still impede unaccredited investors with annual income, net worth formulas. This confuses investors and invokes security and privacy concerns. A hard inflation-adjusted number would be simpler and straightforward. For instance, $10,000 per Reg CF investment and $20,000 per Reg A+. Alternatively, and preferably, Congress should remove the limits completely.

Conclusion

If enacted, the JOBS Act 4.0 would foster economic resiliency and provide opportunity for entrepreneurs and investors alike amidst rising inflation and market uncertainty. It is especially important Congress continue opening the private markets to all Americans, not just wealthy individuals living in select locales. The sections highlighted herein would do just that. In addition, the other deregulatory initiatives proposed in this letter would further aid this effort.

CEI welcomes the opportunity to discuss these proposals or provide additional assistance as this important bill continues the legislative process.

Paul H. Jossey

Adjunct Fellow

Competitive Enterprise Institute

[1] “Banking Republicans Roll Out Capital Formation Legislation to Mark 10th Anniversary of JOBS Act,” Press Release, April 4, 2022, https://www.banking.senate.gov/newsroom/minority/banking-republicans-roll-out-capital-formation-legislation-to-mark-10th-anniversary-of-jobs-act.

[2] Jason Rowley, Where Venture Capitalists Invest and Why, TECHCRUNCH (Nov. 9, 2017), https://techcrunch.com/2017/11/09/local-loyalty-where-venture-capitalists-invest-and-why/ (describing how venture-capital funds tend to invest in firms within close geographic proximity); cf. Dana M. Warren, Venture Capital Investment: Status and Trends, 7 OHIO ST. ENTREPRENEURIAL BUS. L.J. 1, 12 (2012) (“Venture capital investment almost always involves significant participation in and oversight of each of the portfolio companies by the venture capital professionals. As a result, simple logistics makes venture capital investment an inherently local, or at most regional, activity.”).

[3] LAURA ANNE LINDSEY & LUKE C.D. STEIN, ANGELS, ENTREPRENEURSHIP, AND EMPLOYMENT DYNAMICS: EVIDENCE FROM INVESTOR ACCREDITATION RULES (Sixth Annual Conference on Financial Market Regulation 2019), https://ssrn.com/abstract=2939994.

[4] Jumpstart Our Business Startups Act, Pub. L. No. 112-106, 126 Stat. 306, 315-323 (2012).

[5] The JOBS Act at Five: Examining Its Impact and Ensuring the Competitiveness of the U.S. Capital Markets, H.R. Doc. No. 115-9 (1st Sess. Mar. 22, 2017) (testimony of Mr. Edward Knight, Exec. Vice Pres. and Gen. Coun., NASDAQ) (“From the outset the SEC’s view of [equity crowdfunding] was they were not for this they and made it, shall I say, needlessly complicated and did not approach it except as this this was something where the public is going to get harmed and we need to narrow it as much as possible.”).

[6] Facilitating Capital Formation and Expanding Investment Opportunities by Improving Access to Capital in Private Markets, Securities Act Release Nos. 33-10884; 34-90300 (November 2, 2020) https://www.sec.gov/rules/final/2020/33-10844.pdf.

[7] Paul H. Jossey, “Equity Crowdfunding Success Should Spur Further Deregulation,” Open Market, Competitive Enterprise institute, January 12, 2022, https://cei.org/blog/equity-crowdfunding-success-should-spur-further-deregulation/.

[8] SEC, REGULATION CROWDFUNDING, A Financial System That Creates Economic Opportunities Capital Markets, U.S. DEPT. OF THE TREASURY, at 40 (Oct. 2017), https://www.treasury.gov/presscenter/press-releases/documents/a-financial-system-capital-markets-final-final.pdf, (“[M]arket participants have expressed concerns about the cost and complexity of using crowdfunding compared to private placement offerings.”).

[9] Facilitating Capital Formation and Expanding Investment Opportunities by Improving

Access to Capital in Private Markets, n. 389 (Referencing Reg A+ Tier 2); cf. n. 439 (Referencing Reg CF), https://www.sec.gov/rules/final/2020/33-10884.pdf.

[10] Ibid.

[11] Rep. Patrick McHenry, Letter to Hon. Jay Clayton, Chair Securities and Exchange Commission, May 15, 2017, https://www.sec.gov/comments/s7-08-19/s70819-6293559-193383.pdf.

[12] See, e.g. Hon. Gary Gensler, Prepared Remarks At the Securities Enforcement Forum, November 4, 2021,

[13] Paul H. Jossey, “SEC’s War on Crypto Savers Continues,” Open Market, Competitive Enterprise Institute, April 26, 2022, https://cei.org/blog/secs-war-on-crypto-savers-continues/.

[14] Paul H. Jossey, “Professor Gensler Gets and F in crypto,” CoinDesk, January 23, 2022, https://www.coindesk.com/layer2/2022/01/23/professor-gensler-gets-an-f-on-crypto/.

[15] “Gensler Skips Chance to Give Regulatory Clarity on Cryptocurrencies,” Press Release, December 3, 2021, https://www.banking.senate.gov/newsroom/minority/gensler-skips-chance-to-give-regulatory-clarity-on-cryptocurrencies.

[16] Paul H. Jossey, “CEI Filed Legislative Proposals to Rescue Crypto,” Competitive Enterprise Institute, September 30, 2021, https://cei.org/blog/cei-files-legislative-proposals-to-rescue-crypto/.

[17] These proposals are taken directly from, Paul H. Jossey, FIXING THE JOBS ACT AND INVITING THE TOKENIZED FUTURE, THE NEED FOR CONGRESSIONAL ACTION, Arizona St. Corp. and Bus. L.J., Vol.2:2: Feb. 2021, https://cablj.org/wp-content/uploads/2021/02/Jossey_READY.pdf.

[18] Letter from Sara Hanks, CEO, Crowdcheck, to the SEC on the Concept Release, at 29 (Oct. 30, 2019), https://www.sec.gov/comments/s7-08-19/s70819-6368811-196431.pdf, ((“[T]he states have differing requirements with respect to the timing of notice filings ranging from requiring filing 21 days prior to ‘offers’ (which is not consistent with the ability to test the waters under Rule 255) to requiring filing prior to qualification, to not accepting filings before qualification.”).

[19] About EDGAR, U.S. SECURITIES AND EXCHANGE COMMISSION, (May 28, 2022),

[20] 15 U.S.C. § 77r(c)(2)(F).

[21] Facilitating Capital Formation and Expanding Investment Opportunities by Improving

Access to Capital in Private Markets, p. 133-135, https://www.sec.gov/rules/final/2020/33-10884.pdf.